Download PDF:

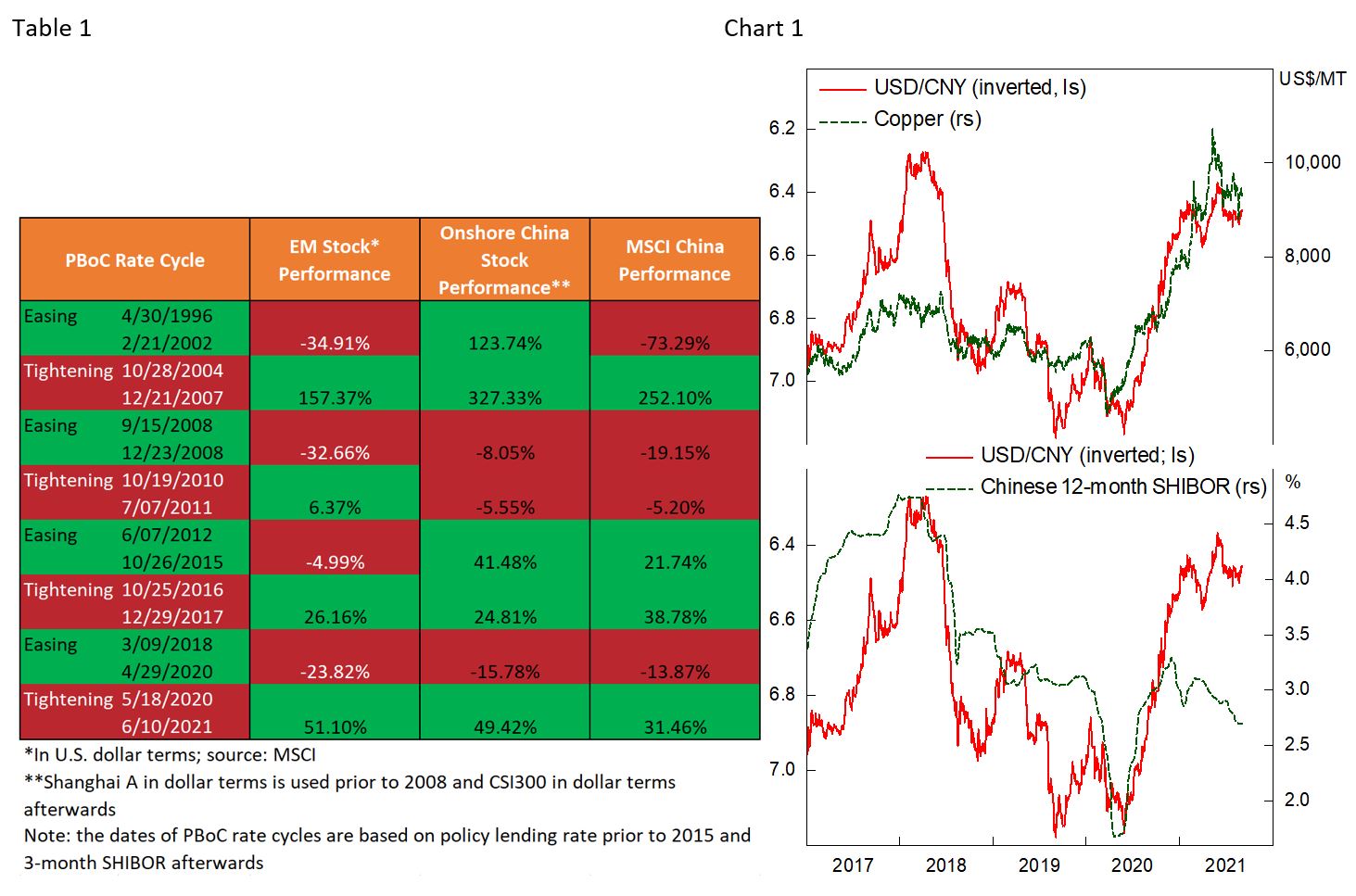

Chinese manufacturing and services PMI print for August shows growth continued to shift lower amid tight credit and fiscal condition, although it is probably worsened by the mini-outbreak and restrictions last month that distort the number to the downside. One important thing to note is that growth momentum in the rest of world has also shown signs of weakness, with activities and employment coming below market expectations. High-frequency data coming from mainland China will likely continue to disappoint until the end of year despite the authorities’ efforts to reflate the economy. In terms of market, the downside risk for Chinese equities remain as regulatory crackdown on the tech sector seems to be still ongoing and materials, industrials, and financials likely suffer during the down cycle as commodities correct and the PBoC start cutting rates. Historically, periods of Chinese policy easing have boded poorly for EM, Chinese stocks, and risk assets in general (Table 1).

