Download PDF: LATAM Countries Revisited PC

Argentina

The Fernandez government is taking a hard stance on the debt renegotiation, postponing interest payment until 2023 and forcing a 5-12% haircut on the bond principal value. The “Globales” bond’s principal under restructuring amounts to 6.7% GDP and its annual interest expense close to 0.4% GDP. The key point in the current negotiation is to drastically reduce and defer the interest payment of its dollar bonds, as outlined in the Table 1 below. Current bondholders have the choice of accepting the offer or going on a lawsuit demanding a full payment against Argentina’s government in the international court. Should they accept the “exchange” term of the new bond proposed currently, this translates to a recovery rate ranging from 30 cents/$ for the infamous “100-year bond” to around 35 cents/$ for the bonds maturing in the medium-term (Table 2).

Argentine domestic economy is still very weak and the current crisis risks putting the already timid recovery in jeopardy. Although exports have been boosted by the much cheaper currency and the trade balance has turned into surplus, its manufacturing sector capacity utilization remained low and will likely suffer further from reduced global demand due to COVID-19 (Chart 1). Money supply growth has been accelerating and inflation will remain high as the ARS has yet to find a bottom (Chart 2).

The longer-term prospect also remains bleak. Risk premium on Argentina’s sovereign debt will remain high for the foreseeable future, which will strain the government ability to stimulate its economy. Social security benefit accounts for over a third of government revenue and interest payment took over 3% of GDP, even after current restructuring (Chart 3). The stock market is more interesting, trading at 5x trailing earnings and below book value (Chart 4). However, as the impact of economic shutdown is yet to be quantified, the key is to monitor development in the corporate sector leverage, foreign-currency exposure and the banking system ability to handle rising NPL and maintain adequate capital ratio.

Mexico

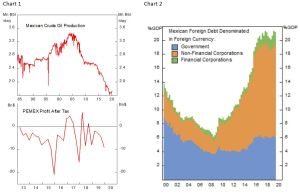

Last month’s (April) PEMEX credit rating downgrade into junk and Mexican sovereign by one notch to Baa1 has further increase the macro risk of Mexican assets. However, this should not come as a surprise as PEMEX balance sheet has deteriorated for years and oil production has slumped amid low investment and unfavorable policies toward foreign investment (Chart 1). In the short-term, fixed-income managers and ETF will be forced to sell their PEMEX bond holdings, the largest fallen angel this year with $133 billion (11% GDP) outstanding, which may put a short-term cap on the Peso. Longer-term, this will dramatically increase the interest cost burden further, which will deteriorate both profitability and leverage position of the state-owned oil firm, which may require further capital injection from the Mexican government and drag down its fiscal rating.

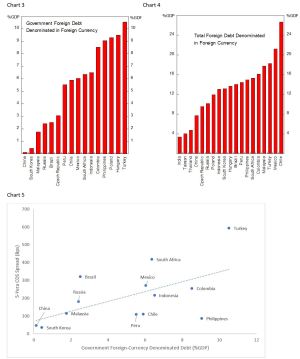

The cost of insuring against default of Mexican government hard-currency debt has widened to 270bps from 78 bps early this year. Comparing to other EM countries government debt level relative to its economy, however, the increase is proportional to the risk (Chart 3-5). More worrying is the foreign-currency exposure among corporates, which has increased from 2% GDP in 2008 to 13% GDP currently (Chart 2). It remains to be seen whether Mexican businesses are able to service their hard-currency debt obligation with a much weaker revenue and currency.

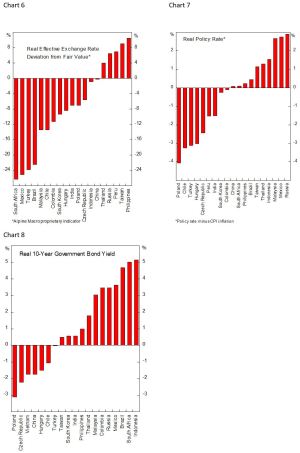

The current rout in EM currencies have pushed the MXN, already cheap before the crisis, deeper into undervalued territory (Chart 6). We maintain our positive stance on this currency. Despite the massive monetary easing across EM, Mexican monetary policy is still among the tighter one, with real policy rate at 2.8% (Chart 7). Moreover, Mexican current account has turned into surplus last year due to the slump in the domestic economy. On the fiscal side, the government willingness to do big fiscal stimulus is low, with COVID-related stimulus amount to only 1% of GDP, as the president is stubborn on maintaining healthy fiscal balance and reigning debt amid the crisis. This should be positive for the country’s local-currency sovereign bond, whose real yield is currently among the highest in EM, trailing only Indonesia, South Africa and Brazil (Chart 8-9). Long Mexican local-currency government bond, currency unhedged.

Brazil

Bolsonaro is losing several key people in his administration, some of which play an important role for the structural reform. The former justice minister, Sergio Moro, is accusing the president of obstruction of justice regarding his intervention is his family’s police investigation. Mr. Moro was one of the key figures that helped Bolsonaro became a president after putting in jail Lula da Silva, the leading candidate in 2018 election on corruption charges, which was unwound afterwards. There is a non-trivial possibility that the president will be impeached. Rodrigo Maia, the lower house speaker, who currently have feud with the Bolsonaro family will hold the key to whether to proceed on the impeachment process.

With COVID-19 forcing policies to support the economy and rising political risk, reform agenda will likely be put on the backburner. So far, the government has announced 6.5% of GDP fiscal stimulus to support businesses and employees. The president’s reluctance to put the economy in a “lockdown” and feud over the quarantine policies have resulted in the resignation of the health minister and risk prolonging the time for eventual recovery.

From a macro perspective, Brazil’s monetary policy has been very loose, with real policy rate close to zero (Chart 1). This has caused the BRL to plunge and put additional pressure on the corporate sector to service their hard-currency debt. The good news is that Brazilian foreign-currency denominated debt level, relative to its economy, is much lower compared to Mexico and the banking sector for both countries are well capitalized in facing the increase of NPL.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.