Download PDF:

For long investors have regarded Chile and Peru as one of the more stable Latam countries, as reflected in these countries’ borrowing cost and disciplined management of fiscal and monetary policy. Late last year, however, Peru went through a political crisis over the impeachment of former President Vizcarra by the Congress over corruption allegation, and the country saw three presidents within a week. The general elections next April could potentially be a pivotal moment for Peru’s political landscape and growth outlook, as the feud between executive and legislative branch in recent years has hampered investments in the country. So far, market reaction is muted and a radical shift in fiscal policy is unlikely, as marked by the country’s 10-year local-currency government bond yield being stable at 3.7% and the government was able to issue a 100-year USD bond at 3.23% yield just few days after the impeachment of the country’s president in November.

This report scrutinizes Peru’s structural development in the past decades, its cyclical outlook, and the risks culminating from domestic political instability and migrant crisis in Venezuela. We believe that the disciplined government and central bank policy will continue to support the country’s structural growth outlook and Peru stands to benefit from the acceleration of green energy demand, as discussed in a previous report. Meanwhile, we hold a more optimistic view that the political gridlock between the executive and legislative branch will lessen in the coming administration, as voters are likely to punish lawmakers that had been holding back necessary reforms in the coming election. As part of our overweight EM Latam vs Asia theme, we also recommend investors to allocate above benchmark weight for Peruvian equity to benefit from the improvement of the country’s growth outlook and cyclical recovery from higher commodity prices.