More importantly, global risk assets will be weighed down by the slowdown in Chinese economy, with the impact increasingly felt in the coming months. Generally, stocks and commodities should correct, while Treasury bonds will remain well bid. The policy divergence between China and rest of world should also provide opportunity for macro investors in the currency space to short CNY versus the greenback. Both the Fed and ECB are now talking about tapering of its QE program, although policy rate increase is still far ahead and remains too optimistic, especially for the former. Meanwhile, Chinese central bank will err on the dovish side in the coming months as economic data continues to worsen. Policy divergence, potential shakeout in risk assets, and increasing visibility on global growth slowdown all point to a stronger dollar in the coming months (Chart 1).

In turn, stronger dollar will put a lid on the rally in Emerging Market stocks and currencies, commodities, and select high-yield sector bonds. Since June we have been trading copper from the short side with handsome reward, although daily volatility of the metal remains high, at times surging 3% in a day. This highlights the importance of selling on strength instead of chasing the slump in prices.

Commodities and Precious Metals

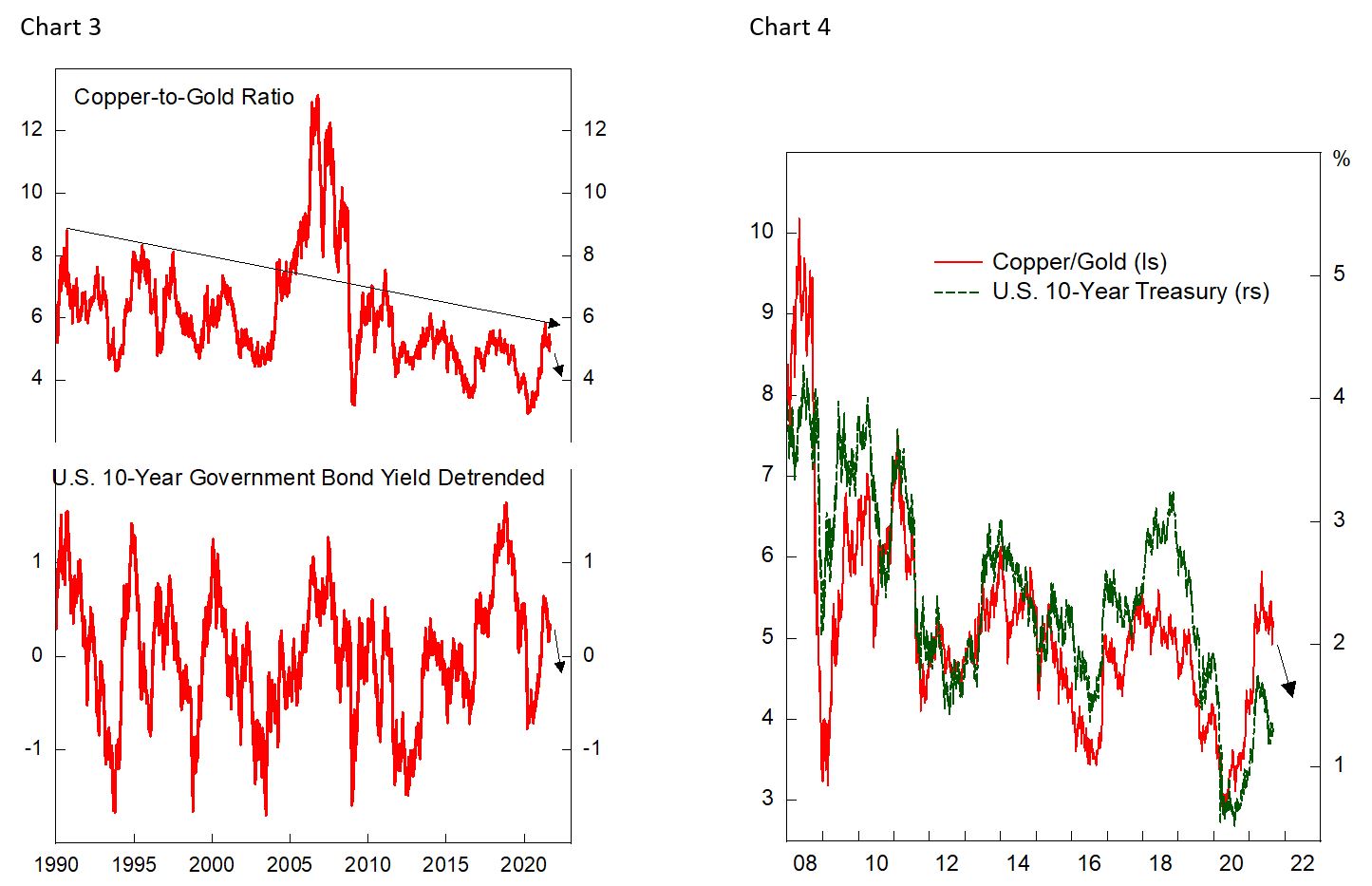

The outlook for Treasury yields remains on the downside. With the Fed already making its dovish pivot during the Jackson Hole meeting, the current growth slowdown in U.S., and Europe in the coming months, should drive Treasury yields lower, dragging copper-to-gold ratio along with the strength in the dollar (Chart 3 and 4). As we noted in previous publication, a decline in copper-to-gold ratio and yields have normally coincides with correction in copper and gold in dollar absolute terms, with the former underperforming, hence the decline in the ratio.

