Download PDF:

5 Signposts for Global Equity Recovery

The decline in DXY of late has arguably help global equity grind higher amid easing financial condition. For long, we have been highlighting the widening valuation between U.S. equity and the rest of the world, which has gone much cheaper post-COVID19 correction. In-line with previous crisis experience, we believe a rotation between value and growth stocks will inevitably happen, compounded by the regulatory and privacy issue surrounding big tech firms and advertisers rethinking their online marketing strategy through social media. There are five things in our mind to assess the risk/reward in global and U.S. equity:

- Fiscal support from the U.S. government, including the extending the Paycheck Protection Program. This will likely support household spending and prevent domino effects in the economy from a fall in consumer confidence. In the long-term, however, investors will eventually reassess the debt sustainability of each country, especially emerging markets, and demand high country risk premium from highly indebted countries, such as South Africa, Brazil, and India. This means that yield or valuation multiple for several countries will not go back to their pre-COVID-19 level.

- Loose monetary condition supported by Fed’s expanding balance sheet and continuation of dovish forward guidance. So far, Fed Chair Powell has been very dovish and likely to remain so after an overly tight policy in the middle of last year. Meanwhile, EM central banks have been widely supportive of the economy and cut rates aggressively amid low inflationary pressure.

- Curbing the spread of COVID-19 globally to suppress R0 below 1, allowing lockdown restriction to be lifted on a sustainable basis. This would be the key for economic activity to resume normally, until a viable vaccine candidate is approved and widely distributed. An elimination of the virus, which is not impossible, as China, Taiwan, New Zealand, and other countries have shown is paramount for the long-term outlook of risk assets.

- Continuous fiscal support and credit growth in Chinese economy, driven by infrastructure spending. Total Social Financing of late has been surging significantly on the back of LGFV issuance and strong credit growth, which acts as a direct stimulus in the Chinese economy. More important is the shadow banking sector, which serves as the backbone of credit for many SMEs.

- Banking sector resilience. Although so far capital ratio among Global Systemically Important Banks (GSIB) is still above BASEL III requirement and loan provisioning seem to be manageable relative to capital base, non-performing loans (NPL) are likely to grind higher in the coming quarters as businesses ran out of announced fiscal support. In a base case of 4% hit (10% default rate and 40% recovery rate) to banking capital, it is likely that many will have to raise equity capital or reduce their lending activity significantly, worsening the situation.

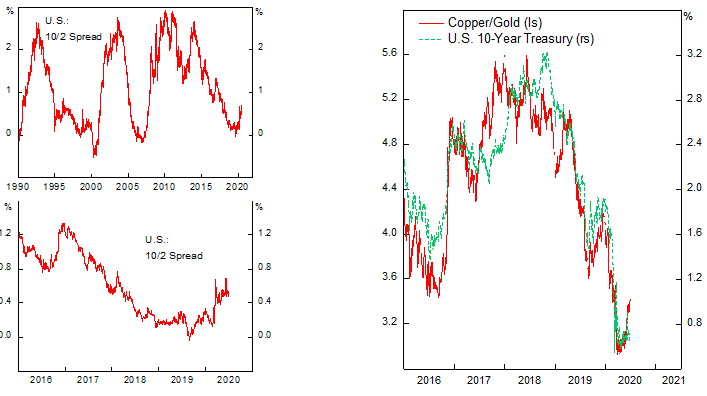

And what about Bonds? Have we seen the through in yield? Bond yield and the economic cycle goes together. For the current cycle, we think 10-year bond yield has seen its low and likely to rise as the growth outlook improves, which depend on the five signposts mentioned before. The yield curve has steepened significantly, and further upside is the path of least resistance. At the same time, copper/gold ratio has started to pick up and may be followed by 10-year UST yield in the coming weeks. Our target for the next 12-month period is for yield to go around 1.5%. Few major risk that may hinder our base case scenario includes a revival of the COVID-19 spread in Winter 2021, intensifying conflict between U.S. and China related to Taiwan, and geopolitical risk related to Iran, North Korea and other ME countries.

Turning Point in The Global Commodity Cycle?

For the past few quarters, we have turned increasingly bullish on commodity prices due to both increasing demand from China and other EM countries’ infrastructure projects and underinvestment in commodity-producing firms in the past decade, on the back of easy monetary policy. We think a rotation is in the making, as relative valuation for EM/DM and growth/value has reach its extreme. The catalyst we are looking for is further dollar weakness.

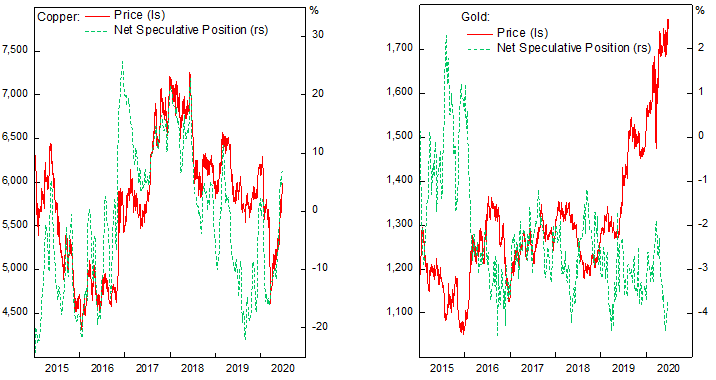

- There are few reasons we think the dollar will go down further. First, Federal Reserve commitment to stay on the easing path and loose monetary policy for the coming two years is relatively more dovish than its European and Japanese counterpart. Second, there has been an explosion of money supply, which reduce the value of fiat money and boost the prices of real assets, including stocks, property, and commodities. Many investors have made a bullish case for gold on the back of inflation fear and devaluation of fiat money, but we think copper is a more interesting play. First, as a real asset copper prices benefit from dollar weakness, similar to gold. Second, copper and gold prices have move in a cyclical basis following the global cycle, which currently favor copper/gold ratio moving higher.