EM Growth Story and A Latam Anomaly

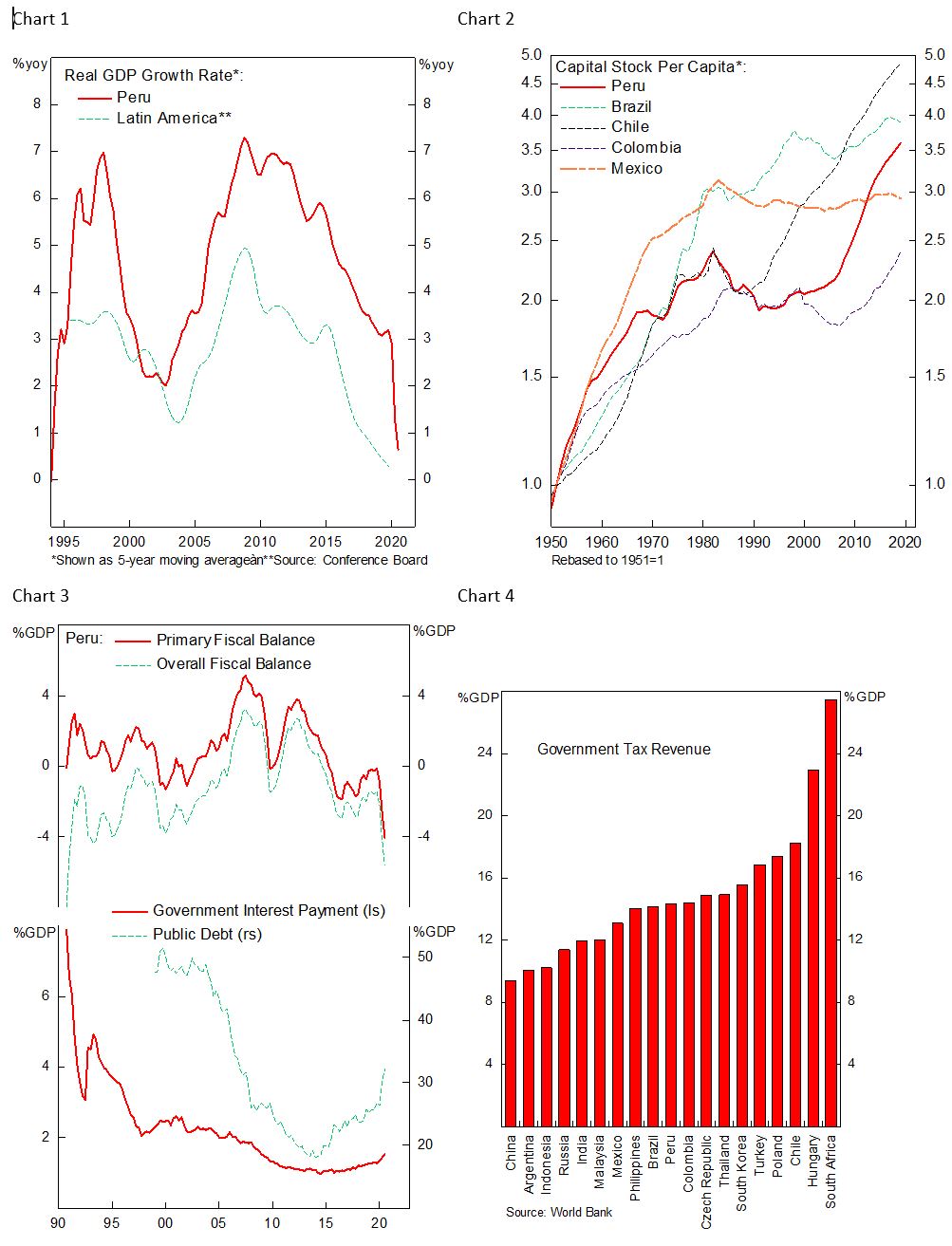

For a country in region mired by low productivity growth and constant crisis, Peru easily stands out and could be considered as one of EM countries where growth improvement is visible. The size of Peruvian economy has grown by 3.5 x in the past three decades, whereas Brazil and Mexico have less than doubled (1.8x) during the same period (Chart 1). This is partly contributed by the country’s disciplined fiscal and monetary policies that provide stability for the domestic economic and financial conditions, attracting FDI into the country and allowing faster pace of capital accumulation relative to other Latam countries that continues until today (Chart 2).

One notable feature with regards to fiscal policy is the country’s headline fiscal deficit ceiling and a debt ceiling of 30% of GDP, and a dual expenditure growth ceiling (on non-interest expenditures and on total expenditures). Although escape clause can be invoked in case of significant external shocks – which the country did during last year’s Covid-19 pandemic – the existence of the rule forces Peruvian government to maintain only a modest fiscal deficit and reign in public debt level, which had been in a downtrend from the turn of the millennium to 2015 (Chart 3). Last year’s 7.2% of GDP worth of fiscal support has accelerated the rise in public debt level to 33% of GDP, above the ceiling rule yet still among the lowest in EM universe, meaning that the government is constrained to provide large support to the economy in the medium term until public debt level decline below the ceiling or the ceiling itself is modified. To bring the country’s finances back into compliance, the government also announced Solidarity Tax to boost its tax revenue, which is aimed at the high earners and could raise PEN 300 million per month or 0.5% of GDP annually (Chart 4).

