Download PDF:

Stay Positive on Brazilian Assets

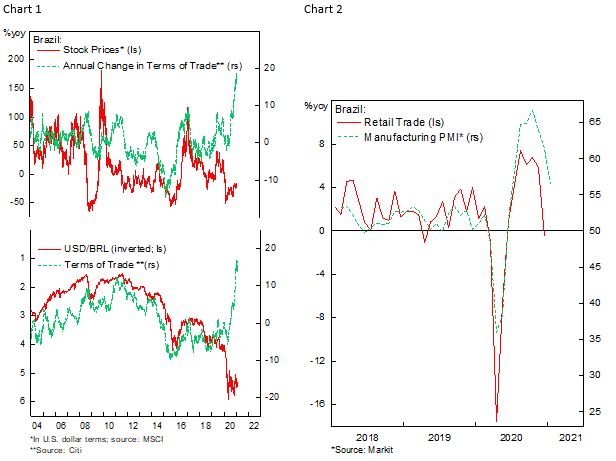

- The backdrop for Brazilian assets remains bullish amid rising commodity prices and undervalued Real (Chart 1). In addition, Brazilian economy has recovered strongly and various indicators – such as manufacturing PMI and retail sales – are now back to pre-pandemic level (Chart 2). With the global economy continue to recover and lockdown restriction likely to be eased as the number of cases decline, commodity prices should continue to rally and provide a tailwind to Brazilian assets.

- The sharp rebound in economic activity last year was aided by large fiscal support and the central bank cutting rates to record-low level. Going forward, the risk lies in the ability of Brazilian government to scale back its fiscal support without causing significant damage to the pace of economic recovery. As the government resources are depleted and President Bolsonaro is facing re-election next year, the political will to continue with market-friendly reform program is currently low, which may become a drag for Brazilian assets. Already, Bolsonaro’s decision last week to replace Petrobras executive to curb increase in gasoline prices – and appease the population – spook the market. The pandemic-related stimulus last year has been widely popular and increase the approval of President Bolsonaro, but with the government fiscal being constrained government policies will likely be becoming more erratic.

- Lastly, Brazil’s policy rate is likely among the first to be hiked, with the market expecting 50 bps increase in the coming 3 months and 100 bps rise within 6 months (Chart 3). Currently, Brazilian real policy rate is negative and among the lowest in EM – the country’s policy rate is at 2% and headline inflation has risen to 4.6%, although core inflation has remained stable at 2.7%. We expect the tightening in both fiscal and monetary policies as a normalization process as the economy recover from the pandemic damage, and the later may increase the attractiveness of BRL, which has not appreciated as strongly as other EM/Latam currencies since the through last year.

Turkish Equity Should Outperform

- The fundamental problems that cause the Lira to plunge in recent years are being gradually corrected, with official reserves rising alongside the TRY in the past few months. In its last monetary policy meeting the CBRT remains committed to bringing inflation down to its target of 9.4% by year end and 7% by 2022. Both the new central bank governor and finance minister have delivered hawkish commentary on achieving price stability and policy rate will likely remain high in the medium term, which should provide a floor for TRY (Chart 4). Granted, the country is not out of the woods just yet, but the tailwinds from global economic recovery and liquidity have significantly lowered the risk of another crisis.

- Another encouraging signs for Turkish assets come from the return of foreign capital. Despite the still fragile confidence on government policies, foreign investors have bought $9 Bn of Turkish bonds in the past six months (Chart 5), lured by the high yield of Turkish government bonds. Meanwhile, inflation should come down in the coming months – driven by stronger Lira (Chart 6) – and push bond yields further lower, which will make Turkish stocks more attractive.

- Finally, valuation for both Turkish stocks and the Lira are cheap – despite the recent rally – and its asset prices trail significantly relative to EM overall (Chart 7). Turkish Lira is 25% undervalued, according to our fair value estimate, and should benefit from the recovery in European manufacturing sector, its largest exports market. More importantly, Turkish stocks are now among the cheapest in the world and trading at only five times cyclically adjusted P/E ratio, while EPS is set to improve, all of which limit the downside from current level.

Appendix

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.