Download PDF:

I) Turkey: Back to Coma Again?

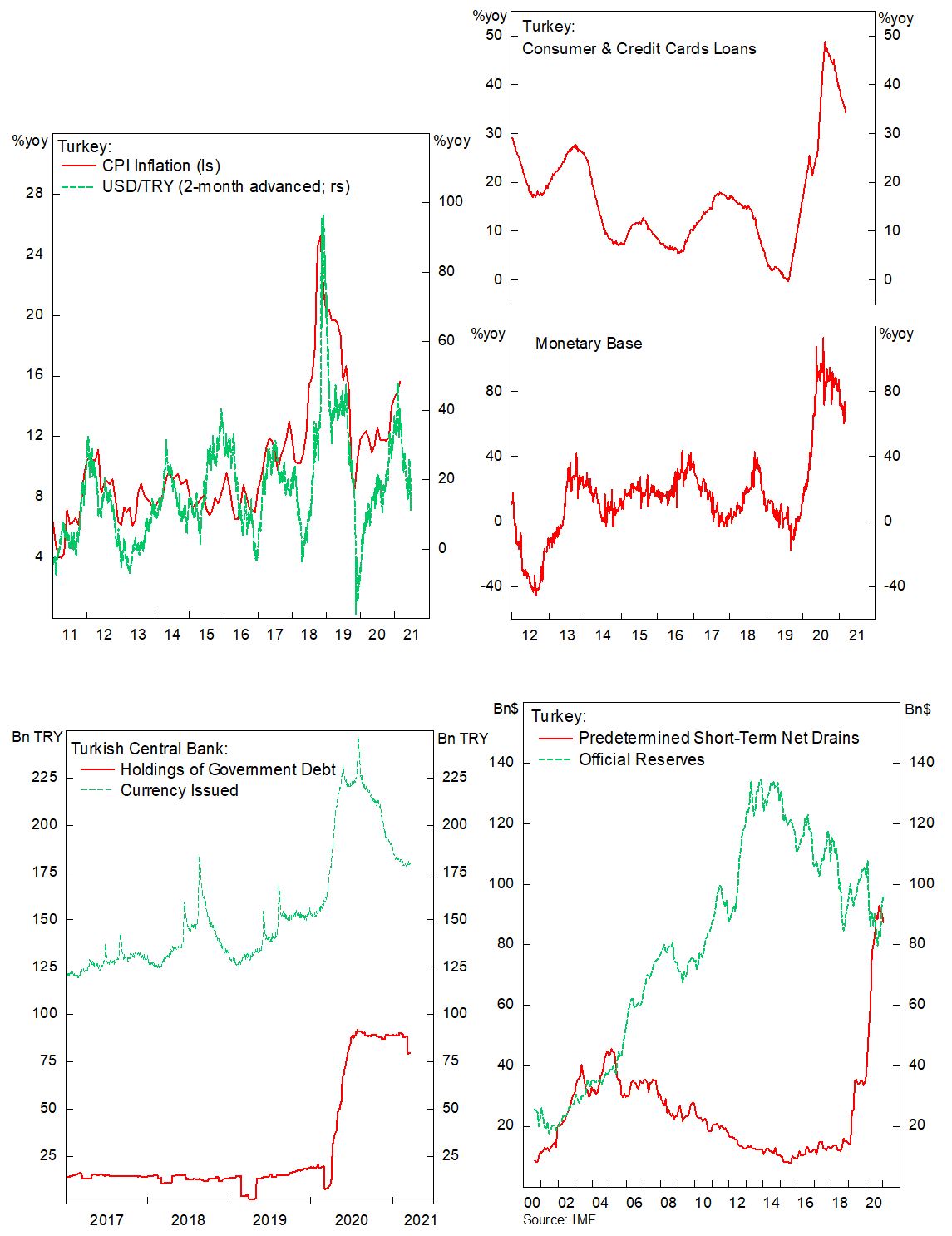

Various indicators were still flashing red even before President Erdogan fired Naci Agbal – the central bank governor he appointed just four months ago – for pursuing a hawkish monetary policy. Although his firing of Mr. Agbal is akin to shooting himself in the foot and undermine the credibility of the central bank further, we think a drastic increase in interest rate is also not be justified by domestic conditions and may inflict damage to the domestic recovery. With the market already went to a riot last week, what should investors do and how further low could the Lira and Turkish stocks depreciate? In our view, Turkish assets will stay volatile in the short-term and the country will undergo through a similar situation as in the 2018 crisis, when monetary policy was tightened abruptly to quell inflation, with few notable differences:

- First, Turkish foreign-currency reserves situation has worsened. The Lira has depreciated another 10% against the dollar since the through in 2018, making it harder for domestic firm to service their foreign-currency borrowing, and the Covid-19 crisis has hit Turkish corporate hard. Previous effort to prop up the Lira has drained the country’s inadequate reserves, with gross foreign-currency reserves declining from $80 bn in the middle of 2018 to $52 bn currently, while short-term financing needs rose dramatically – this, however, includes $45 bn in swap transactions, such as the $15 Bn swap lines with Qatar central bank initiated last year, which could be rolled over. We are watching Turkish FX reserves closely in the coming weeks for signs of the central bank intervention in TRY – a negative red flag.

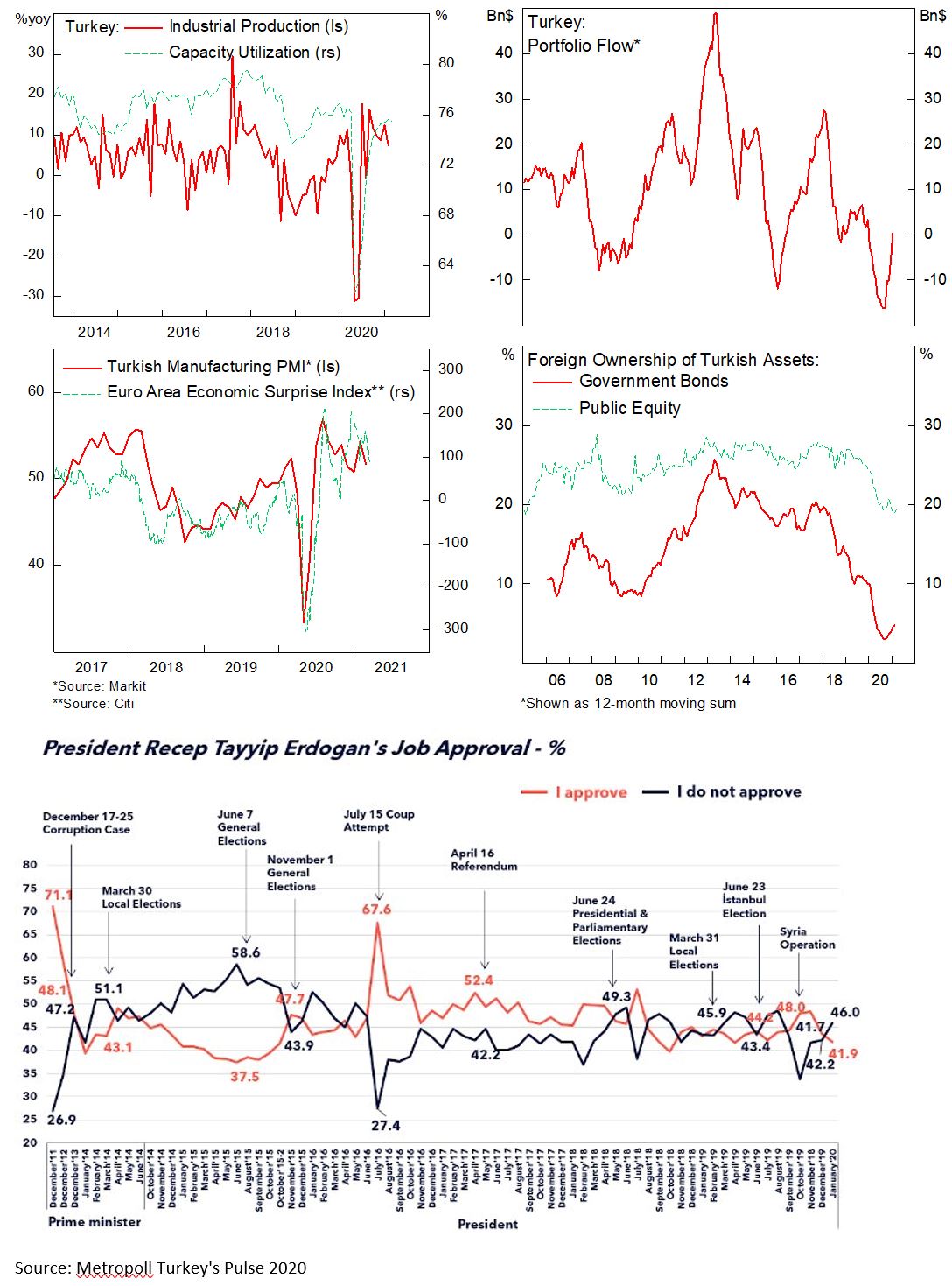

- Second, the drastic monetary tightening through interest rate hike and previously stronger Lira may start to bite the still fragile domestic economic recovery. Credit growth has peaked out and money supply is contracting. However, unlike in 2018 when global manufacturing was already in decline amid the trade war and European growth was weak, the current situation is more supportive. The world’s manufacturing sector is still recovering post-pandemic and economic figure coming out of Europe is still registering positive surprises, which should support Turkish exports. This combination should result in a milder growth slowdown this year relative to the 2018 crisis.

- Third, President Erdogan is increasingly unpopular among Turkish people. His popularity has been in a steady decline – amid economic slowdown, involvement in war in Syria, clash with Europe over refugee issues and Greece, among others – and he is losing control; in 2019, the ruling AKP party lose its control of Istanbul, the capital, after 25 years of domination. It is too early to tell whether President Erdogan has learnt his lesson from the previous crisis. For now, fiscal support has been tapered and there is minimal need for a new stimulus as the inoculation campaign continue and restrictions are eased, while money supply has fallen, and credit binge was phased out in the past quarters. Going forward, the worry is that President Erdogan will relaunch its credit-fueled growth policy to serve its political goal, which may lead to the vicious cycle of weakening Lira and rising inflation.