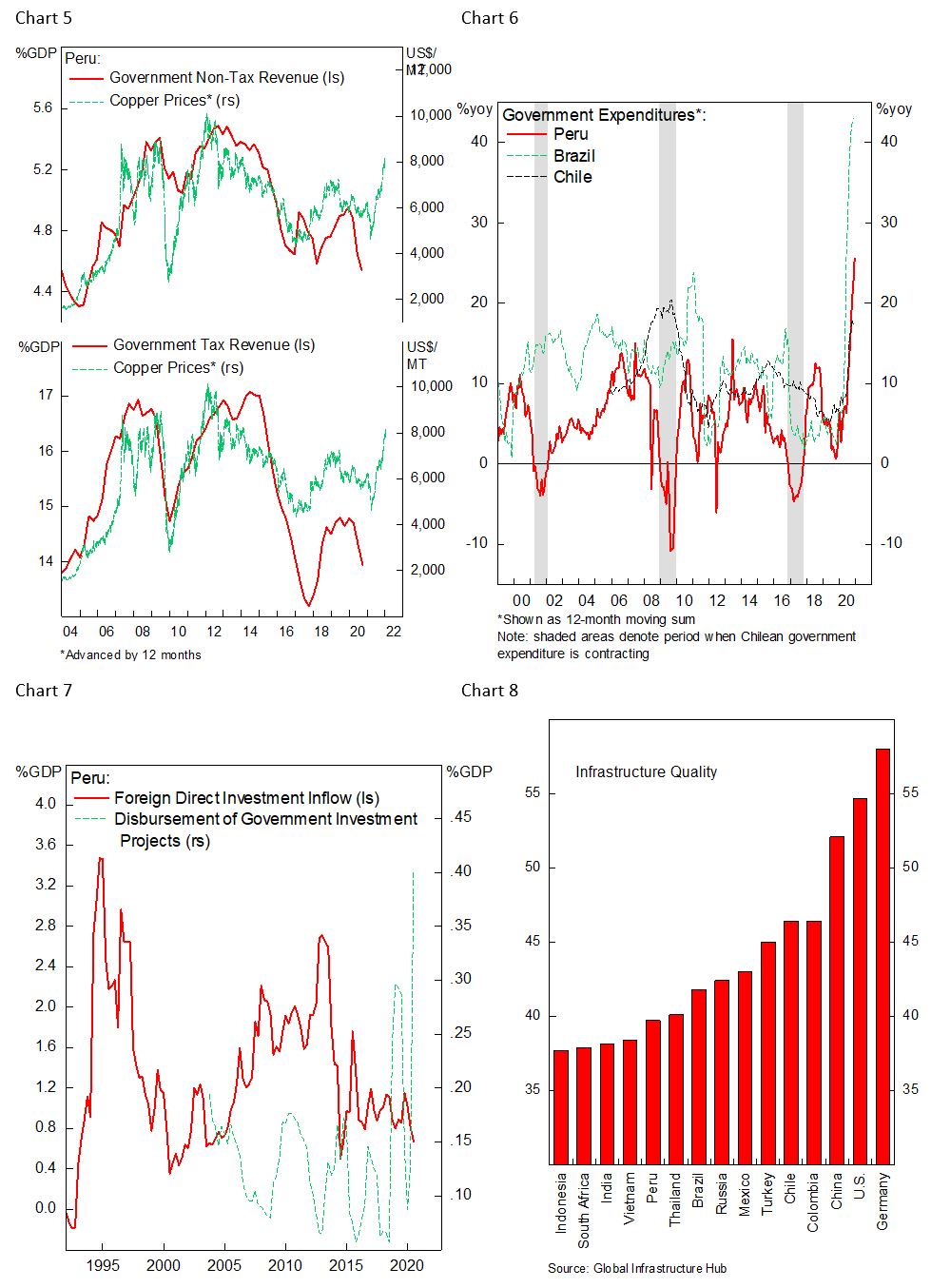

Although the deficit ceiling translates to the superiority of Peru’s fiscal health within the region, it also causes fiscal policy to be procyclical and amplify the volatility of growth that is already heavily tied to the commodity cycle (Chart 5). This means that during the downturns, not only tax and non-tax revenue will contract, but public investments and social spending also have to contract and become a drag on growth (Chart 6).

The fiscal limit significantly affects government’s ability to fund public infrastructure, leaving domestic investments at the mercy of Foreign Direct Investment (FDI) inflows, and restrict outlays on both education and health care spending unless tax revenue could also be increased. It is only in more recent years that Peruvian government has initiated a large-scale investment spending to fill the gap in investment needs and offset the decline in FDI inflows, but the amount is still far too low to meet the country’s investment needs (Chart 7).

First, Peru’s infrastructure quality is inferior compared to its neighbors and capital stock per worker still has much room to catch up (Chart 8 and 9). Similar case could be made for education and health care spending (Chart 10 and 11), which has resulted in a poor educational quality (Chart 12) and partly a reason for the failure to diversify the economy from primary goods extractions – the share of copper in Peruvian exports has continued to rise despite bear market in price in the past decade (Chart 13). The high urbanization level (80%) makes it even more crucial for the government to diversify its economy and reduce unemployment in the city, where job opportunities tend to reside outside primary goods extraction.

More urgently, reforms over labor law are needed as the country’s labor informality reached 70%, far above its Latam peers (54%), amid stringent labor regulation that prevents firms from hiring more full-time employees when companies reach the threshold of 20 employees. As a result, the lower bargaining power of part-time worker has depressed wages amid the productivity surge in the past two decades (Chart 14).

