This research paper is prepared by and is the property of H-o-l-o-c-e-n-e.com and Putamen Capital and is circulated for informational and educational purposes only. This disclaimer informs readers that the views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual. You should not treat any opinion expressed in this article as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of an opinion.

“Analysis of complex systems almost always turns on finding recurring patterns in the system’s ever-changing configurations.” John Holland

Adapting to the Virus

The past two years saw both familiar and unfamiliar shocks. Diverse agents adapted differently to the virus. For example, the developed world adapted to the vaccine by being more innovative (innovating vaccines) than in the past; and developing countries learnt how to co-exist with the virus. Meanwhile, China decided to remain isolated as Beijing maintained zero-covid policy – a stance unexpected to reverse, likely because of the fear that its vaccines are less efficient and that an uncontrolled spread of the virus will overwhelm its healthcare system.

The economic shock was not as severe as the 2008 crisis because of the policymakers’ historical experiences. The action to the stimulus was timely and appropriate. It avoided the deflationary pressure, but it created new problems. The demand-supply imbalances created by overly generous easing efforts risk driving up asset bubbles and temporary shock in prices as goods demand outpaces supply capacity.

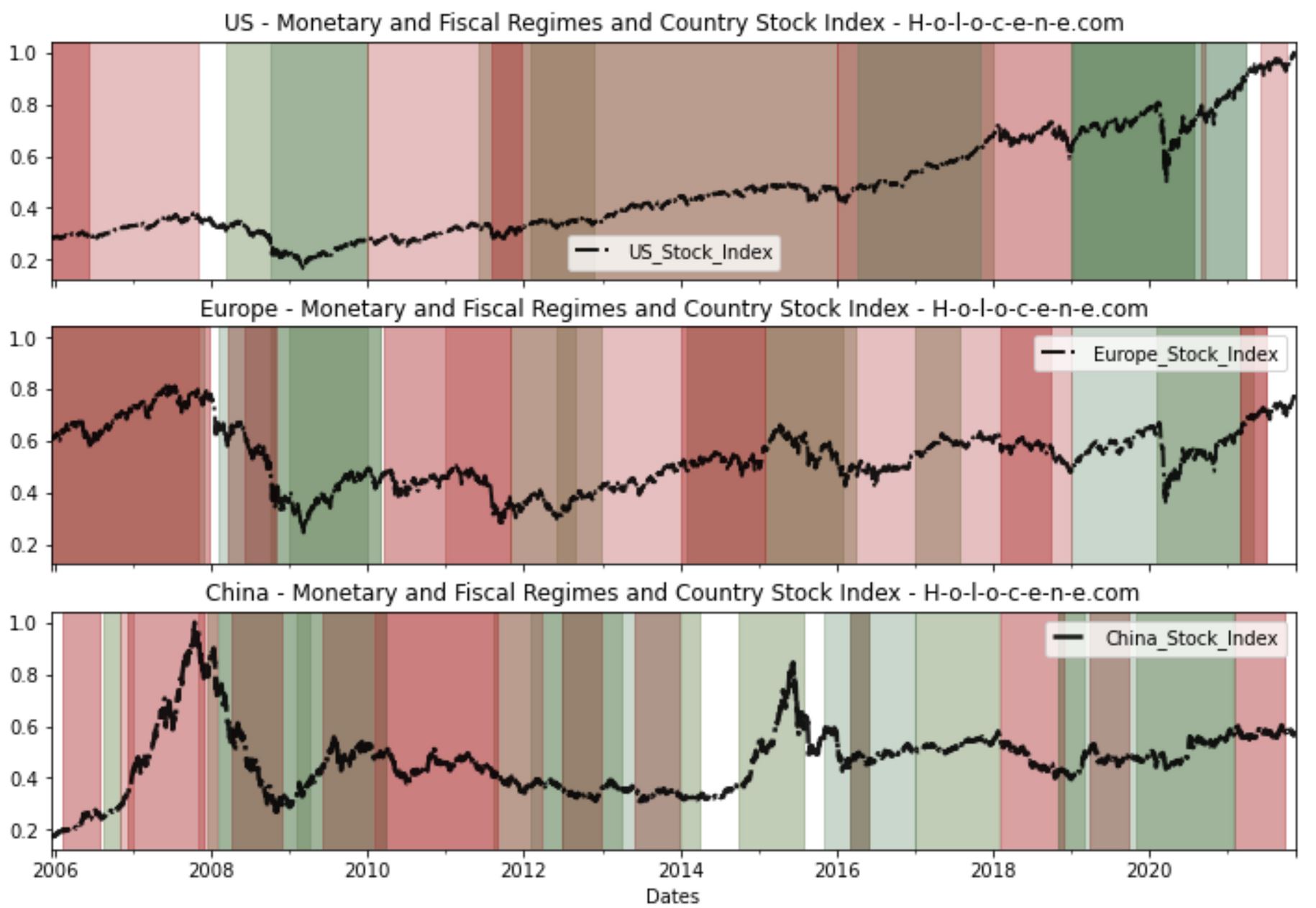

The Tri-polar Monetary and Fiscal System: US, Europe and China

* Red is tightening and green is easing. Mixture of both gives them different hues. Source: H-o-l-o-c-e-n-e.com

Japan, US, China and Europe’s Economic Statistics

Source: H-o-l-o-c-e-n-e.com and Bloomberg Intelligence

The market performance synchronized with supper easy monetary & fiscal policy in the developed world, market reforms in some emerging market countries (for example, India), policy tightening in China and the bouts of inflationary pressures.

Global Markets – Last Twelve Month Performance

Source: H-o-l-o-c-e-n-e.com and Yahoo Finance

“Whenever I see a stock market explode, six to 12 months later you are in a full blown recovery” (Stanley Druckenmiller) except in China. To a well-balanced investor, China’s FX, Equities and FIs are both a blessing and a curse. Blessing in-term of exceptional diversification feature and a curse in terms of unpredictability.

