Download PDF:

Russia -Neutral View

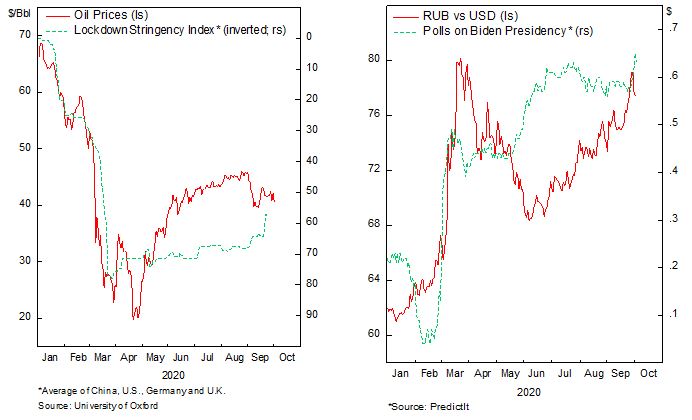

+ The tendency for oil prices is to move higher as global lockdown restrictions are lifted and a nation-wide lockdown is averted amid the virus’ second wave infection. Half of Russian equity index is dominated by energy companies and the economy is also very dependent on oil prices, making Russian stocks and currency a high beta play for oil movement.

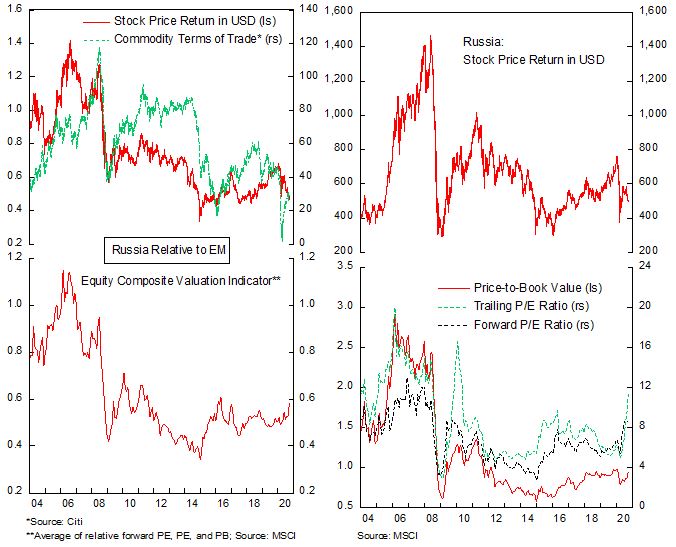

– Russian parliament last week passed mineral extraction tax increase bill, which increases the taxes of companies mining metals, ores and rock used to manufacture fertilisers by 3.5x starting in 2021. The government estimate that it will raise $ 700 million and help plug in fiscal deficit. This will put a further pressure to earnings of mining-heavy Russian stocks at a time when global commodity price is still weak. Moreover, Russian equity is no longer dirt cheap at 8.5x forward P/E, above its last 5-year average.

– Another risk relates to what a Biden Presidency could mean for Russia, whose probability has increased markedly. The former vice-president and Democrats have a tough on Russia policy and may put further sanctions on Russia amid its violation of international law and the suspected poisoning of Alexei Navalny, the anti-corruption activist and opposition of Putin’s regime. Although Russia has ringfenced its economy since 2015 amid its annexation of Crimea, the Rubble and current equity valuation will be under pressure on the news of a renewed international sanctions.

