Download PDF:

Central banks in Czech and Hungary have begun to raise their policy rate this year amid acceleration in inflation as their domestic recovery unfolds, creating a tailwind for the koruna and forint against the Euro, which will not see the ECB raising its borrowing cost anytime soon (Chart 1). With Central and Eastern European countries well-integrated to Western European supply chain and the region benefitting from ECB’s easy monetary policy, the widening spread against German bunds should push yield-seeking capital into the region, further bolstering their currencies. So far this quarter our overweight recommendation (EMC_20210707) for CEE stocks has panned out well, with Czechian, Hungarian, and Polish stocks advancing 10% on average in absolute terms since July. Going forward, we are expecting further gains for several reasons.

- First, more than half of Czechian and Hungarian equity indices, and over a third of Polish index are comprised of banks, which benefits from the spread widening between local curve and its Western European counterpart (Chart 2). Although banks’ profitability across the European Union have been pummeled since the Euro crisis as the ECB brings policy rate to negative, banks in CEE fare relatively well with net interest margin much higher than its Western and Southern European counterpart, while faster economic growth also bodes well for their lending operation (Chart 3). The divergence between policies within the region is also worth paying attention. With the Polish central bank being relatively dovish compared to Czech’s and Hungary’s and its equity index having a lower share of banks stocks, Poland’s equity and the zloty should continue to lag the advance in Czechian and Hungarian stock and currency in the current tightening cycle.

- Second, valuation of CEE stocks is cheap, and these bourses are trading at a discount relative to EM benchmark (Chart 4). Derating of the region’s bourses is advanced and rebound in earnings and expectations will likely propel stock prices higher. In addition, CEE bourses are defensive and historically outperforms during broad-based market correction.

