In the past few weeks, Russians have been venting their rage in both the street and online due to the increasing hardship resulting from various lockdown measures. But even before the virus struck, many have been protesting against the government, including against the planned constitutional reform that would extend President Putin term limit until 2036. Although the proposal was hurriedly passed by both houses of parliament for a scheduled vote on April 22, the president eventually postponed the nationwide vote due to fear of backlash from a further outbreak of COVID-19. In the first few months of COVID-19 spread Russia seems to be managing the outbreak very well, by launching a large-scale testing among its population. However, as outbreaks of virus clusters surfaced across the country, it became increasingly clear that the country has to implement a stricter lockdown measure to curb the spread. At the end of April, President Putin reverse its rhetoric and acknowledged that “a hard and difficult path lies ahead”. Currently, Russia rank 3rd in terms of number of people infected but managed to keep mortality rate low, at only 0.9%.

It remained to be seen whether the current crisis and round of protest will trigger a larger social upheaval, especially in Moscow, or just another round of protest that eventually be crushed by the government security force, as has been normally the case. On the economic front, there are several development worth noting:

- Growing dissatisfaction among Russians. After having doubled in the first decade of the millennium, the level of real wage has stagnated in the past 8 years (Chart 1). Investment has slowed on the back of lower oil prices and the country’s dependency on oil has left other sector neglected, unable to provide a buffer during period of low commodity prices. The lockdown measures, which have resulted in drop in income and rise in unemployment among majority of the population, have only add further pressure on household and many are asking the government for a subsidy or to provide employment.

After the protest in Vladikavkaz, where many were breaking the self-isolation rule, Russians are shifting the protest to online platform such as Yandex, the country’s equivalent of Google Maps, by marking their position in front of government buildings and leaving anti-government comments. Many demand that the lockdown, which has hurt employment and small businesses, to be lifted. It is likely due to this pressure that even as the COVID-19 new daily infection cases are still high, the national lockdown restriction is lifted on May 11. However, many of the local governments are still implementing city-wide lockdown and bans large public events. It is likely a strategy by President Putin to shift the blame and responsibility to the prime minister and local government, to do the heavy weight of lifting the economy and battling the disease, as his popularity declined.

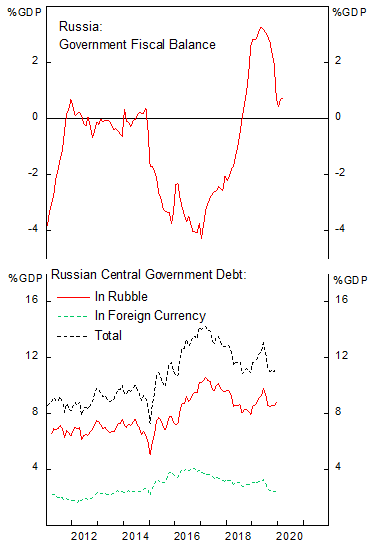

- With low ability to significantly boost social spending significantly, Russian government is perceived as doing too little and abandoning the people to fight for themselves. So far, the government has announced a fiscal package worth 2.1% of GDP related to the COVID-19 response. The combination of collapsing oil revenue and higher expenditure is projected to push government fiscal balance to a deficit of 4.5% of GDP (Chart 2). However, we think the government balance and debt level is not a cause of concern for sovereign default, as central government debt amounts to only 11% GDP in total, with a fifth denominated in foreign currency.

The weak growth condition will put further pressure for the government to utilize its National Wealth Fund (Chart 3) to support the domestic economy, as we argued on a previous report (Russia Footer). President Putin has been the champion for 2018-2024 National Projects, worth some $391 billion, or equivalent to 25% of GDP. Prior to the crisis, the implementation of the projects has been slow and now there are increasing doubts that the project will fall apart, similar to the 2007 national projects prior to the Global Financial Crisis. However, we think that the renewed pressure on President Putin popularity will force him to refocus on managing the domestic economy after years of foreign adventure in the Middle East.

