Download PDF:

U.S. Equity

We have a neutral stance on U.S. equity and think it is only slightly overvalued at current level (SPX: 3885 at the time of writing). However, we note that U.S. stocks are priced to perfection and will be vulnerable to bad news, on the back of expensive valuation and potential earnings growth disappointment, especially if corporate tax rate will be increased under President Biden administration. In the table below, we present our base case scenario for MSCI U.S. index (which has 100 points gap lower than S&P 500 level), from the perspective of forward and trailing expectation.

First, we expect multiples to contract to a more reasonable level amid recent rise in yield to 19 times for forward earnings and 26 times for trailing earnings, in-line with the upper range of historical level. Second, using a top-down estimate we projected forward earnings to grow 6.6% and trailing earnings to rebound to its 2019 peak. Multiplying respective multiple and earning projection at the end of the year results in an estimate for U.S. equity being 4.1-8.6% overvalued currently. Note that we are using a more optimistic scenario for our “base case” to account for the supportive fiscal and monetary policy environment, where President Biden is planning on another $3 Tn infrastructure spending and the Fed has new reaction function targeting average inflation above 2% and full employment.

U.S. 10-Year Yield and The Dollar

We hold the view that 10-year Treasury yield may top out rather soon, as market expectation for rate hike is already too hawkish relative to Fed’s dot plot. Employment is still far from pre-pandemic trend and average inflation is nowhere close to 2%, two criteria that has to be satisfied before Fed start raising rate. Moreover, term premium has risen dramatically in recent months and may soon peak, an indicator that has coincided with the peak in Treasury yield since post-GFC.

The attractive U.S. yield relative to other G7 countries, in turn, may soon be followed by foreign capital flowing to U.S. domestic bonds and drive up the dollar. U.S. long term yield hedged into JPY and EUR is now more attractive than the respective countries’ sovereign yield. Meanwhile, the faster inoculation campaign and much stronger fiscal support have led to U.S. growth outperforming its European counterpart, which is a tailwind for the dollar to rise.

Copper

In recent publication we have outlined our structural bullish case for copper and commodity in general, but recent price movement has resulted in an overbought condition and is due for correction. For now, we are flat on this asset class.

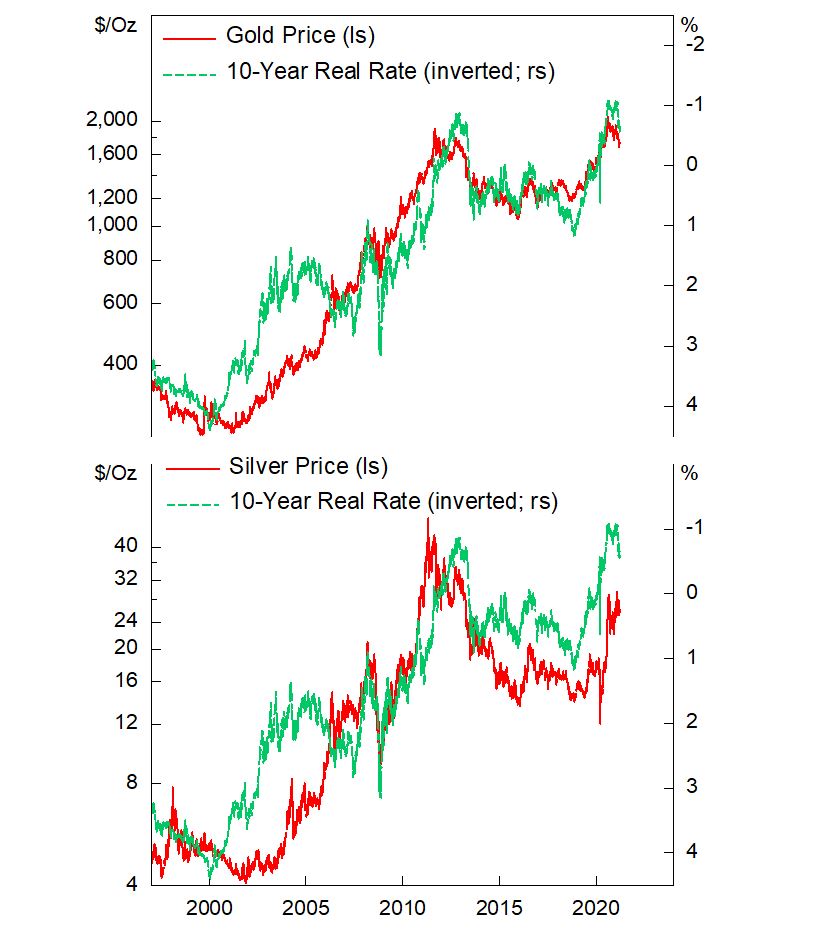

Gold and Silver

After the correction in precious metal, the overbought condition has largely eliminated, although the short-term outlook is rather mixed. On the bullish side, we are betting that Treasury yield is peaking out and will stabilize at 1.5% while inflation breakeven stays at 2.5%, resulting in real yield of -1%. This scenario would be consistent with gold at $1800-2000 range and silver at $35-40 range. However, potential rebound in the dollar could add pressure precious metal from going higher. In sum, we hold a positive medium-term outlook on both gold and silver but are warry of the spike in the dollar.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.