Download PDF: Monthly_201911

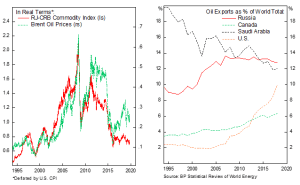

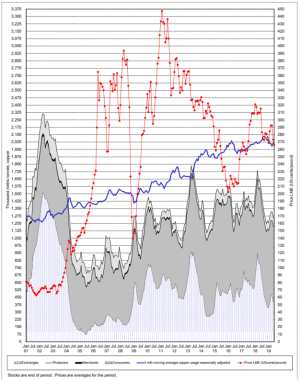

The structural backdrop of excess global savings, lackluster global consumption and investment demand and deleveraging cycle have all push bond yields lower. Meanwhile, the slack in manufacturing activity since 2014, magnified by the trade war, has push commodity prices in real terms to a level equal to those in 2001. Subjectively, it is unthinkable that commodity prices, especially metals, barely budged after two decades of massive infrastructure spending in China and emerging markets. Arguably, supply does expand when price rises, and technological advancement have made it cheaper to extract minerals from the ground. However, the reduction in number of reserves and increasing demand from electronic goods consumption are likely to far offset the increase in supply. For example, International Copper Study Group (ICST) estimated that demand for copper has increased by 60% since 2001, from 1.275 million MT to 2.025 million MT. More on the hard data below.

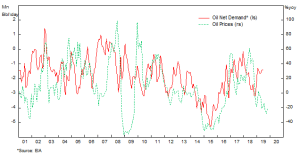

From a contrarian point of view, it is easy to make the call that in the next decade commodity prices are more likely to go up rather than go down. Large price correction in 2014 must have caused bankruptcy on companies with higher cost, leaving only those profitable enough to make a margin on depressed prices. And as usually is the case for commodity, depressed prices will initially force companies to produce higher amount of volume to offset the decline in prices, exacerbating the price decline. From the chart, we could see that this is the case for oil prices in 2014, until OPEC and Russia decided to cut production and essentially collude to maintain high prices. That decision results in the U.S. shale oil producer, with lower breakeven cost, benefitting from both higher prices and higher market share.

The case is a little bit different for commodities other than oil, as they do not necessarily have a well-established mechanism to adjust their production volume similar to OPEC. For example, Codelco production target, a Chilean SOE copper producer, may not be influenced by production target of Freeport-McMoRan or BHP Billiton. In short, higher competition (or lower collusion) forces each producer to maximize their own production function based on current market prices, rather than trying to bring higher prices together as an industry. That explains why oil price has historically been at a higher level after a slump compared to broader commodity index.

There are few logical implications going forward. First, the excess/shortage in commodity ex-oil is likely to be corrected by natural market forces, with higher proportion of firms going bust during price downturn and higher margin of surviving firms during price upturn (since it takes more time to establish new firm when price is increasing). Second, as a result of the natural cleansing process, current price better reflects the underlying supply-demand picture, with each firm optimizing their capacity utilization. This is contrary to the oil market where firms may underproduce in order to maintain price stability and allow healthy margin for the overall sector. Third, as a result of (1) and (2), a structural pent-up demand for commodity overall is going to affect commodity ex-oil price more than oil prices itself in the medium term, although oil does have a higher beta to global growth.

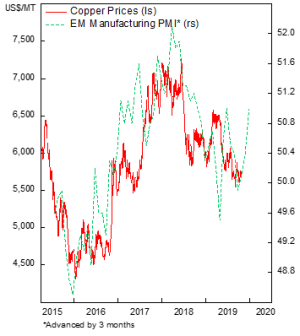

In this article, we are arguing that the recent slump in copper prices have eliminated marginal producer. From cyclical point, an improving growth in Emerging Markets, where massive structural investments are still needed, is pointing to a higher copper price. Moreover, since 2015, copper demand has been outstripping supply, causing inventory to decline from 1.55 million MT in early 2015 to 1.2 million MT early this year. Higher demand and the need to replenish inventory are likely to drive copper price higher in the next 3-12 months.

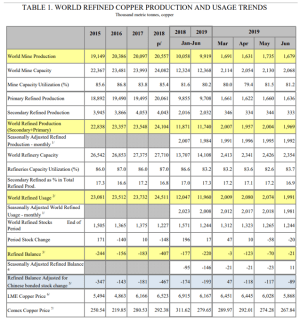

Source: International Copper Study Group

Source: International Copper Study Group

A Note on Oil

We also maintain a bullish stance on oil prices due to the improving cyclical backdrop. Moreover, declining growth on U.S. shale oil production and Saudi Arabia need for higher oil price to balance their budget is likely to encourage them to push harder cooperation with Russia. Recent estimate of oil supply/demand is pointing to shrinking imbalances, which should push oil prices higher.