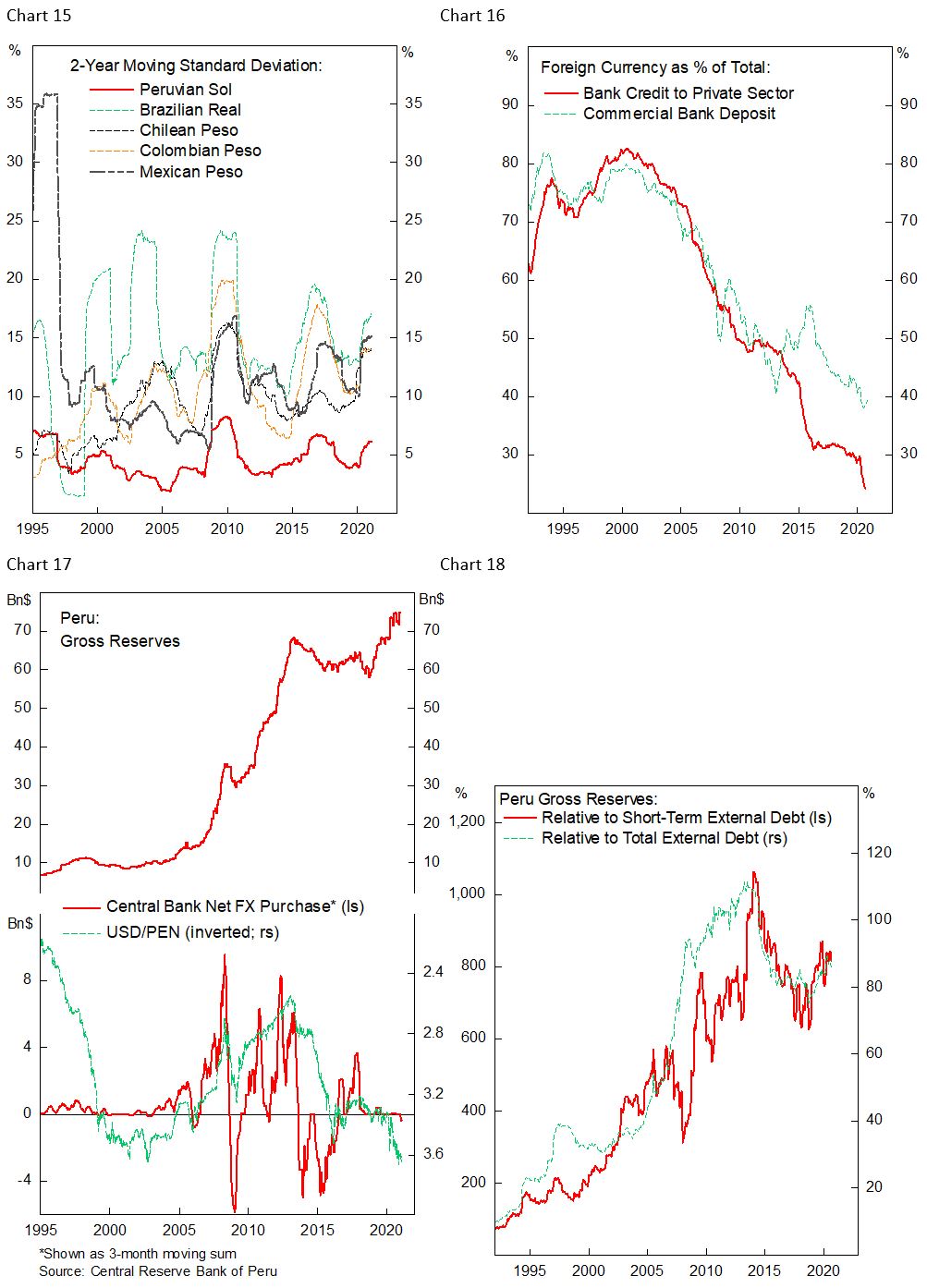

In terms of monetary policy, Peru’s managed floating regime has provided stability for the Sol and reduce the risk of currency mismatch in the financial system (Chart 15). Despite efforts to reduce the dollarization of the economy, sizable portion of Peru’s credit and deposit is still denominated in foreign currency – mainly the dollar – that increase the risk of illiquidity and insolvency in the financial system when the PEN significantly depreciate (Chart 16). This points to the necessity for the central bank to accumulate foreign-currency reserves as war chest during the downturn (Chart 17). Chart 18 and 19 show that Peru’s FX reserves has been rising relative to external debt, and its coverage of foreign-currency debt is among the highest in EM. In addition, the credibility of its central bank and anchored inflation expectation should translate to stronger domestic currency in the long run to reflect higher productivity growth (Chart 20). Our fair value assessment shows that PEN is currently 5% undervalued (Chart 21), and cyclical rebound in global growth should bolster the currency further.