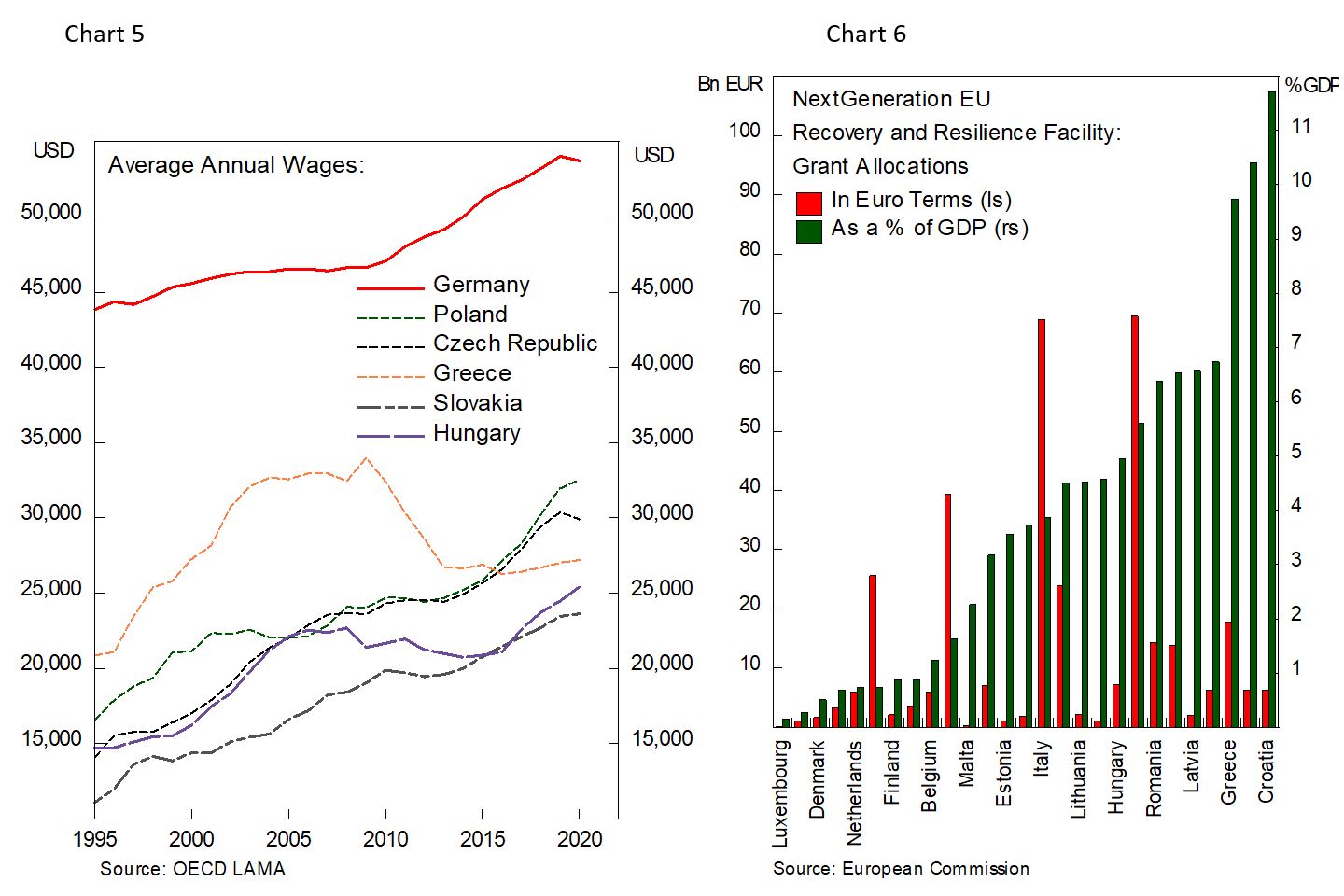

- Third, CEE countries will continue to benefit from the shift in manufacturing base from Western Europe amid much lower labor cost compared to in Germany and France (Chart 5). The CEE countries currently export 25-35% of its goods to Germany and benefit from the current upswing in manufacturing activities, despite semiconductor supply chain issues that affect auto manufacturers. More importantly, due to larger income gap relative to the region, these countries are among the largest recipients of EU transfers, including from the EUR 750 bn NextGeneration EU (NGEU) fund that aims to boost the post-pandemic recovery through improvement in education, healthcare, and other physical and social infrastructure. In total, the annual boost from NGEU fund is worth 3-5% of GDP, on top of the 1-2% of GDP annual transfer under the EUR 1.074 tn Multiannual Financial Framework (MFF) scheme (Chart 6 and 7).

In sum, current tightening in monetary policy should see these countries’ currency appreciate against the euro while also boosting bank’s profit, which is a big chunk of the equity indices. In the medium term, the structural bullish case for CEE countries’ economy remains intact as the region’s success in transitioning from post-Soviet collapse to an open economy and democratic system has allowed CEE countries to share the benefit of globalization and lift wages multiple folds during the past two decades, one of many factors that are driving the global deflationary trend since the turn of millennium. In the longer run, however, two factors are becoming headwinds for the region’s growth, namely aging population and domestic political consideration.

Declining fertility rate and longer life expectancy bode poorly for CEE countries’ dependency ratio, which is set to increase significantly until the middle of the century (Chart 8). Older and unproductive population will add extra burden to the state’s welfare expenditures that may eventually result in higher tax rates to plug the deficit. In addition, without abundant supply of cheap labor wages could start to rise, which if not supported by corresponding rise in productivity could translate to higher unit labor cost and more labor being replaced by robots. A stagnation in living standard, in turn, could affect domestic political environment and further tilt the scale towards populism.

On the later, Hungary’s prime minister is championing the country to become an “illiberal democracy”, whatever that means, while the Polish government is tightening its control on the judiciary for years and silencing its critics through the controversial media bill approved last month, both of which has been a sticking point with the EU over the primacy of the domestic rule-of-law. These issues matter as the EU has many times threaten to withhold its funds to these two countries to force compliance to EU’s values and laws. Although the economic benefit of being an EU member is clear, it does not preclude both countries leaving EU once the contribution to EU budget exceeds the benefit, which is expected to occur in the next decade. Despite these longer-term headwinds, however, we expect the region’s stocks and currencies to do well amid the policy rate hike in the coming months.

Bottom line: remain overweight Czech, Hungary, and Poland’s equity in an EM portfolio and long an equal-weighted basket of HUF and CZK against the Euro.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.