Growth Outlook of Two Giants

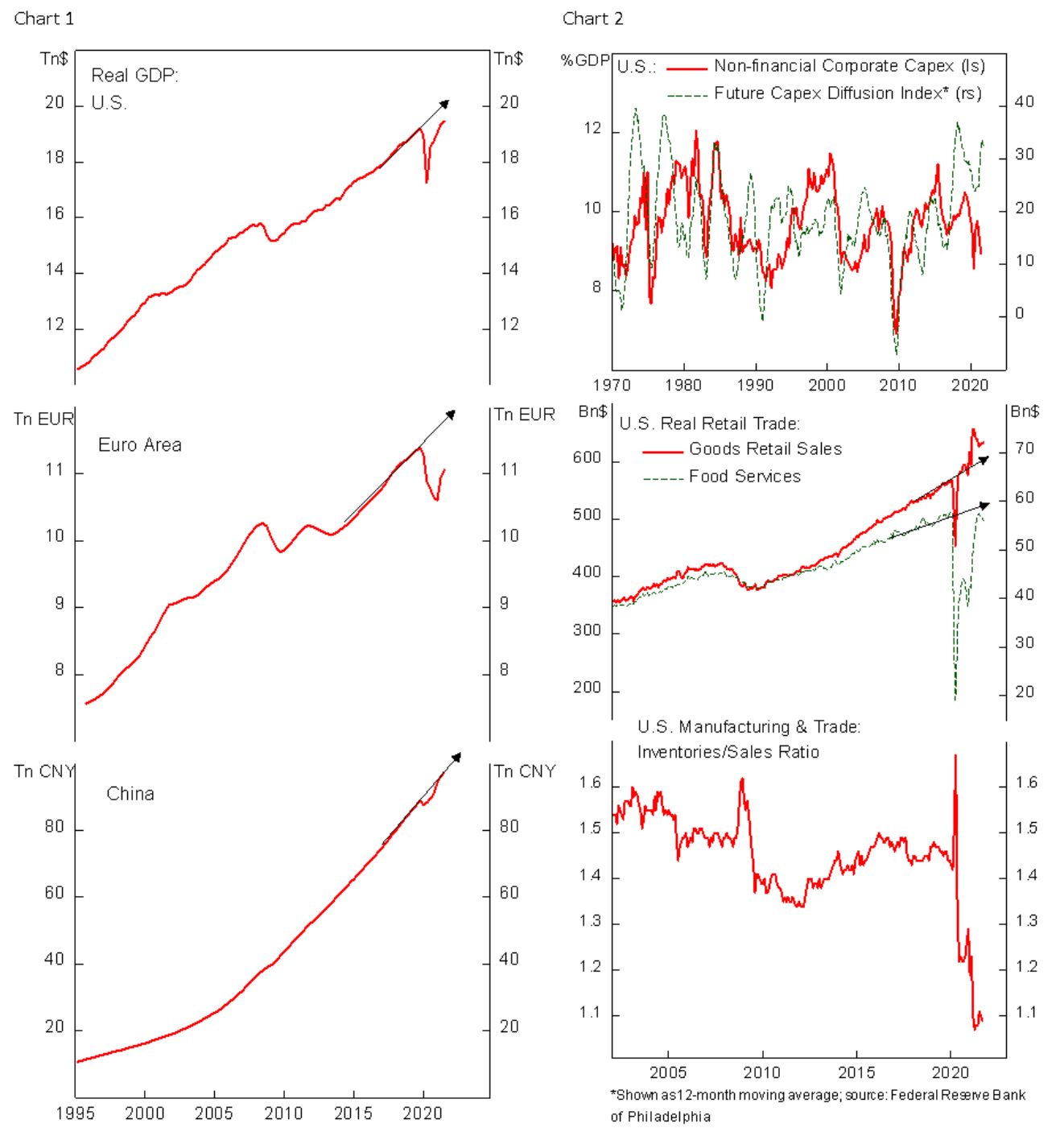

Despite the apparent boom in global economy, however, U.S. GDP today is still 3-5% lower relative to pre-pandemic trend, while Euro Area GDP has yet to recover to per-pandemic level and is probably still 8-10% lower compared to its trend growth (Chart 1). China is the only country that has already catch up to its pre-pandemic trend, although this has been driven by strong export demand rather than robust domestic demand. All these mean that although growth will continue to decelerate in the coming quarters, it will likely remain above trend in the U.S. and Europe. The bullish case for Chinese economy is uncertain due to the government active policy to reign its over-levered property sector and slowdown in its export demand due to normalization of the share of goods and service consumption. Look for the change in China’s policy makers sentiment.

Our bet is that new variants of the virus will become less lethal over time and hence allowing a faster catch up of the service economy. This means travel, hotel, and leisure – the largest casualty of the pandemic – could be the biggest winner next year, replacing demand for consumer goods and electronics, and potentially easing the disruption in global supply chain. Peak in goods demand, normalization of supply from manufacturing base in Asia, and a possible top in the oil market should all ease inflation in the U.S. and Europe. Those on the camp arguing that inflationary pressure is a permanent feature of post-pandemic world should look at inflation across Asia, which has a much better response against the pandemic and continue to record muted headline inflation numbers – despite also being impacted by higher global oil prices.