Lights At The End of Tunnel

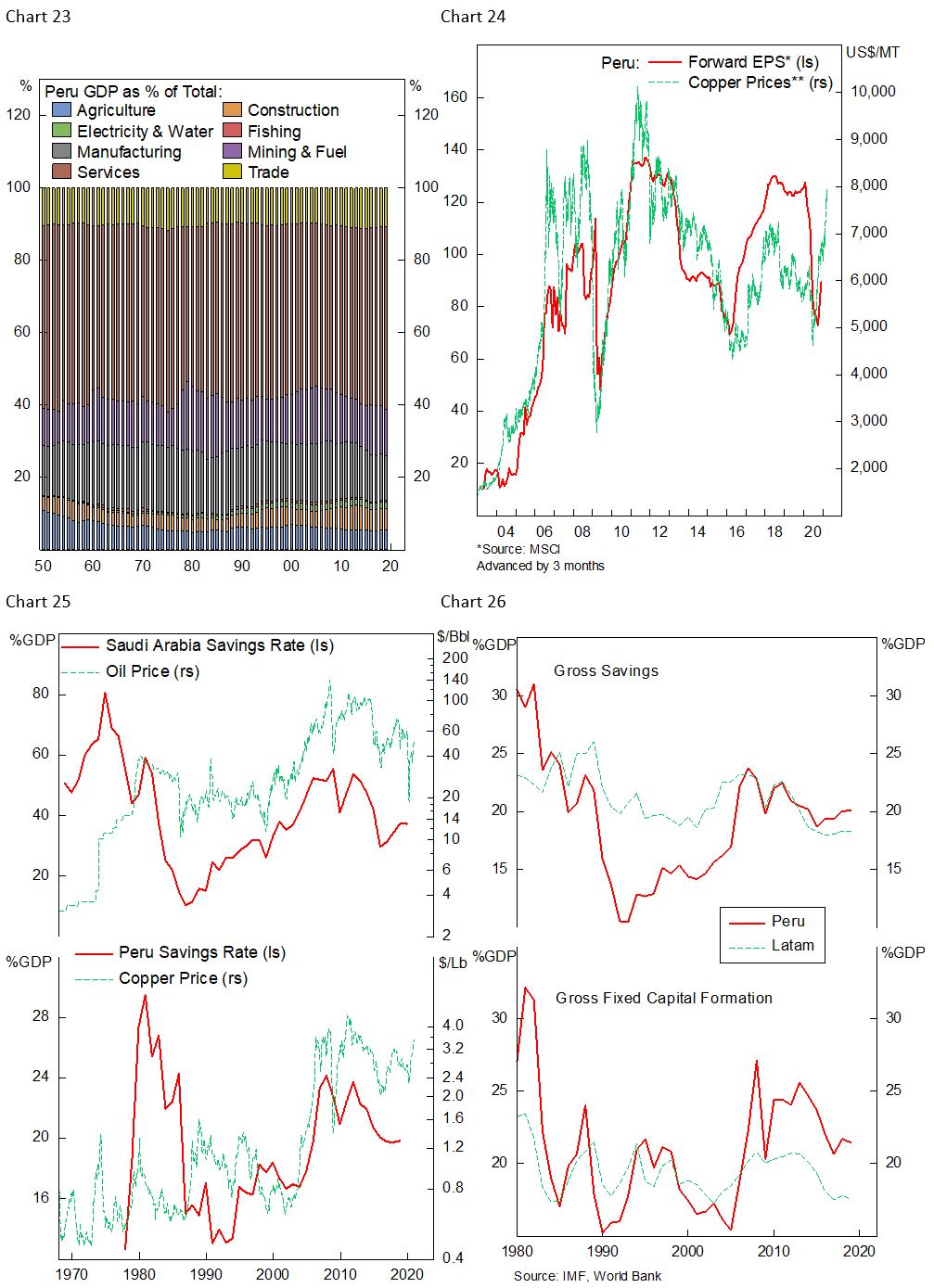

The bear market in commodity prices the past decade has been a major drag to Peru’s growth and exports. Similar to other Latam countries, Peru’s development is tightly linked to global commodity demand, which accounts for a fifth of the country’s GDP and 70% of its total exports (Chart 23). Cyclically, a broad-based dollar weakness and improving global growth outlook will likely continue to boost the metal’s price higher, which in turn, will boost Peruvian terms of trade and equity earnings, the later currently still a third below its recent high (Chart 24).

