Download PDF: Monthly_201910

Risk and Return

This month marks the 1st anniversary of Putamen Capital, with Putamen Growth Fund (PGF), our sole and flagship fund, recorded 34.15% return between October 24th, 2018 and September 30th, 2019. Since the inception, we have been exploring various type of equity, option and volatility strategy across developed and emerging market assets, and continuously improving our method in selecting high-quality investments and allocating capital. We designed various strategies to weather equity volatility while trying to capture alpha from market timing strategy, creating an all-weather portfolio that performed better than standard risk parity strategy.

On the quantitative side, we have developed, refined and back tested 4 models that we continuously monitor on both monthly and daily basis: Global Asset Allocation Strategy (GAAS), Global Equity Strategy (GES), Volatility Strategy (VS) and Global Equity Relative Strategy (GERS). These strategies have been proven to add value to our screening and investment process, saving us time in spotting the best opportunities available and enhance our fund’s return performance; details are available on the menu options of this website. However, it is important to state that PGF is not a pure quantitative fund. It is managed based on combination of quantitative inputs and top-down macro call.

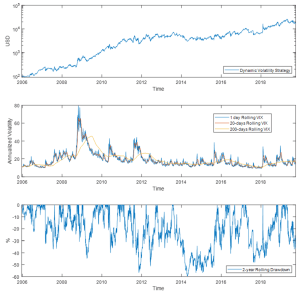

Our greatest drawdown happened last August when the trade war was escalating and equities tumbled globally. Although PGF’s volatility, measured by traditional standard deviation, is greater than S&P500, Developed Markets ex-US & Canada and World equities, when measured by its downward deviation it is very close to world equity volatility. This mainly attributed to our option strategy, whose payoff is asymmetric, limiting our downside deviation. Looking back, we estimated that we could have delivered 20-30% higher return by optimizing our capital allocation and utilizing 90-100% of our capital.

Lessons Learned

In the past year, our biggest winner has also come from our biggest loser. We have been positive on Turkish and Mexican equities since early this year and overweight both countries in our portfolio. We dialed back our positioning when risk aversion increased and bought back securities when we think the worst is over. In our monthly publication several months ago, we recommended a hedging strategy using call option on VIX, which we think is probably the most effective and cost-efficient hedging tools when compared to other alternatives (put option on equity index, short index futures, etc.). We did implement the strategy when volatility spikes in August and were able to profit from the hedge, reducing our drawdown significantly.

Over the past year, there are several important lessons that we learned. The first lesson is to differentiate the force driving improvement in the economic data and rising asset prices. Being right in predicting economic improvement does not always translate to profit from buying the country’s assets. We experienced drawdown from our long position in Turkish equity in the first half the year when concern about reserves and possible sanction from U.S was brewing, forcing us to re-evaluate our investment thesis and limit our risk. Inflation, which peaked at October last year was declining as projected, current account balance adjusted and several confidence measures were improving, but equity prices were falling.

The second lesson we learned was that even when valuation is extremely cheap, and the economy is improving from the low, rapid adjustment in asset prices is prone to a sudden pullback arising from political risk. Such is the case for Argentine and Turkey recovery: Turkey suffered from confidence on its Central Bank after meddling from Erdogan and CFK win on Argentine primary election sent its asset prices falling. This are risks that are difficult to financially quantify, but nevertheless important to monitor. Extreme hardship on country’s economy often lead to change in political leadership.

The third lesson is realizing that missing a fantastic opportunity could emotionally hurt more than being in a losing position. We missed the bull market on EM bonds, particularly Brazilian, Mexican and Indonesian bonds, due to our limitation on initiating long position in foreign countries’ sovereign bonds. We have been very positive on these countries yield last year, a position which would have returned over 20% over the period. This is one of the reasons that PGF usually only use 60%-80% of the fund`s capital, for us to be able to deploy capital decisively when investment opportunities arise. PGF also has margin trading capacity up to 200% capital, which we have not use so far, allowing us to do derivative overlay to hedge our underlying position when fully invested. In short, we are looking forward to further optimize the return of our capital.

Opportunities and Risk in the Current Global Landscape

On the current investment landscape, we tilted toward a higher risk tolerance portfolio as we believe global equity ex-U.S. offers a relatively good value compared to bonds and other asset classes. We expect public equity to outperform private one, as private capital seems to be adjusting down its valuation froth after several IPO flops this year. The current environment resembles classic late cycle behavior: 1) Easing monetary cycle across global Central Bank 2) Increasing pressure for government to ease fiscal 3) Weak commodity prices 4) Pessimism among investors (% of cash holding, equity-bond allocation). We summarized our thought framework in the four quadrants below.