Our base case for U.S. economy for next year is as follows: Robust profit growth will translate to capex boom next year and drive productivity higher in the medium term (Chart 2). Home construction activity will remain strong amid low rates environment and low supply/inventory. Meanwhile, the consumer demand for goods should shift lower albeit still above trend, coinciding with pick up in services consumption. A tailwind to GDP growth will also come from the corporate sector replenishing its inventory, which has been depleted this year amid supply-chain issues. Taken together, U.S. growth should continue to be strong in the first half of 2022, which could close the output gap by summer and allows the Fed to hike rates in the second half of the year (discussed in the next section).

A rapid turnaround of the ongoing slowdown in China is less likely, as the government is keen on cleaning up excesses and focusing on “quality growth” – a hint that it will not indulge in another binge of infrastructure projects financed by the local government financing vehicle. The underlying growth trajectory of Chinese economy continue to downshift amid structural headwinds and the near-term risk remains to the downside, despite recent easing efforts. Beijing has maintained pressure on property developers to de-lever without causing systemic risk to the financial market and tighten regulation on its tech champion. Chinese tech stocks listed in the U.S. have continued to trade near its post-crackdown low and Chinese regulators have asked Didi, the ride-hailing firm, to delist from U.S. bourse. The government’s stance in these two sectors highlights the lack of urgency among policymakers to stimulate the economy

More importantly, Chinese policymakers have historically tended to be reactive rather than proactive in easing fiscal and monetary policy – creating large volatility in the market. This time seems to be no different. The divergence in growth outlook for the U.S. and China will also translate to an opposite policy response from both countries’ central bank, with profound impact for the dollar, commodities, and risk assets.