- The good news is that Turkish assets are trading at battered down valuation and majority of foreign capital has flown out in the previous debacle, which limit the potential surge in capital outflow and further Lira decline. Turkish equity is now trading at 5.8 times forward earnings and 1 time book value (vs 8.5 times forward earnings and 1.5 times book value in the beginning of 2018), the lowest in the world, and the Lira is 30% undervalued in real effective terms, according to our fair value estimate. Much of the pessimism has already been reflected in the country’s asset prices, and a violent rally could happen if President Erdogan err on a more conventional fiscal and monetary policies.

The bottom line is that risk remains very high, and it is too early to bottom fish Turkish assets amid the still poor fundamental picture. Investors should monitor the development of the country’s reserve situation and next month’s monetary policy decision to see whether the central bank is still committed to bringing inflation down to its target.

II) EM Policy Normalization

Expectation for policy rate hike is mainly concentrated in the more fragile EM countries, with Brazil, South Africa, Indonesia, and Russia among the top candidates. We see the policy rate hike as a normalization process as economic activity accelerates and interest rate was cut aggressively last year, which brought real policy rate to historical low level.

- The historical precedence is not encouraging for EM equities, where policy rate hike has historically coincided with poor stock performance. There is a 6-month lag between the peak of our policy and LEI diffusion index before the stock market topped. In addition, EM countries’ bourse are no longer cheap with valuation multiples above its 50th percentile for most market and historically EM stocks have never had 2 consecutive years without an above 20% correction.

- In the past, a strong global – and U.S. – economy has always led to the fear of Fed rising its interest rate, which most of the time was followed by period of volatile equity market, especially for EM. However, last year the Fed changed its reaction function and pledged to not raise interest rate until the economy see full employment and average inflation above 2%. This means the dollar may resume its downward trajectory – a boon for EM stocks – and lift commodity prices higher, benefitting commodity-sensitive Latam countries.

- Earnings are poised to grow strongly in the coming quarters, which may offset the potential decline in multiples. EM equity should continue to do well, at least until the third quarter this year. It is too early to cut exposure to EM stocks, but investors should rotate from the high-flying growth sector to the still-cheap value.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.