Download PDF:

The rally in gold and silver prices this year has been impressive, although both metals have corrected somewhat. With the prospect of further stimulus still being debated, it is useful to revisit the thesis behind our bullish call on precious metals and reassess our portfolio positioning. First, let us start with the tailwinds:

- Money printing on the back of global central banks’ Quantitative Easing (QE) program to finance government’s deficit, which essentially is a form of fiat money debasement will lead to a weaker dollar. The aggressive easing of the Fed relative to other central banks and upturn in global cycle has historically coincide with period of dollar weakness, which is a boon for precious metals (Chart 1).

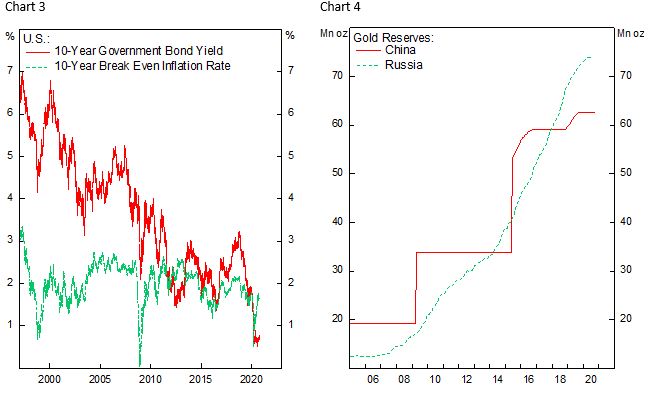

- As zero yielding assets that has a storage cost and minimal convenience yield – except for jewellers and manufacturers using precious metals as their product’s component – the current environment of negative real rates reduces the opportunity cost of holding gold and silver (Chart 2). Without a back up in bond yields, U.S. long-term bonds’ real yield will approach -2% as breakeven rate rises, pushing metals price higher (Chart 3).

- Precious metals act as a substitute for hedge assets, such as U.S. Treasury, which has experience reduced hedging capability due to its record low yields. Central bank reserves have been slowly shifting from U.S. dollar assets, which will benefit other currencies and gold. The transition is already happening in countries that deem U.S. hostility could potentially void their claim on reserve assets, such as Russia and China. Both countries have seen a marked increase in their gold holdings volume (Chart 4).

- Another force that often drive precious metals is the mania potential from an environment of low rates, easy fiscal and monetary policy. The difficulty in valuing these assets make them susceptible from forming a bubble. Currently, gold and silver price relative to U.S. money supply is still far below its mania peak in 2011 and 1980s, an argument supporting further upside of gold price in dollar terms (Chart 5 and 6).

Against the drivers outlined above, there are several headwinds to the bullish case for precious metals:

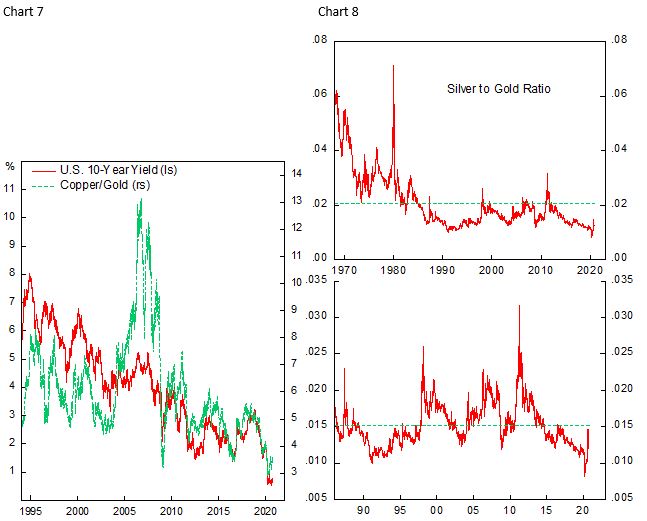

- Cyclical upturn has historically coincided with rising copper/gold ratio, which is at rock-bottom level currently (Chart 7). Although this could imply copper prices increasing faster than gold rather than gold price itself declining, the ratio is a reminder on the large gain gold has recorded this year.

- Declining equity risk premium and a back up in long-term bond yields would weigh gold advance. Gold performance has historically correlate negatively with real rates. A stable inflation expectation and rise in Treasury yield will halt advances in precious metals. Moreover, the silver/gold ratio seem to have a difficulty going up, an indicator that has historically useful as a proxy for mania sentiment in the market (Chart 8).

- The concern may seem premature, but an earlier than expected hawkish posture from the Fed regarding its policy rate increase or tapering of the QE program would send the dollar stronger and pop the bullish trend in risk assets and gold. This could result if the economic recovery is much faster, i.e. unemployment rate going below 4% and inflation shot up above 2% before 2023, a scenario that is far from the consensus today.

The bottom line is that the structural case for previous metals as a long-term holding remain intact, but an upturn in the global cycle and a backup in bond yields may first lead to a correction in prices, which have been bid significantly this year.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.

One thought on “Where Are Precious Metals Headed?”