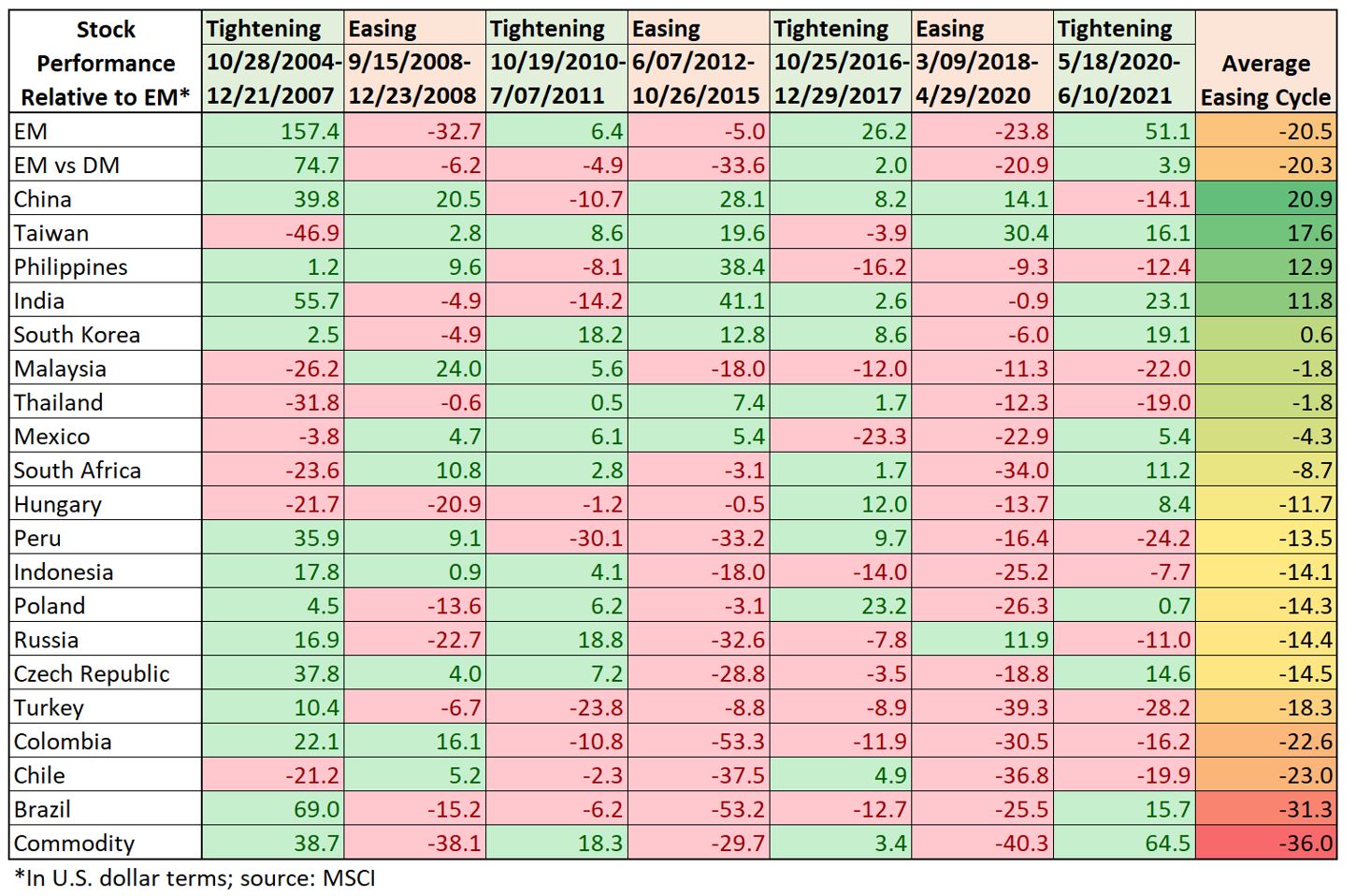

China Easing Periods – Rear-View Mirror

The Ghost of Global Imbalance Past

The unprecedented fiscal and monetary stimulus bolstered aggregate demand by households and prevented a liquidity crisis in the corporate sector, causing a boom in retail spending and the financial market that partially drove up inflationary pressure. A large portion of the stimulus ended up as household savings and are still sitting on bank deposits, one of the reasons for the jump in U.S. household wealth aside from the rising real estate and equity market.

The Moon and Sun of the Global Macro: (S – I) + (T – G) + (M – X) = 0.