Over the longer-run, strong growth of base metal demand from green energy demand bodes well for the country’s growth outlook, terms of trade, and asset market, all of which are centered around copper production. Peru currently produced about 2.4 Mn Tonnes of copper or equivalent to a tenth of global production figure, and rank as the country with third largest copper reserves, after Chile and Australia. The rising strategic importance of copper in new energy infrastructure should also translate to increasing geopolitical importance of copper-producing countries, potentially lifting their status and wealth to those of oil-producing countries in the 20th century.

In such case, the rise in copper prices will lift domestic savings rate – similar what happened in 1980s when copper price doubled and those for gulf countries (Chart 25) – and bolster investments over the long run. The large investment needs for transportation, energy, education, and health care mean the rise in savings will not be exported out but rather be used to develop domestic infrastructures (Chart 26).

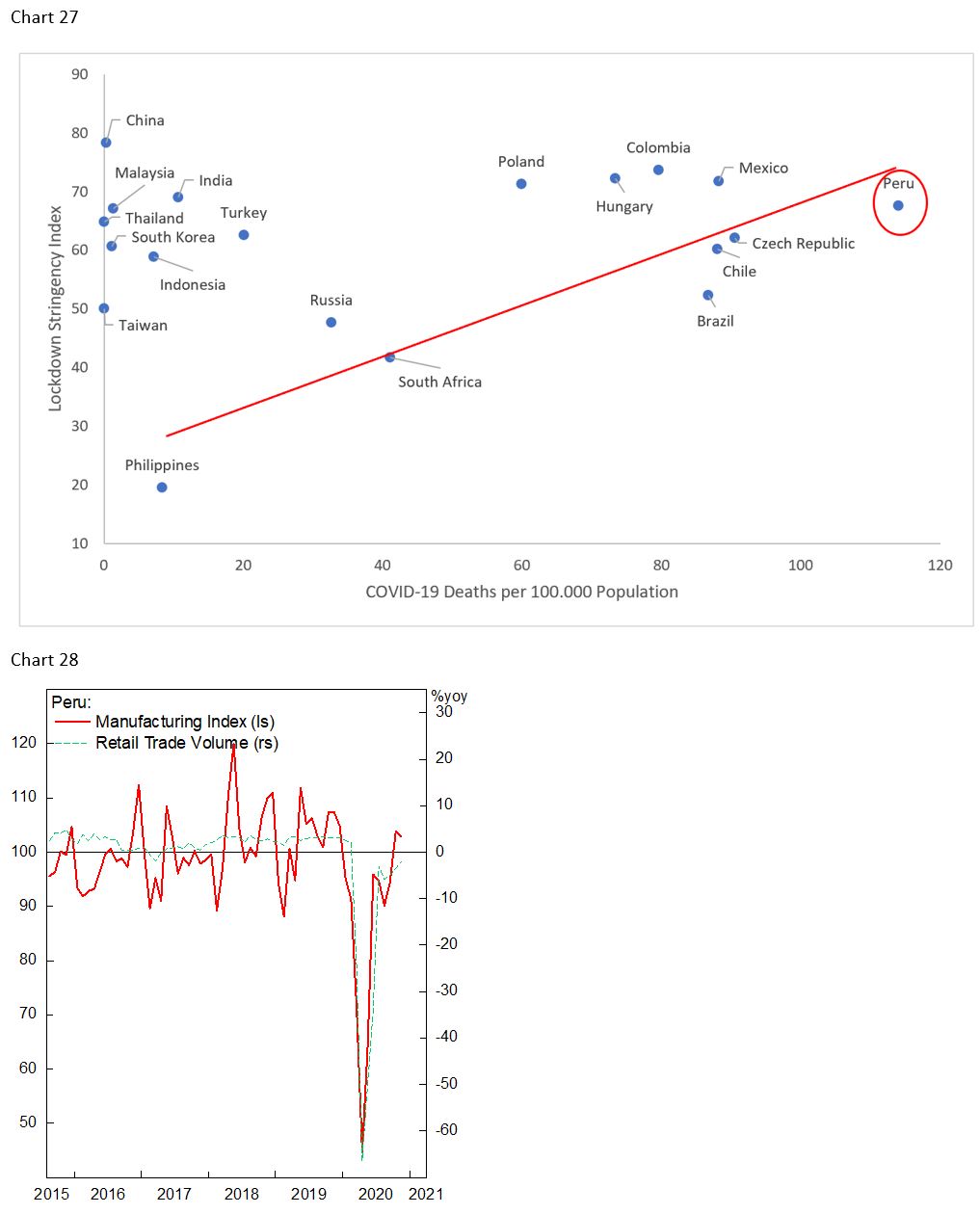

Lastly, Peru suffered the most from Covid-19 pandemic in terms of deaths per capita and economic damage (Chart 27), which make the case that a rapid distribution of an effective vaccine could help the country quickly reach the threshold for “herd immunity”, supported by the already high infection rate among large portion of the population. Currently, Peruvian manufacturing activity has rebounded above pre-pandemic level while retail trade is still slightly below last year’s level, both of which will be further aided by inoculation of the country’s citizen (Chart 28).

A New Hope?

The battle between the executive and Congress over anti-corruption reforms, ending parliamentary immunity, and the issue of illicit campaign finance will continue to dominate the political debate of the next Peruvian government. Last year’s political drama related to the impeachment of former President Martin Vizcarra over corruption allegation by the Congress will continue to color Peru’s presidential and congressional elections starting in April, with candidates supporting the country’s anti-corruption drive likely enjoying popular support (Chart 29). Over 80% of the public believe that the impeachment of Former President Vizcarra was motivated by political or personal interests of the congressmen – half of the lawmakers are under criminal investigation – and disapprove the Congress decision to impeached former President Vizcarra. This will likely be reflected in the elections results, with Accion Popular and Fuerza Popular, two party that support the impeachment and the later led by Keiko Fujimori and a known opposition of Vizcarra’s government, losing their seats in the Congress.

