Download PDF:

Copper/gold ratio has increased to prior peak in the business cycle, although yield curve is only halfway through. This could be explained by the dovish stance held by Federal Reserve to stay accommodative until maximum employment is achieved and inflation average at 2%, meaning that unlike in previous cycles, pre-emptive tightening is not likely to happen, and monetary policy will stay dovish than what previous cycle suggests. This should translate to inflationary pressure continuing to rise gradually, while a hike in policy rate expectation being shifted to the long end of the curve, potentially delaying the timing of the first hike in policy rate but increasing the pace of the hike once it begins.

After being strongly bullish on copper since last year, we now see the attractiveness of copper and gold as balanced, with gold potentially outperforming if the upturn of the cycle is botched by an overkill in “policy normalization” from China or abrupt tightening in fiscal and monetary stimulus globally. Global equity should continue to do well, but a sustained double-digit return is unlikely for developed market stocks. We see more attractive opportunities for value stocks in the EM space.

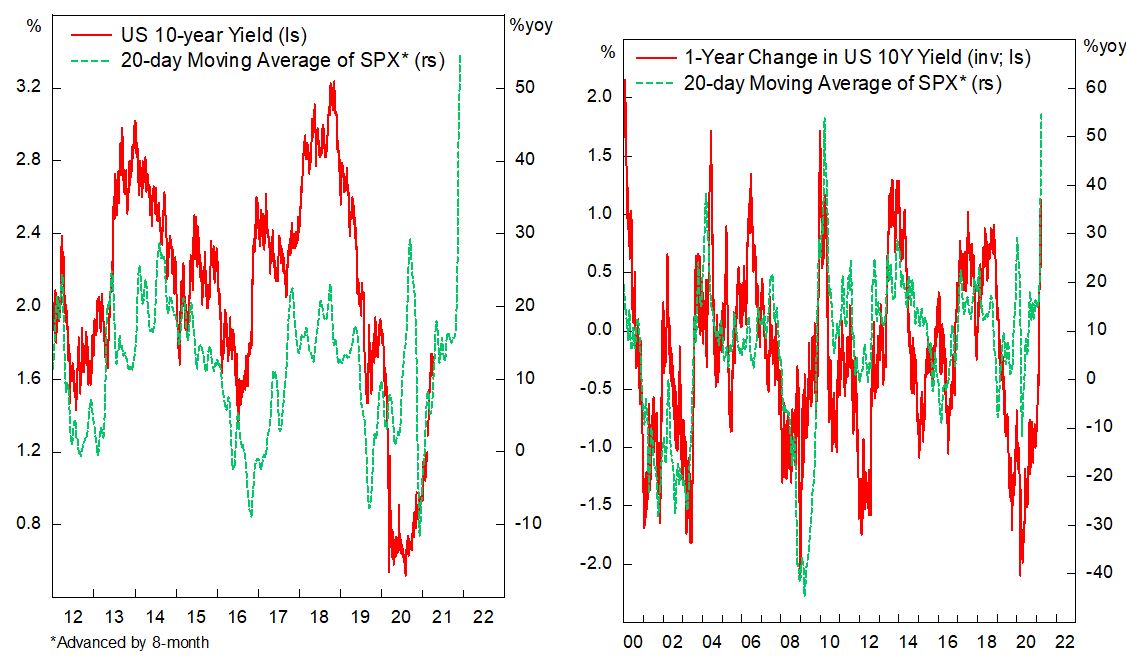

In the short-term, we are expecting a pullback in 10-Year Treasury yield to below 1.5% range based on two reasons: market converging to dovish Fed policy and correction from an oversold condition. Treasury yield is reaching an inflection point on a rate-of-change basis, which historically coincided with the reversal in yield direction. A pullback in yield, if not coinciding with decline in inflation breakeven, should put the shine back for precious metals, which have corrected heavily of late.

The bottom line is that we are passed the maximum acceleration point in the upturn of the cycle, with asset market potentially becoming more volatile and entering consolidation phase.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.