Inflation Will Follow

A reversal of low inflation world would occur once global demand picks up and demand for commodity strengthen. Higher oil price, copper prices and other raw material will eventually translate to higher purchasing cost for many manufacturing firms such as automobiles. This will push consumer prices for durable goods higher. The problem is that now we are in a slow phase of inventory drain cycle. The turning point would be when supply of commodity products fall below demand, a condition we forecast to be coming in the next one to two years.

The long-term structural force that is likely to drive commodity prices higher is infrastructure construction in emerging and frontier markets, especially on the demand for base metal. Current cheaper prices will increase the viability of projects and hence driving the increase in prices when the momentum builds up. The decline in food prices, however, are likely to be a structural headwind for food inflation to go up, mostly attributed to invention in better and more efficient farming practice, not to mention genetically engineered plants that are more resistant to changes in weather condition and bugs. All these factors drive agricultural output prices down and is benefitting especially the poor countries, where hunger and poverty are still widespread.

There are reasons to believe that current decade’s low inflation is a one-off shock from technological advancement. Consumers have been benefitting from technological innovation to save cost like never happened before. Whereas in the past, consumers need to buy TV, sound system, furniture to hold it, nowadays younger consumers can live with their laptops to watch movies. And the need for camera, speaker, radio and phone have been replaced by smartphone. This has arguably reduced the demand for the former, not to mention that the price of electronic goods themselves have been declining despite better quality over time. Better quality of goods also reduces the turnover and needs to replace it, in effect, reducing the aggregate demand in the overall economy.

On the service side, the price of cable TV has been replaced by Netflix subscription, at the cost of the former’s revenue. This is also happening in the telecommunication sector in the form of switching from traditional line-based messaging services into internet-based services. All these anecdotes benefit consumers and push inflation lower. By optimizing the utility function, consumers can enjoy higher value for each dollar spent. Services will likely continue to flourish as younger people spend on experiences rather than accumulating goods, which has been made more accessible through the concept of sharing economy. Finally, the trend toward minimalism and awareness of excessive consumption have also initiate a trend among conscious and educated youngster to buy fewer but higher quality goods that will last them for a long time.

The bottom line is that current low inflationary period is unlikely to be sustained forever and a higher service inflation combined with changing consumption basket weights from goods to services are likely to drive inflationary pressure higher

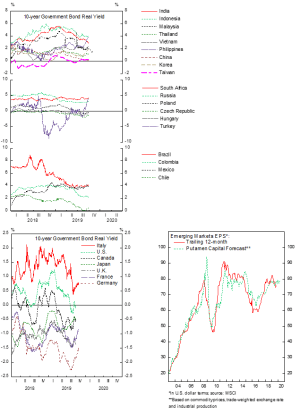

Another Up-Cycle in the Making: Country Selection

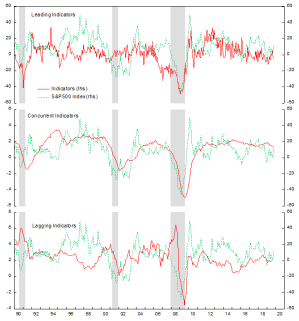

Despite the weak Chinese Q3 growth data, we are seeing an improving condition of global growth, coming from the higher than expected U.S. Q3 growth. Our leading economic indicator for the U.S. has been pointing higher for the last few months, helped by the Fed easing effort and lower yield. Some thoughts on the world:

- Europe is still slowing down, but the cycle is late

- Improvement in macro sentiment of late as a result of “phase one” U.S.-China trade deal and progress on Brexit.

- Rebound on German manufacturing PMI and South Korean exports number as a confirmation for bottoming in trade slowdown.

- Mining firms are likely winner from reflating world. The divergence between Chilean equities and copper price has been wide as a result of civil turmoil of late, giving investors the opportunity to buy Chilean copper firms at a cheaper valuation.

- Given that now government bond yield is at a low level, fiscal spending is more affordable to many countries without stretching their fiscal limit.

Bottom line: stay positive on Turkey, Mexico and Chile stocks.

Copyright © 2019, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.