Colombia – Positive View

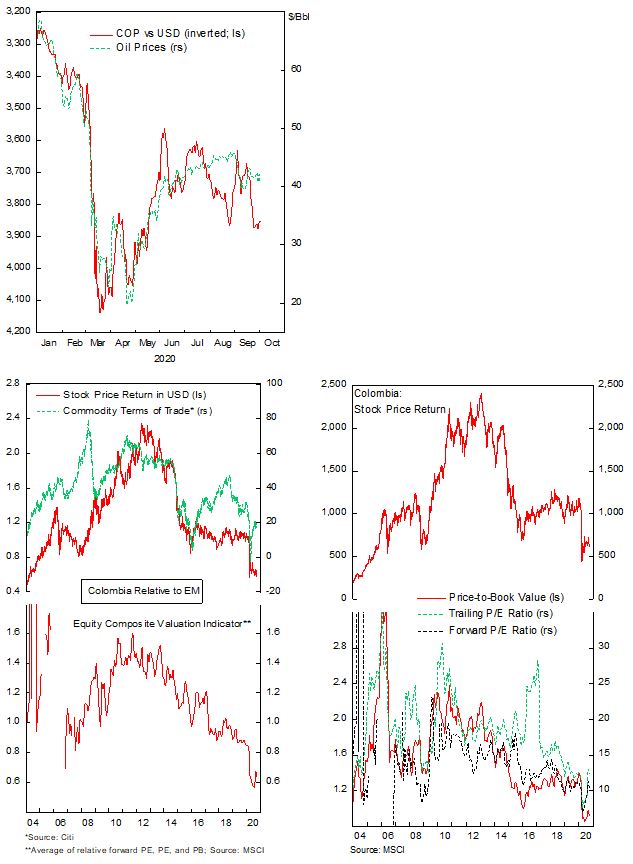

+ The tendency for oil prices is higher as lockdown restrictions are lifted and a nation-wide lockdown is averted amid the virus’ second wave infection. Colombian economy and the market are well-correlated with oil prices, and there is less geopolitical risk in Colombian assets relative to its Russian counterpart.

+ Colombian stocks and the peso lag the recovery in oil prices, mostly due to heightened risk premium demanded by investors amid the poor health care situation across major Latin American countries. Valuation of Colombian equities remain cheap on a stand-alone basis and is on its historical low relative to EM. A recent downtrend in the country’s infection cases should allow the government to ease its lockdown restriction gradually in the coming months, allowing greater economic activity to rebound.

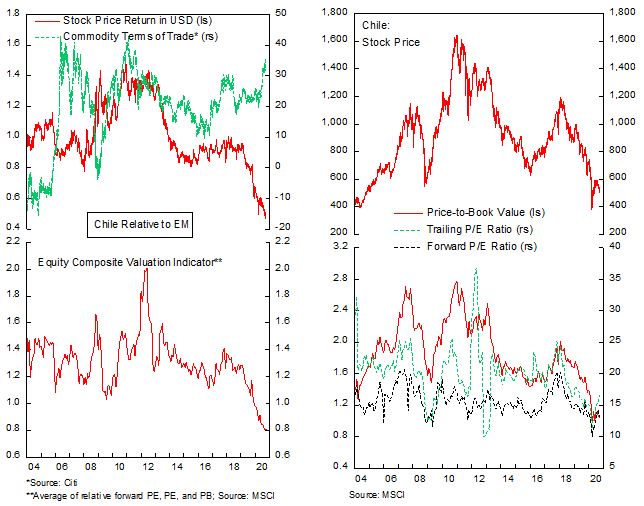

Chile – Positive View

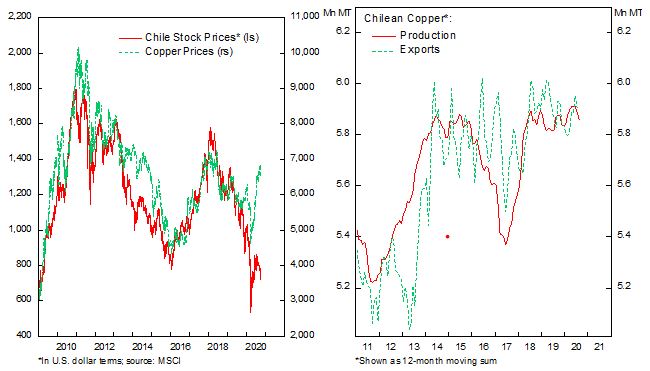

+ The rebound in copper prices remain impressive amid strong Chinese demand while Chilean equity, historically closely tracking copper prices, lags significantly. This is due to both contraction in valuation multiples and poor profitability of Chilean stocks, which are facing increasing costs in the past two years. If anything, the downtrend is late in the cycle and a further rise in copper prices amid strong demand from China and long-term Electric Vehicle (EV) demand should be a tailwind to producers’ profit going forward.

