Download PDF:

South African government fiscal situation turned from bad to worse this year amid a shortfall in tax revenue and increase in spending to support growth (Chart 1). The government’s revision to its budget in June mainly reflects a shifting of its spending, i.e. delaying projects to 2021/2022 or beyond while prioritizing funds for the Covid-19 fiscal relief package (Table 1-3). Although the aide to the economy by increasing transfer payment to the poor and unemployed is welcome and should provide a floor to growth, this come at the cost of a huge dent to the government fiscal and a delay in investments that are important for the country’s long-term growth drivers.

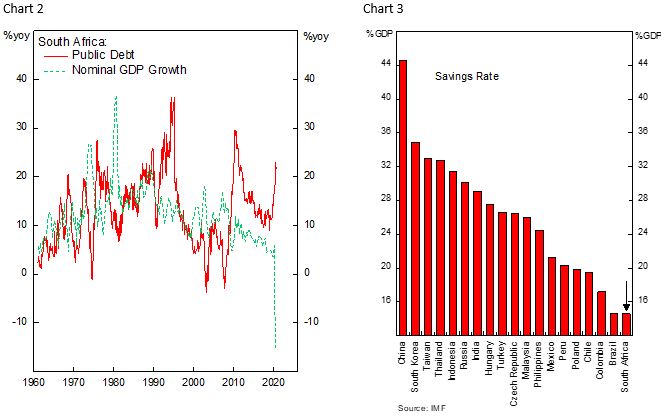

Chart 2 shows that South African economy has barely grow in the past decade amid low productivity growth and the country is weighed by numerous structural and political issues. First, the country is trapped in the cycle of low savings and investment – the country’s savings rate is among the lowest among EM countries, even lower than Latam countries (Chart 3). Second, unemployment remains stubbornly high amid low skill working age population, although the government has been increasing its spending allocated to education (Chart 4). Third, inequality is rampant, and the political environment could be defined as chaotic, as highlighted by squabble inside the ruling party itself. Meanwhile, governance indicators have all deteriorated in the past decade, none of which are attractive for foreign investment (Chart 5).

The combination of deteriorating government fiscal situation and low growth prospect has refocused investor’s attention on the country’s debt sustainability. The South African government itself projects debt service cost will rise in the coming years, which if not tackled by fiscal restraint points to a significantly higher bond yield (Chart 6 and 7). And with the government expenditure burdened by the increasing debt-service cost overt time, the window of opportunity is narrowing for the government to correct its fiscal and bring the country’s growth rate higher through investment in real and human capital.

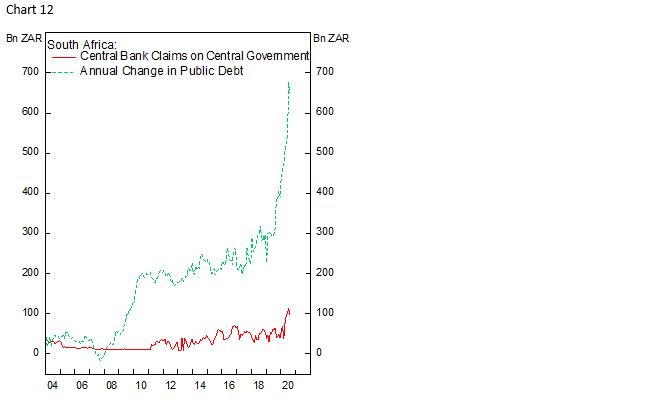

On a more positive note, the Rand is currently cheap and investors with high-risk tolerance should long the currency against the dollar (Chart 8). Inflation is well under control – despite the significant fall in currency – and the central bank’s easing cycle seem to be over (Chart 9). Rising commodity and mineral prices have also led to an improvement in South Africa’s terms of trade, which historically bodes well for the currency (Chart 10). As for the government bond, the investment case is not clear cut. Foreigners have sold off some 15% of outstanding government bonds while the central bank has been partially financing the government deficit (Chart 11 and 12), which may have kept yields elevated. South African nominal and real bond yield indeed is among the highest in EM, but the significant deterioration in the country’s fiscal outlook and lack of clear way out make the risk/reward of buying its government bonds unattractive.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.