- Excluding oil, there has been underinvestment in the commodity complex in past decade, which will likely result in supply constraint if demand recovers strongly. Commodity inventories, ex-oil & gas, have been declining prior to the COVID-19 shock. We agree that inventories for many base metals have been rising amid the pandemic, but this has resulted in many producers halting its operation or even shutting down mines, which will become a supply bottleneck when the economy grind faster and demand for base metals strengthen. This will be especially explosive if, as we believe, government around the world will stimulate their economy by ramping up infrastructure spending. This should be a boon for both steel and copper.

If our thesis is proven to be correct, the Latam region will benefit most and investors should accumulate both the region’s equity and currency gradually. Our model shows that Brazilian real and Mexican peso are currently about 20% undervalued, based on their Real Effective Exchange Rate, while Chilean peso is about 10% undervalued. In these countries, valuation multiple is below historical average and especially depressed for both Mexico and Chile. We have a leveraged position on Mexico, which we think will deliver multiple baggers to our invested capital in the coming 18 months. The country also benefits from reshoring of manufacturing base away from China due to its proximity with the U.S. and USMCA trade deal.

The table below shows the drawdown of each country equity market from its 2-year peak, P/E and P/B multiple, and their respective percentile since 1996. More than half of EM countries have a weighted percentile below 50%, meaning that valuation is currently below its historical average. Moreover, there are eight countries with P/B value trading close or below 1x, underscoring the limited downside risk from current level. Our top picks include Chile, Turkey, Philippines, Indonesia, and Mexico, due to cheap valuation and diversified equity market.

Should the dollar fall and commodity cycle rebounded, EM will finally outperform DM and rotation is inevitable. Investors should start accumulating the winners and avoiding the losers. In the past decade, many firms in commodity-sensitive countries have been undergoing a deleveraging campaign and painful adjustment amid lower commodity prices, which have led to a stronger balance sheet and elimination of high cost producers.

- Commodity net importer will be hurt by rising prices, among them China, India, Turkey. Deteriorating terms of trade will be reflected in a narrowing trade surplus or widening of the deficit, which may weight the currency in these countries and the need for Central Bank to maintain a hawkish monetary policy.

- Among commodity-producing countries, there are obvious winners:

- Copper – Chile and Peru. Copper is likely to be the biggest beneficiaries from global growth improvement and monetary stimulus. Copper/gold ratio is recovering from an all time low and further upside is likely. Chilean equities’ valuation has been drifting significantly lower in the past few years and is trading at a depressed level (1.1x P/B value). Moreover, Chilean stocks have been trading at a ”discount” relative to copper prices of late.

- Oil – Russia, Colombia, Mexico. The prospect of oil-producing countries is more uncertain, as the U.S., Russia and OPEC could all ramp up output if oil price increased significantly above their production cost, leading to another round of prisoner’s dilemma between these countries. These countries’ stocks and currencies are very sensitive to the development in oil prices, highlighting the need of high oil prices for the bull market to be sustained.

- Iron ore – Brazil and Australia.

- Coal, nickel, and palm oil – Indonesia, Malaysia, and Australia

Commodity in the 21st Century: Chip Wars

In the world history, countries and tribes first battled using troops and swords, which then evolved into gun in the 13th century and finally reached nuclear power in the World War 2. In this century, the battleground is in the technology sector and involve information warfare, including in the high-tech semiconductor industry and industrial espionage. And whereas oil used to be the highly prized commodity due to its crucial need for the Developed Economy, today the priority shift toward semiconductor chips, which are used in many electronic products including military equipment. Few observations related to the current market and geopolitical development:

- U.S.-China rivalry is intensifying, and the technology sector is becoming the battleground between the two giants. Following U.S. restriction on chip exports to Chinese hardware producers, there has been a strong push from Chinese government to develop a local champion on chip manufacturing, highlighted by the recent spotlight on SMIC of late. Although China is now still lagging behind Taiwanese and South Korean manufacturers, it is likely that China will play catch up in the long-term, supported by government push toward indigenous innovation. DRAM prices will face a structural headwind in the long-term due to rising competition from China, although current leaders benefit from growing demand from both U.S. and China. TSMC’s decision to open a new factory in U.S. is likely to appease the U.S. export rules while its Taiwan-based factory utilized for manufacturing chips exported to China.

- South Korean stocks have been particularly hit hard while Taiwanese equities have benefit from the U.S.-China rivalry, led by TSMC. South Korea is an end-manufacturer of electronic products, which use chips in its computer, graphic cards, computer, video console, etc. Meanwhile, Taiwan (TSMC) is perhaps the most important semiconductor (which DRAM is a type of it) manufacturer in the world. The jump in DRAM prices in 2017/18 likely increased the input cost for companies like Samsung, which is consistent with their significant decline in margin last year, while benefitting TSMC. Going forward, correction of DRAM prices of late will benefit end-producer such as South Korean firms and hurt the margin of chips manufacturer, including Taiwanese stocks (TSMC).

Copyright © 2020, Putamen Capital. All rights reserved. The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.