+ Despite the lockdown restriction, copper production and exports remain strong, a rebuttal to the argument that rising copper prices are mainly due to falling global supply. At 13.5x forward P/E and trading at a book value, Chilean equity valuation is not demanding and likely to expand as global growth improves.

– The constitutional referendum, planned later this month, will decide whether the country will draft a new constitution as demanded by the protesters on last year’s upheaval. The referendum will also decide on whether existing legislators or a directly elected body will write the new charter. A new constitution will likely drift the country marginally to the left, supporting the way for more social support by the government to poorer households. In the longer term, this will sharpen investors’ question on whether the country will take a leftist drift and turn the country on a more similar path with its neighboring Argentina.

– The constitutional referendum, planned later this month, will decide whether the country will draft a new constitution as demanded by the protesters on last year’s upheaval. The referendum will also decide on whether existing legislators or a directly elected body will write the new charter. A new constitution will likely drift the country marginally to the left, supporting the way for more social support by the government to poorer households. In the longer term, this will sharpen investors’ question on whether the country will take a leftist drift and turn the country on a more similar path with its neighboring Argentina.

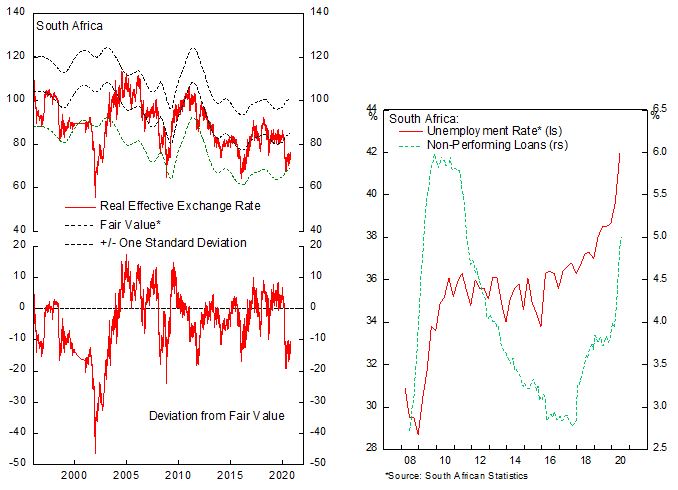

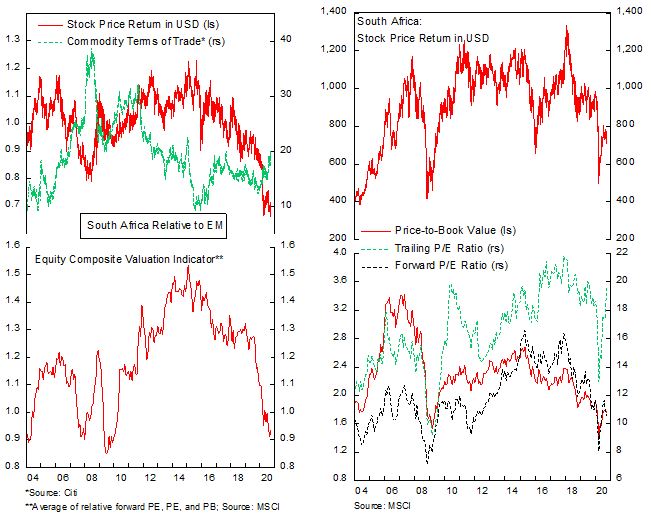

South Africa -Neutral View

+ The underperformance of South African equities is well-advanced, and a rebound is due. The equity market is trading at 10.5x forward earnings, the lower end of its long-term average. The country’s term of trade has improved of late, supported by rising gold and commodity prices, which should be a tailwind to profits (10% of its equity index is gold miners and 23% is classified as materials).

+ The country has been bombarded by bad news even prior to the pandemic, which is increasingly priced in the asset market. Inflation has remained subdued despite the Rand weakness, which allows the SARB to ease monetary policy this year. The ZAR is cheap, according to our fair value assessment, and an improving outlook will inevitably lift high-beta Latam currencies and the Rand.