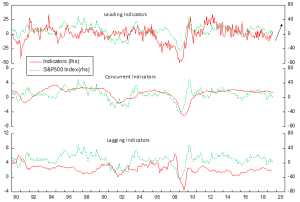

Contrary to most bearish call on equities, we currently see low odds of recession in the U.S. but agree that valuation of U.S. stocks is on the high side. We have been bearish on the S&P500 since last year and the market has not moved much since. Economic data from U.S., however, has surprised to the upside in recent months after a slowdown this year. This underpin our conviction that the U.S. economy is slowly recovering, following the rebound in some Asian and Latin American countries.

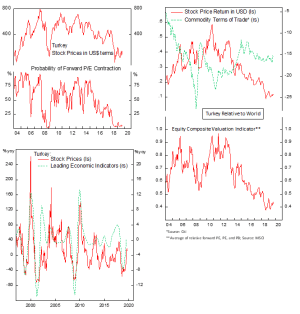

For this month, our internal model shows that there are fewer countries with historically depressed valuation, as many countries, such as South Korea, Mexico and Japan, have recovered 10-15% from their recent low. Shown below is several countries whose trading at a low forward P/E ratio based on its historical averages and worth investigating further.

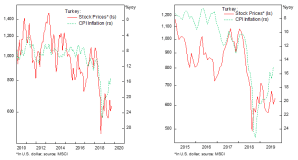

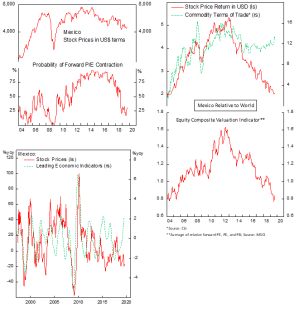

We maintained our positive view on Turkey, Colombia, Japan, Mexico and Argentina for equity selection. Several other countries that are also interesting include Hong Kong, Singapore, Poland, Austria and Czech Republic. The recent rally on Chilean equity, however, has made the stock market valuation back to its median. This is normal during the recovery period when investors are expecting improvement in earnings.

Mexico

Poland

Turkey

Model Performance Update

Global Asset Allocation Strategy (GAAS)

Our flagship GAAS model returned 2.4% in September, slightly below MSCI ACWI 2.6% rise for the month, as the model was whipsawed by the marked increase in daily volatility. Although our Global Equity Strategy (GES) model performed well during the month, the Volatility Strategy (VS) model has been dragging down the performance of GAAS model (see below). This brings GAAS model return to 2999% (27.8% annually) since its inception in December 2005 compared to MSCI ACWI 140% (2.5%) rise during the same period.

Global Equity Strategy (GES)

Our in-house equity allocation model returned 4.9% in September, outpacing the 2.6% rise in our benchmark. The model recommendation to overweight Mexican equities has largely paid off. This brings the model performance to 1658% (22.5% annually) return since its inception in December 2005.

Volatility Strategy (VS)

The marked increase in volatility due to news flow related to the trade war and prospect of restricting capital investment from China have driven the VIX index swinging more wildly in September. Our volatility strategy model declined 3.5% in the month, driving our VS portfolio down 36.2% from its peak in April this year. Since its inception in December 2005, however, the model delivered 16702% return, or 44.7% annually.

Global Equity Relative Strategy (GERS)

The Global Equity Relative Strategy (GERS) model returned 4.96% in September, outperforming the MSCI ACWI 1.94% increase. This brings our model return to 4212% (27.1% annually) since inception (January 2004) compared to MSCI ACWI 105% (4.7% annually) rise during the same period. One recommendation that strike us as interesting is the recommendation for Mexican equities, which is also supported by the GES model.

Investment Strategy Going Forward

There are two big themes that we think is likely to happen in the coming decade:

- Commodity bull run from big push on infrastructure spending in emerging markets, demand for electronics, electric cars and IoT application. Base metals are likely to outperform gold from demand pull.

- Fiat money depreciation will drive gain for precious metal/gold. Although we are more positive on base metals, we also believe gold will structurally benefit and deserves a strategic position in investor’s portfolio. Massive easing across the world and competitive devaluation among countries are likely to boost real asset (property, etc.) prices and create a bubble.

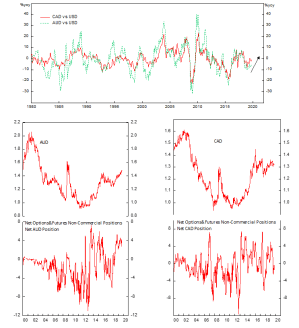

On a more tactical note, we will continue to manage our portfolio using derivatives position: 1) Long call options on selected countries, focusing on those with higher growth profile and attractive valuation 2) Long copper futures 3) Hold gold as strategic allocation 4) Long commodity currencies (CAD, AUD)