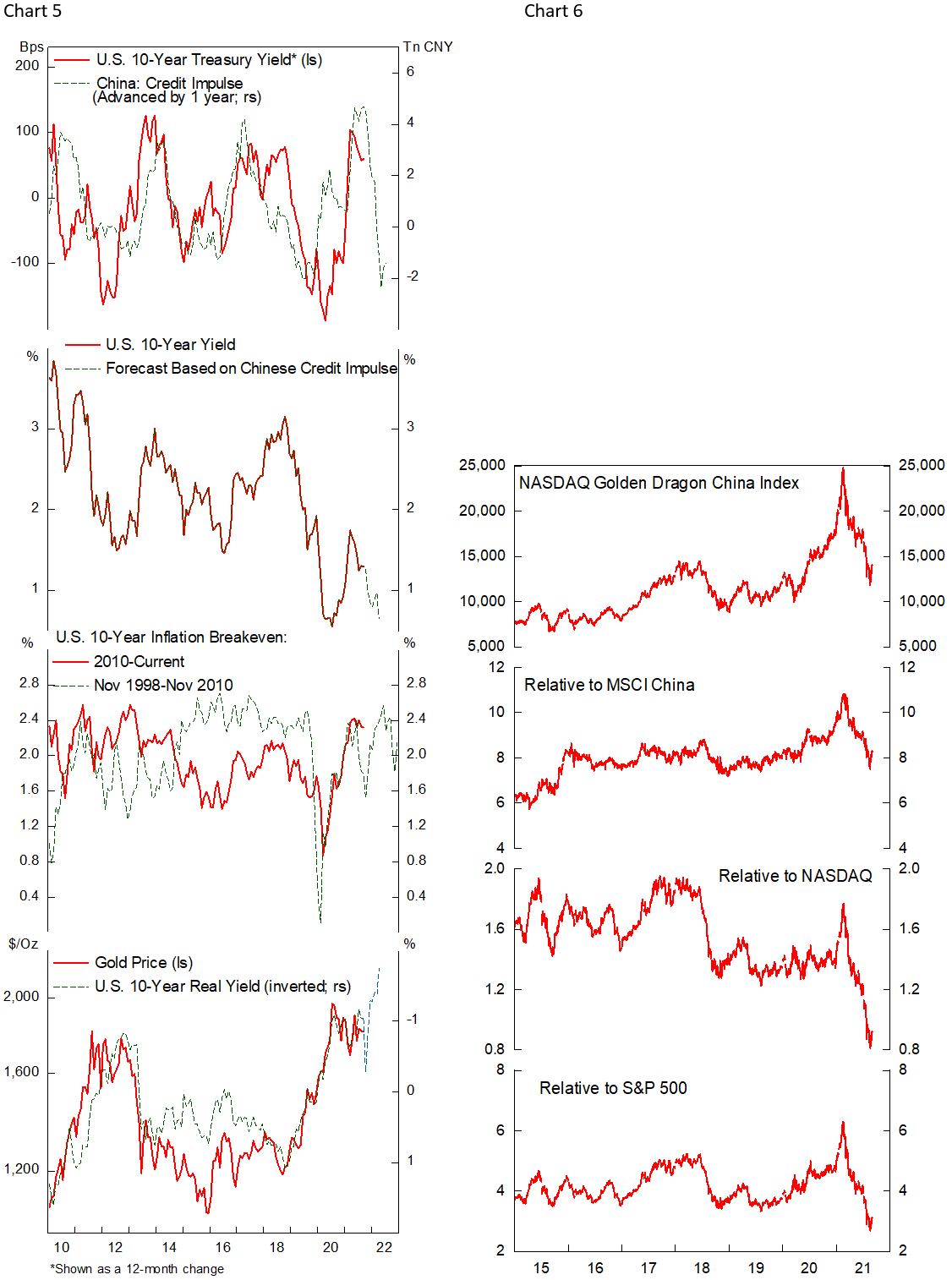

The potential dollar’s strength makes the outlook for precious metals more complicated, as decline in real yields could be hampered by the stronger dollar. Chart 5 shows our projection for U.S. 10-year yields, inflation breakeven, and real yield. Under this scenario, gold could surge above $2200/Oz, should the dollar steady. However, our conviction on this trade is low, unlike our short copper trade.

A Word on Chinese Tech Stocks

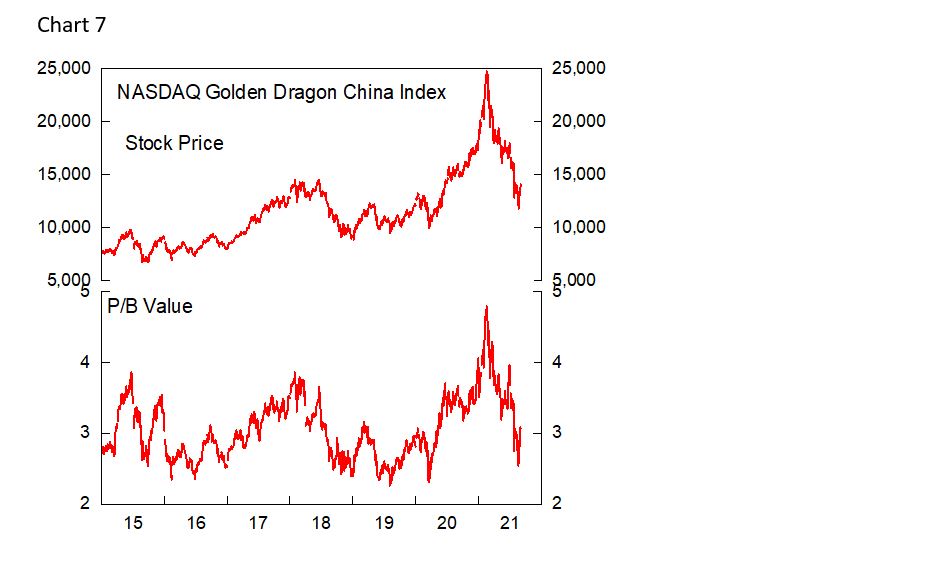

Recent selloff in Chinese tech names points to sensitivity of tech stocks to a combination of decline in terminal growth rate and increase in equity risk premium. A regulatory crackdown shed 50% of the market cap of Chinese tech names, bringing P/V value from 5 to 3 times (Chart 6 and 7). Should the Biden administration ramp up its anti-monopoly policies and Lina Khan, chair of Federal Trade Commission, succeed in limiting the growth of (or even breaking up) U.S. tech names, similar impact could be felt among the FAANGM stocks, which account for a quarter of the S&P500 index.

Investment Conclusion

The bottom line is that investors should continue to be defensive in terms of asset allocation. Traders could accumulate position by selling on strength in risk assets with a tight stop loss (i.e., 5% trailing). Remains bearish on copper until Chinese policy reflation intensifies and economic data reach bottom, which could be around the end of year. Long the dollar vs fragile currencies and buy bonds.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.