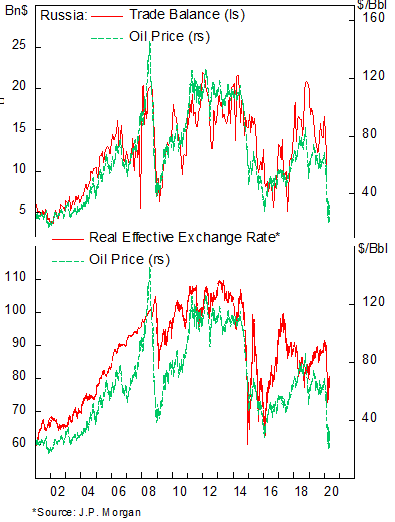

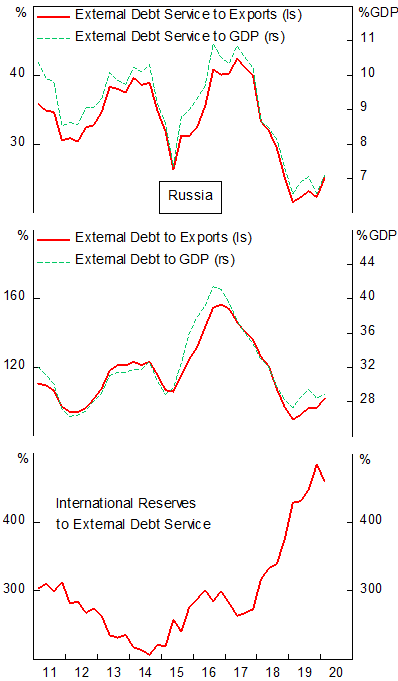

- With current account surplus, ample reserves and manageable external debt level, the risk of Balance of Payment crisis or default is very low. First, Russian trade balance will likely remain on surplus despite current oil price collapse, as the cheapened Rubble depressed imports further (Chart 4). Going forward, the trajectory of global recovery will highly determine the path for oil price and Rubble’s likely appreciation from current level. Second, after the 2015 sanctions by the U.S., Russia has been building a war chest and preparing for a severe shock as happened currently. Russian foreign reserves to external debt coverage is more than adequate and is among the highest in EM universe (Chart 5).

- Monetary policy will likely be loosened further to support businesses and the banking sector. The current policy real rate at 2.5% is still among the highest in EM space and the Ruble has been showing strength of late, which should reduce the worry of the Central Bank to cut its policy rate further. Although banks non-performing loans (NPL) will inevitably increase, currently, 80% of Russian bank loans are denominated in local currency (Chart 6), which should translate to a still manageable debt servicing cost for companies. However, we acknowledge the growing risk in Russian banking sector, which was still dealing with NPL legacy from 2015 oil price crash, before the virus struck.

As EM currency depreciated significantly in the current rout, we notice that EM countries have a diverging inflation trend. Mexico, Brazil, South Africa and Indonesia have seen CPI inflation decelerating even as their currency fall, while Russia has seen an uptick in its inflation due to higher food prices (Chart 7). This is a risk to monitor, as higher inflation will put the Central Bank on a more hawkish stance and might lead to renewed weakness in government bond and the Rubble.

Who Blinked First?

The rout in oil market last month has led to OPEC and Russia agreement on supply cut, which has stabilized price somewhat despite demand destruction exceeding the agreed cut and massive contango on oil futures. We have taken a positive view on oil and oil stocks in the next 12 months, as we think more positive surprises will likely occur. The first surprise is that in the second week of April, Saudi Arabia curb production more than it agreed to, highlighting its weaker bargaining power against other oil majors. This confirms our thesis that Russia is much more prepared to survive an oil price war than the Saudi, for the following reasons:

- Russia has a much lower fiscal-breakeven oil assumption vs Saudi Arabia. Although the Saudi’s marginal cost of production is much lower than Russia’s, its government fiscal is much more dependent on high oil price. The breakeven oil assumption for Russia is around $40/barrel whereas Saudi requires $80/barrel to maintain balance budget (Chart 8).

- The social construct between the two countries is on an opposite polar. Whereas Russians are adapted to living in a hardship and has unemployment rate of 4.6% prior to the crisis, Saudis benefit from the generous government support and around 30% of its young people aged 15-24 is unemployed, with total unemployment rate at 6%. This results in higher social pressure for the Saudi government to maintain its welfare program and the incentivize the government, whose majority of revenue comes from the sales of oil, to maintain higher oil price. All these will result in Saudi Arabia’s government running a huge fiscal deficit this year, financed by debt (Chart 9).

- The slump in oil price will likely turn Saudi’s trade balance into deficit, which put pressure on the currency peg to devalue (Chart 10). With the dollar being very strong, the SAR has become very expensive, putting much pressure for the Saudi to utilize its large international reserves to defend the currency peg (Chart 11).

Copyright © 2020 Putamen Capital All rights reserved

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization Putamen Capital relies on a variety of data providers for economic and financial market information The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible

for the accuracy of data used herein