Download PDF:

This month’s monthly piece is a short note on three signposts to monitor the growth recovery, taking a bird-eye perspective on risk assets after three separate publications last week detailing our view on oil, precious metals, and select country outlook; links are provided at the end of the piece. First, we are revisiting three important indicators to monitor global growth outlook: the dollar, Treasury yield, and copper/gold ratio.

The dollar should decline further from current level, although technical and speculative positioning show that the selloff in the dollar is overstretched, which may point to a short-term rebound. The uncertainty regarding further fiscal stimulus, November presidential election, and changing consumer behavior from a prolonged lockdown restriction all point to an elevated volatility and rebound of the dollar in the coming month.

In more recent days, speculative position also points to more short interest in long-term U.S. Treasury. The 10-year yield has back up to 0.77% from its 0.50% low – still a very depressed level amid Fed’s commitment to hold rates at zero at least until 2024 – and further normalization in economic activity and growth measures should drive yield closer to 1%.

Copper/gold ratio should also trend upward, although both metals’ price could rise altogether. The increasing copper demand from China for production of electronic goods, electricity line, and EV battery should all point to a structural bull market for copper. Meanwhile, we are still positive on gold price in the long-term due to the debasement of fiat currency in the U.S. to finance fiscal stimulus.

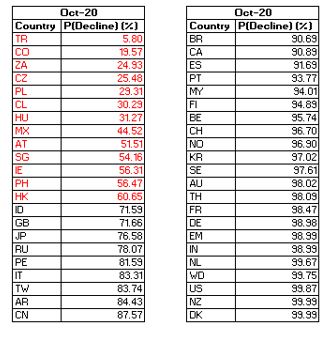

On equities, we think the valuation is being inflated by record low yields and few alternatives for investors to put their money in. Although the risk/reward is not attractive, it may continue to be so considering a still elevated equity risk premium. Our Global Equity Strategy model do not like any country equity in particular this month, preferring to be invested in the ACWI benchmark. We believe this is due to the still poor earnings outlook and elevated valuation in over 75% of investable DM and EM countries.

We continue to monitor the development in Turkey. Two months ago, we pared down our long Turkish position significantly amid concern on their reserves and too loose monetary policy. Now we begin to see a deep value play in the country as the Lira has become very cheap and equity valuation is on a bargain. We discussed our favorable view for Colombia and Chile in a more recent piece. Meanwhile, our call options on Mexican equity initiated in Q1 has delivered significant return, which will have further leg from both currency and stock appreciation.

For a more detailed analysis, we separated the three topics we want to highlight this month on a separate piece:

Where Are Precious metals Headed

Country Outlook for Russia, Colombia, Chile, South Africa, and Indonesia

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.