In the context of savings and investment balance, we think the U.S. will continue to run into excess savings problem in the medium term. The IMF forecast that U.S. government cyclically adjusted primary balance will decline from 8.6% of GDP in 2020 to 6.9% in 2022. Meanwhile, households have saved up majority of the fiscal transfer and the corporate sector has continued to buyback shares – highlighting the lack of investment opportunity. This should drive an improvement in U.S. current account balance next year, potentially unleashing deflationary pressure to the rest of world.

The increase in public savings will have to be absorbed by private domestic investments or foreign public & private investments. But we are living in the world of Neanderthals who thinks mercantilism is the way to banana-land. So, when the US fiscal and the Fed are tightening policy, a lot of foreign policy-makers will be forced to tighten monetary and fiscal policy as well, depressing demand in their domestic economy.

Ok, Walter!

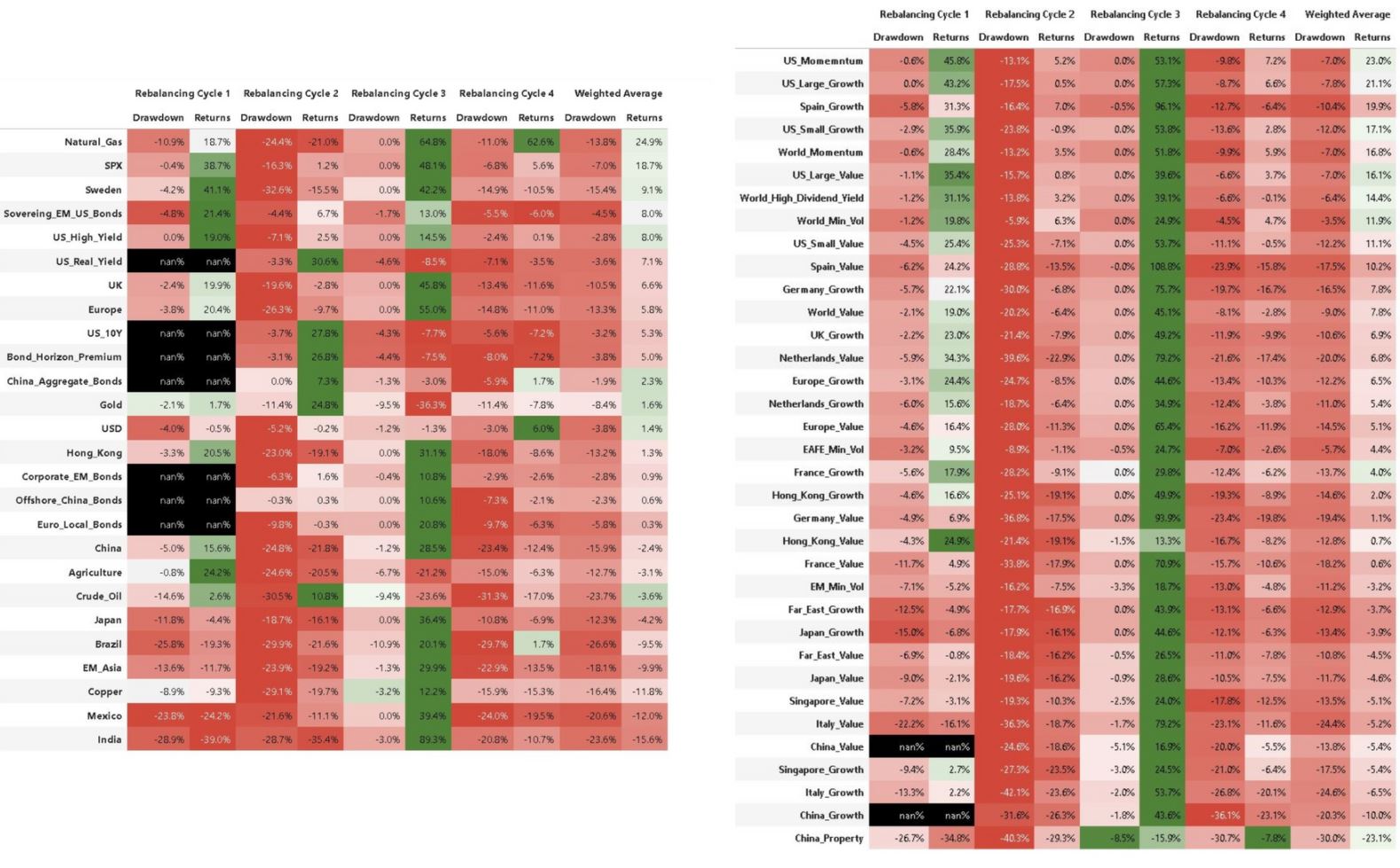

Previous Rebalancing Episodes

* Tequila crisis (not shown in the chart), Asian Currency Crisis (not shown in the chart), Russia’s default (not shown in the chart), Euro Crisis were all examples of the aftermath of rebalancing. * 2008 was because of the great imbalances. *H-o-l-o-c-e-n-e.com

