Download PDF:

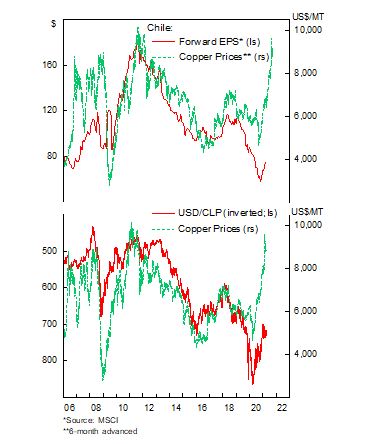

Chile

The cyclical bullish case for Chilean stocks is straightforward. Chilean earnings are set to improve dramatically from the higher copper prices, which will continue to enjoy structural boost from electrification of vehicle and green energy infrastructure demand, as discussed in a previous report. Chinese imports continue to pose strong number in recent months despite the fear of policy normalization, and President Biden’s $2 Tn infrastructure plan further bolster demand for the metal in the coming years. In addition, copper accounts for over half of Chilean goods exports and hence higher prices provide direct tailwind to the country’s trade balance and is a boon for the CLP.

Despite the strong tailwind Chilean stocks are still trading at a reasonably cheap valuation, with cyclically-adjusted P/E at 14 times – far below its historical average – and the market has been excessively bearish on the country’s earnings expectation, which may be explained by the country’s poor health situation and political uncertainty. Although Covid-19 new confirmed cases and deaths are still rising as of this week, with over half of the country’s population now vaccinated, we expect the health condition to improve in the coming weeks, which should allow economic activity to rebound more rapidly.

Lastly, the prospect of a left shift in Chile’s policies after the constitutional referendum this year looks unlikely. The centre-right is united and set to take over a third of the seats of the constitutional assembly, hence the ability to block major reforms. With the left coalition acting as a marginal member of the body, the resulting charter will likely be a consensus between centre-right and centre-left members, reducing the likelihood of withdrawal of current market friendly policies.

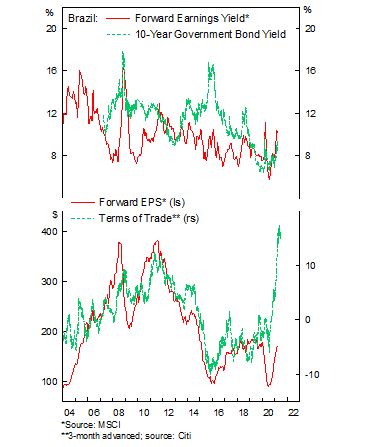

Brazil

Remain slight overweight Brazilian equities. Our expectation of higher earnings for Brazilian stocks have slowly materialized in recent quarters with earnings back to pre-pandemic level, and we are still expecting further gain in earnings in the coming months, driven by the rising soybean and iron ore prices that translate to a massive improvement in the country’s terms of trade.

Meanwhile, the improvement in earnings has not coincided with a rise in the asset market, – stock price in local-currency terms has been flat last quarter – pushing down the country’s forward earnings multiple from 13 times in December last year to 9.8 times. As a result, Brazil currently provides an attractive 10% forward earnings yield, near the historical high level in the past decade and normally marks the bottom in Brazilian stocks.

More importantly, the Real is massively undervalued, according to our fair value estimate, and recent policy rate hike should bolster the attractiveness of the BRL. We think previous headwinds for the BRL – such as the poor fiscal situation and ultra-low real yields – are starting to and the Real should be among the biggest winner once the dollar resume its decline.

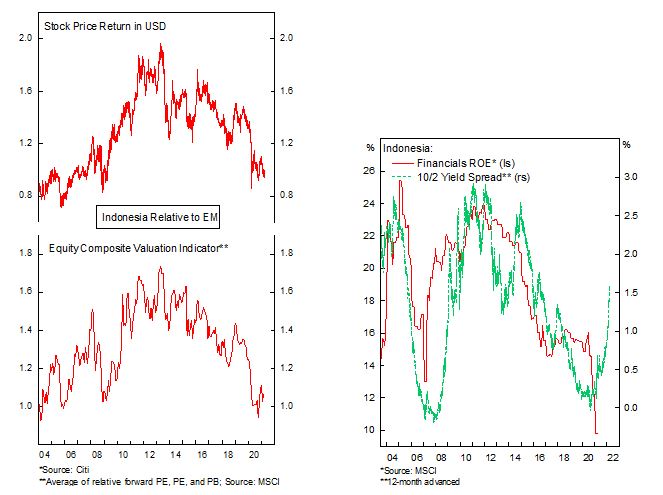

Indonesia

Indonesian stocks have so far lagged the recovery in asset prices and the country’s valuation is now comparable to the EM benchmark, near the low end of its two-decades trading range. First, unlike energy or material firms, which directly benefit from rising commodity prices, banks – which accounts for half of Indonesian stock index – tend to lag the recovery but should catch up in the coming months.

Second, Indonesia’s monetary policy will remain accommodative amid negligible inflationary pressure, which should allow the economy to rebound faster and lead to further steepening of the yield curve. Financials, which account for half of Indonesian equity index, should do well in this environment, with net interest margin set to rise in the coming year and non-performing loans ratio to moderate going forward.

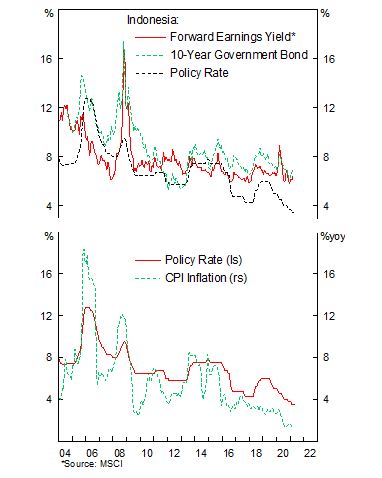

Finally, we are betting that Indonesian local-currency bond yields to fall, which should also push equity multiple higher (or forward earnings yield lower). At 5.5%, the real 10-year sovereign yield of Indonesian bond is very rich, even if investors want to hedge the currency exposure.

Mexico – Slight Overweight/Neutral

Mexican equity has fared well relative to other Latam bourse since the bottom of last March and should continue to outperform the benchmark, despite real economic activity lagging other EM country, mostly due to the tepid fiscal and monetary support provided by the government. In fact, Mexico is among the few major EM countries where manufacturing PMI is still contracting and retail trade below pre-pandemic level. Going forward, however, the declining trend in new Covid-19 cases should allow restrictions to be eased further as inoculation campaign progresses, albeit at a much slower pace compared to Chile.

The fiscal and monetary conservativeness shown by Mexican government during the pandemic also means that the country will face much less fiscal drag and increase in policy rate this year, supporting the “natural” recovery of the economy. In addition, the rapid recovery in its Northern border should bode well for Mexican exports – mainly automotive – and boost its trade balance and equity earnings.

On the asset market side, Mexican stocks are still cheap, trading at 14.6 times forward earnings and the currency is 15% undervalued, according to our fair value estimate. Taken together, the improvement in earnings, reasonable multiples and cheap currency should translate to the outperformance of Mexican stocks going forward.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.