Download PDF:

Recent weeks have seen oil price keeps on climbing despite the thawing tension between U.S.-Iran relation that potentially bring additional 1.5 mb Bbl/day supply into the market. We are expecting a continued strong global recovery this year and restraint from Saudi and Russia in ramping up production, as currently the two countries’ oil supply are still some 10% below pre-pandemic level but near their breakeven fiscal price.

Crude Outlook

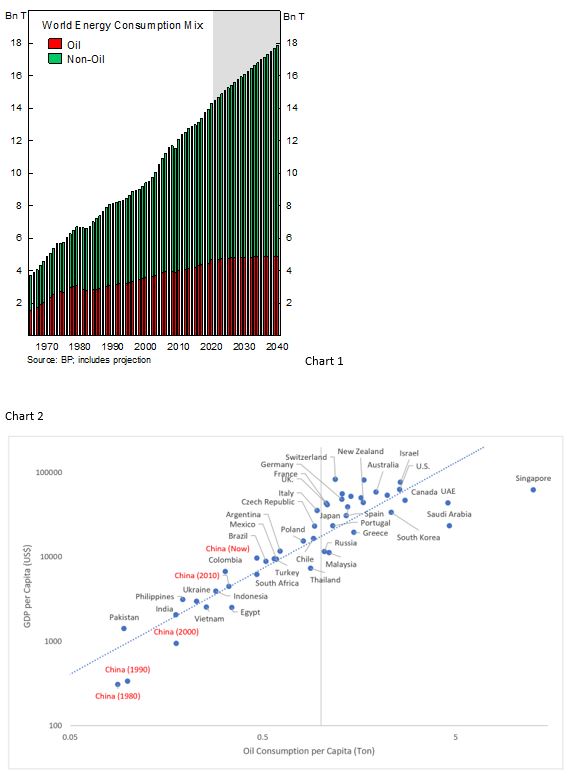

- In the long-term, oil demand will stagnate even from the fast-growing Asian countries (Chart 1). Most of the rise in demand in the past 4 decades has been from China. But even Chinese oil intensity is falling quickly as the country is becoming the world’s leading EV market (Chart 2). About 60% of global oil consumption is coming from transport sector. But in the short run, oil demand is “fixed” and does not vary by much, meaning the supply side is more important to monitor.

- Supply is not a problem, as global oil reserves are enough for another 50 years – assuming current level of annual production (Chart 3). What matter is the domestic economic situation of each country that in turn drives political incentive for OPEC+ to manage price. As country with the largest “inventory”, Saudi Arabia has the greatest incentive to not destroy the market.

- The political situation looks stable, for now. Russia, which has been more aggressive in pushing agreement with OPEC+ to ramp up output, is under less pressure to increase production as oil price is now trading above its fiscal breakeven (Chart 4). Meanwhile, Saudi has been willing to forgo its market share in global exports at the cost of its fiscal budget. But with current market price the country has the incentive to maintain stability and avoid direct confrontation with Russia.

In a hindsight, the price war last year makes sense, as Russia – which was in better shape than the Saudi in terms of fiscal balance and was trying to protect its domestic economy – was balking when being asked to curb production. The Saudi responded to screw Russia back by massively ramping up production, and even flood the market with oils from its reserves to “send a message”. Currently, the situation much different as rising oil price means producers do not have the incentive to offset declining price by increasing volume to meet their revenue target (fiscal needs, shareholders profit, etc.). But personally, I would run for cover once oil price shows weakness, as producers will be back on “fighting mode” by ramping up volume, causing price to spiral down and further incentivize them to offset it by rising production.

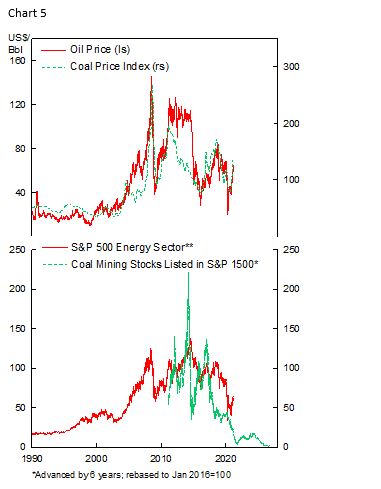

Expect better return on long oil price vs oil producers, which fits well with what happened in the coal sector decade ago. Today, coal price remains high because the world still needs it, but coal stocks have been crushed to nothing (Chart 5).

An Update of Russia

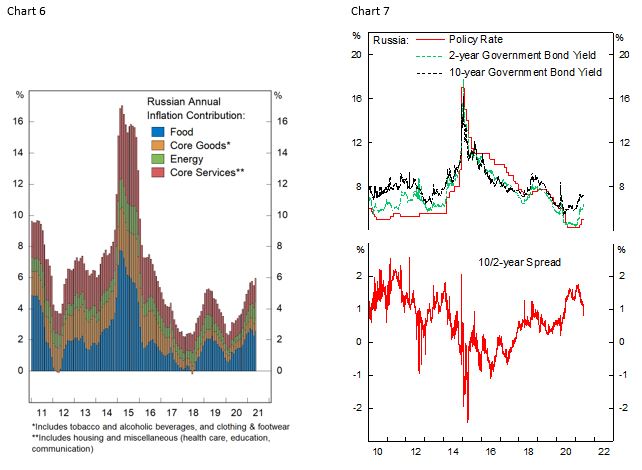

Last week Russian central bank resumed raising its policy rate by 50 bps, bringing it to 5.5% or 150 bps higher than its low last year. Russian economic activity has rebounded strongly in recent quarters, with manufacturing and services PMI consistently expanding since earlier this year, and the country is currently enjoying the tailwind of rising oil prices, which justifies the central bank to normalize its policy. Few observations are in order:

- The inflation number in May shows an uptick amid the rise in food price inflation (Chart 6), which we expect to roll down on a rate-of-change basis in the coming months. Various global agricultural products, such as soybean and grain, have been rolling over, and the Russian government has also kept its export restriction on certain food products to keep domestic prices low. In addition, recent strength in the Ruble should weighed down domestic prices for other goods.

- Russian assets and currency are still cheap, as discussed in previous piece (EMC_20210428) and should continue to do well in the coming months on the back of improving terms of trade and declining geopolitical risk. We are overweight Russian equity in EM benchmark and long the local-currency government bond, the later of which has shown 2%+ (update) gain since late April, when we initiated the trade.

- The markets have aggressively priced in a hawkish monetary policy setting going forward, while yields for the long end of the curve has been stable, which tells that spread of its long end bond is more than sufficient to compensate for the duration risk (Chart 7). Russian government is the least indebted in EM and its relatively high yield is very attractive compared to other EM countries with much weaker fiscal situation, such as Brazil and South Africa. We expect oil prices to remain high cyclically and the Ruble should catch up to improving terms of trade, which should bolster gain for our long bond position.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.