Post-2008 – Rebalancing Episodes – Market Performance

Source: H-o-l-o-c-e-n-e.com and Yahoo Finance

There is a high chance of policy makers choking global growth and creating a classic rebalancing episode. Some assets and pairs are looking compelling. For example:

- Long Gold/Short Copper.

- Long UST Real Yield (Long UST/Short UST Inflation Linked Bonds),

- Long China/Short India

are all attractive positioning going into 2022.

Current Positioning vs Returns During Rebalancing Periods

Source: H-o-l-o-c-e-n-e.com and Yahoo Finance

The call to long Chinese equity could go wrong if China’s policymakers are late in stimulating the economy when global rebalancing takes place. However, investors could reduce the market beta by shorting Indian equity from valuation perspective, Chinese stocks are currently trading at depressed multiples, while Indian stocks’ multiples are near record high amid the impressive rally this year. A mean reversal is likely. We will talk about a potential easing in China in the coming section.

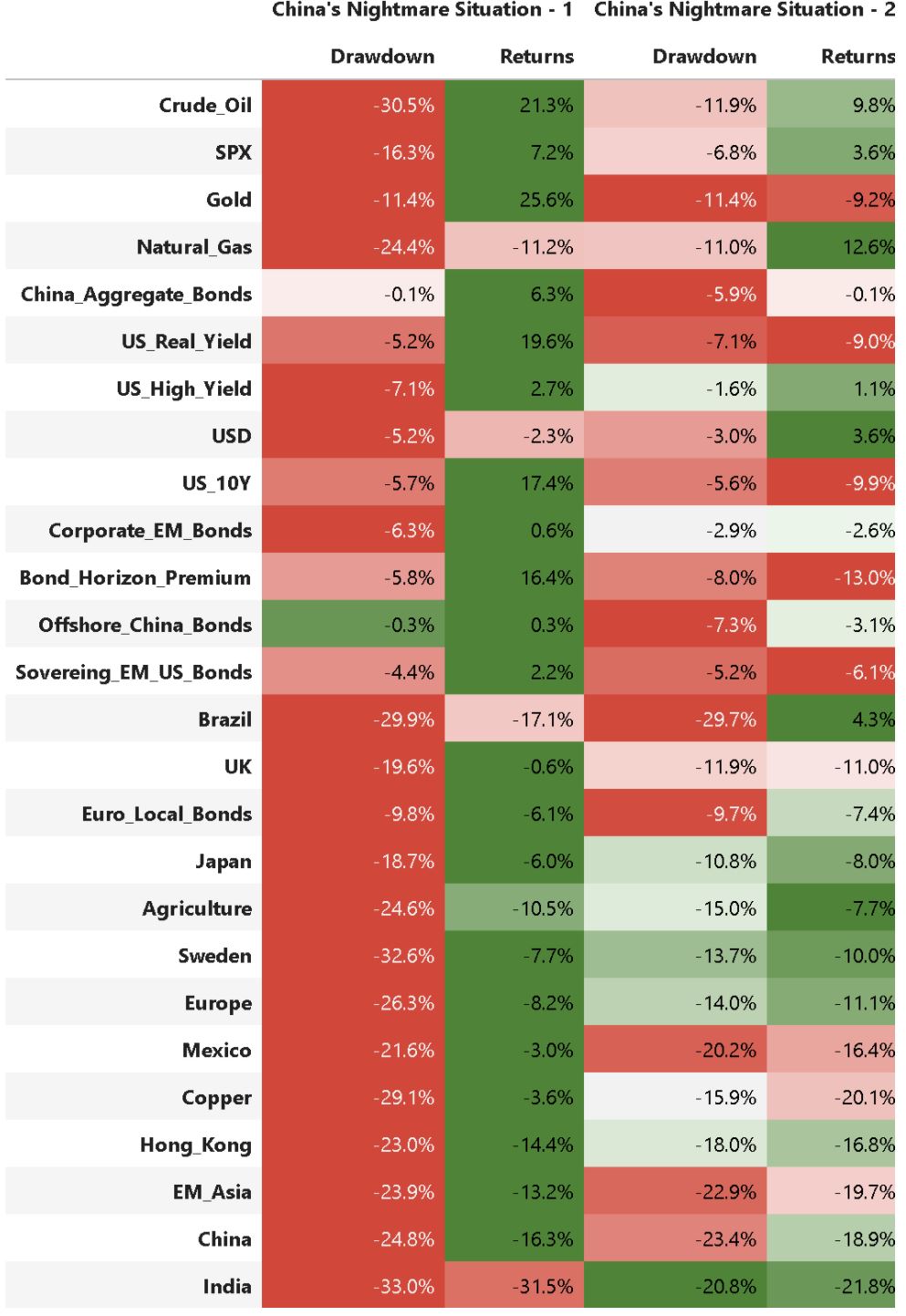

China’s Tightening + Global Re-balancing – China’s Nightmare Situation

Source: H-o-l-o-c-e-n-e.com and Yahoo Finance

Fed vs PBoC: The Dollar, Yields, and Commodities

Our base case of a strong U.S. growth and weak China and the rest of the world is a tailwind for the dollar and U.S. equity, a strategy that has worked well in the past 6 months and should continue to do so if the Fed maintains its relative hawkishness versus other central banks. As in previous tightening cycles, stronger U.S. growth next year should allow the Fed to be the first central bank to hike rates among major central banks – PboC, BoJ, and ECB – and see the dollar firming (Chart 3). So far this year the Fed has been much more dovish than the market’s rate expectation, which causes downside surprises in the dollar and Treasury yield following FOMC meetings. The Fed said that its target of 2% average inflation has been met, but employments have some more room to catch up. A catch-up by the Fed to market expectation will likely rattle the market, which could be the case if employment figures grow above an average of 500k per month until the middle of next year. In addition, a tight labor market and wage increases going into the second quarter of 2022 will force the Fed hand to increase the rate. Good news for the economy will become bad news for the market surrounding the liftoff date.

A stronger dollar, however, also signals tighter liquidity next year at a time when money supply growth will decelerate rapidly. This will increasingly become a headwind for risk assets. We bet that the hawkish Fed will flatten the yield curve further and eventually choke growth, exacerbating the sell-off in both stocks and commodities. Chart 4 shows that in 2018, when the Fed was tightening but PBoC was easing, stronger dollar coincided with correction in both copper and gold. A repeat of a similar episode next year is possible, in our view.