There are hope that voters will ouster lawmakers that were supporting the impeachment and vote for those that supports the anti-corruption drive, which will foster unity to support the difficult but necessary reforms. The current weak party system, where none dominates the political landscape, means that Peruvian democracy often stumble over needed reforms. In the short term, corruption and political instability risk will remain the top in investors’ mind and these two factors will affect the execution of large investment projects, which has been delayed in past years and became a drag on growth.

The political and humanitarian crisis in Venezuela has resulted in displacement of its population to neighboring countries, with Venezuelan migrants living in Peru now equal to 2.5% of Peru’s population. This has added strain on the country’s already poor health care and education system and stoke resentment among the local population. A continuation of global sanctions against Maduro’s regime in Venezuela will only worsen the humanitarian condition of the region and put extra burden on the neighboring countries, especially to Colombia, Peru, and Brazil. This could widen political polarizations in the region and lead to the rise of populist leaders whose policies tend to erode institutional strength and proved to be unsustainable in the long run.

Investment Conclusion

The continued improvement in Chinese economic outlook and growth rebound in the Rest of World should mean that commodity demand will remain strong this year, providing a tailwind to commodity intensive Latam countries. Meanwhile, easy Fed policy, continued dollar weakness, and low investment in the mining complex should provide support for base metal prices to advance further and boost the country’s equity earnings at a time when its valuation remain modest compared to the excesses in developed market bourses and growth stocks. Investors should long Peruvian equity (NYSE: EPU) to benefit from the cyclical improvement in global economy and potential structural bull market in commodity prices. Chart 30 shows Peruvian cyclically adjusted P/E is currently trading at 17 times earnings – below historical average and is skewed higher due to lower EPS from depressed copper prices in the past decade – and has not priced in the strong rebound in EPS this year and potential structural bull market in base metals. Relative to EM benchmark, Peruvian equity’s forward P/E ratio is trading only at par (Chart 31), setting the stage for an outperformance in the coming years should the dollar continue to slide and drive metal prices higher.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.