– The long-term macro picture of the country remains bleak. First, the country’s unemployment rate is surging above 40% and President Ramaphosa has been unable to break through necessary public sector reform and privatization of its ailing SOEs. Second, the country is riddled by an electricity blackout due to Eskom, its national electricity company, poor management and indebtedness, which create a drag on growth. Third, the government’s poor fiscal situation prevents it from bailing out its high-indebted SOEs, leaving the banking sector to take the hit to their earnings. Currently there seem to be no political willingness and capacity for the country to reverse its trajectory amid the conflicting interest within ANC itself (the president’s party).

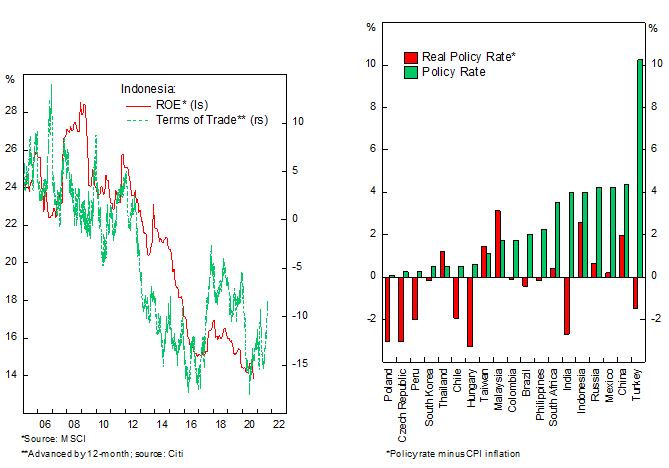

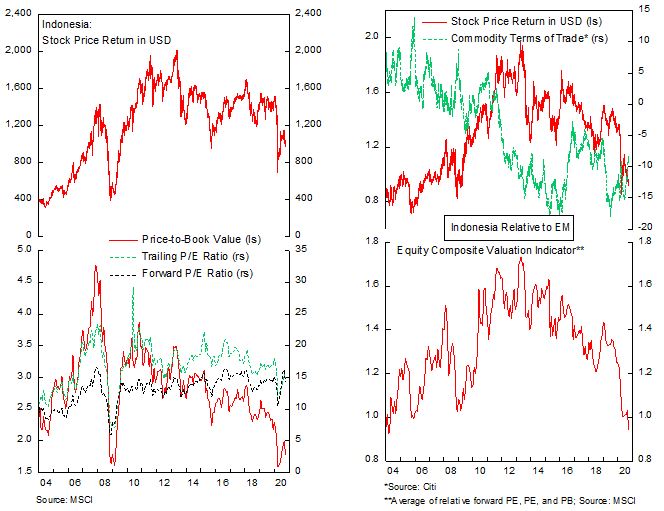

Indonesia – Positive View

+ Indonesian equity valuation has derated significantly in the past decade due to the cyclical decline in commodity prices and profits. This has removed the froth in its stock valuation, which currently trading at a slight discount relative to EM benchmark, at a time when the country’s terms of trade have been improving. The prospect of a further dollar weakness and accelerating growth in China will likely further boost commodity prices in the medium term and benefit commodity-exporter countries, including Indonesian equities.

+ The recent weakness in Indonesian equity and currency may prove to be short lived, mainly due to investors’ aversion as the government decided to impose another lockdown in Jakarta last month amid increasing infection cases, and the scare surrounding a proposed recommendation that could weaken the independence of its central bank. The proposal to legislation committee includes expanding Bank Indonesia’s mandate to not only managing the currency value, but also on growth and employment, and the formation of Monetary Council to whom the central bank would be under supervision. In response to the proposal, President Jokowi and his finance minister pledged that BI would remain independent.

+ Rupiah is among one of the highest yielding EM currencies, in both nominal and real terms. This makes it more attractive for foreign investors searching for higher yield, supported by the relatively favorable government fiscal situation. Moreover, the central bank’s conservative move in cutting policy rates despite low inflationary pressure likely put a further support for the currency.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.