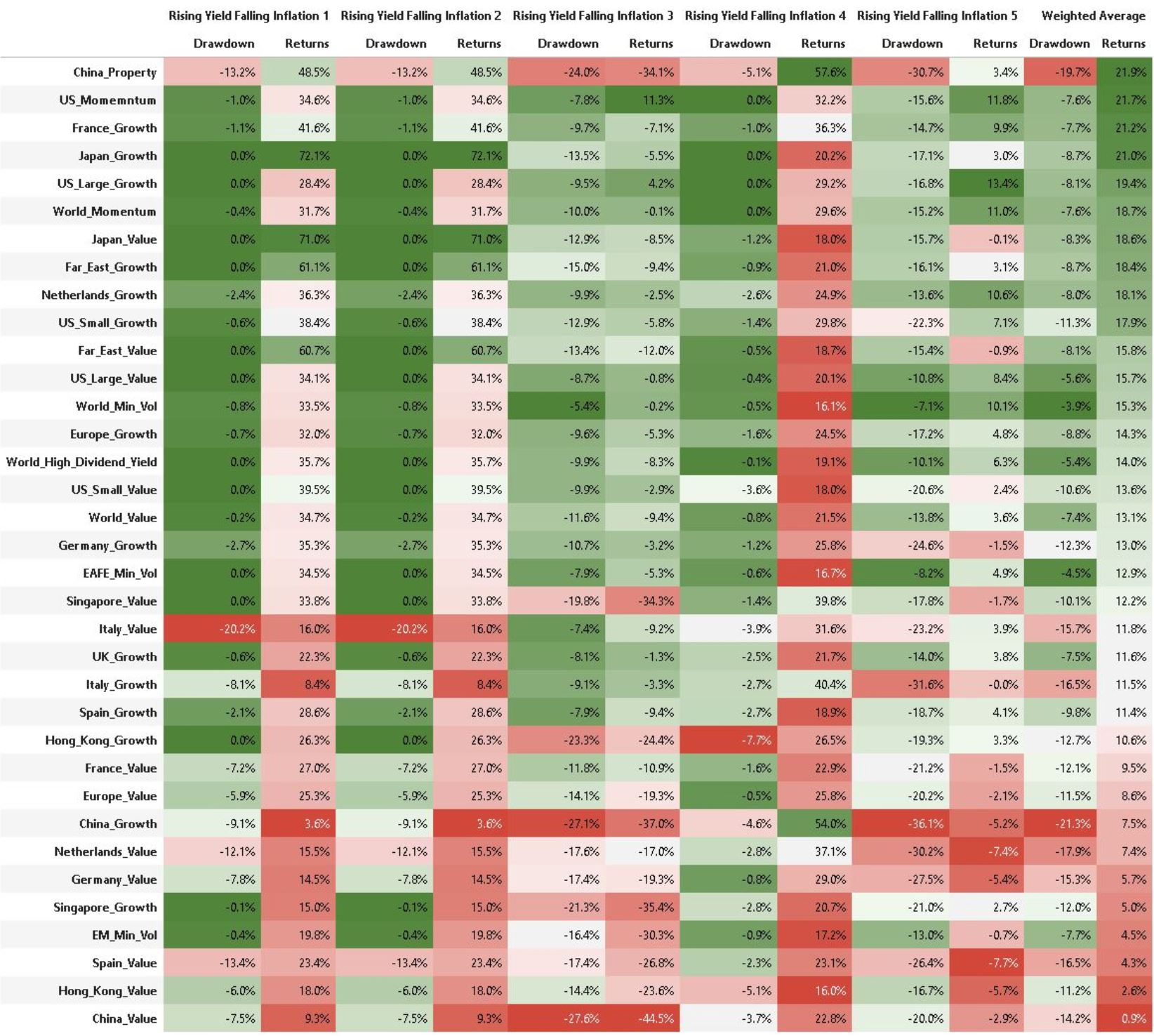

Tightening Cycles & Rising Real Yield-Falling Inflation Period Analysis

Source: H-o-l-o-c-e-n-e.com and Yahoo Finance

More importantly, the business cycle is peaking out already and will mean-revert to the downside in the coming year.

Investors should go defensive and short copper/gold ratio and long U.S. Treasury bonds, while reducing equity exposure. At the margin, slower global growth and easing supply disruption bode poorly for goods and commodity prices. The bearish case for copper is also supported by the normalization of supply from Chile and Peru, and lower demand from slowing Chinese real estate and infrastructure activity into the next year as developers voluntarily de-lever and undertake fewer projects (Chart 6). The country accounts for 50%, 47%, 60%, and 50% of global copper, aluminum, iron ore, and steel demand respectively.

What About Oil?

Oil supply/demand will continue to be tight in the coming months, but the room for prices to go higher is limited. In fact, chances of prices dropping 12 months out from current level have increased amid downside risk from China and the OPEC+ gradually increasing its supply. Moreover, backwardation in the oil curve has reached an extreme, which historically was followed by a drop in prices (Chart 7). Our hunch us that oil price will stabilize around $60-70/barrel, which allow lowest-cost producers to maintain healthy margin and satisfy both the government in Russia and Saudi Arabia. Despite the appearance of strict discipline among OPEC+ members, apparently the Saudis have not been happy about losing its market share to Russian producers (Chart 8). Any demand for further production cut, whether due to slowing global growth or temporary setback from new covid variant, is likely to trigger a strong pushback from both sides – leaving price to adjust lower.

To conclude, look for sectors and factors that do well when the Real yield rises and breakeven inflation falls. China’s property sector and offshore stocks are going through idiosyncratic shock but keep monitoring the new developments in the policy-making space. Long USD/Short CNY looks solid in a policy divergence situation. The global rebalancing + global policy tightening is as bad for India as-is for China. Thus long China/short India pair is looking very attractive. Whether we see a classic rebalancing cycle or CAPEX boom, commodities are unattractive in the short-term, short copper/long gold is a viable trade opportunities, in our opinion. Oil should continue to trade in the range of $60-70/barrel.