Download PDF: Mexico_Reaching_Cyclical_Bottom

- It is likely that Mexican economic condition will improve going forward. Various indicators are at level comparable to those in 2013 and 2016 downturn and monetary stimulus is currently on progress. The easing stance of global monetary policy and reflationary effort in China are further likely to ease domestic condition and benefit Mexican exports.

- Total exports have been declining and may not yet bottom, but automotive exports have stabilized at 10% growth rate. However, the political gridlock in US part for the USMCA ratification possess downside risk to both Mexico and Canada domestic economy. Should the democrat use the ratification to block or delay Trump’s USMCA deal, Mexican assets will suffer.

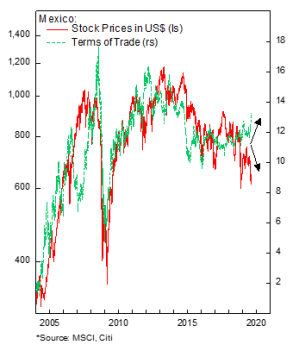

- Terms of trade, which historically has been moving closely with stock prices, has improved significantly while equity tumbled. With the inflation and currency under control, the equity risk premium is likely attributed to the political risk in the country. This divergence is historically unsustainable and considering the valuation of Mexican stocks, our bet is for equity prices to catch the upside.

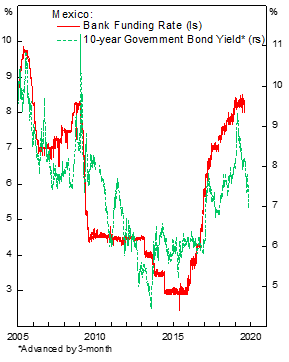

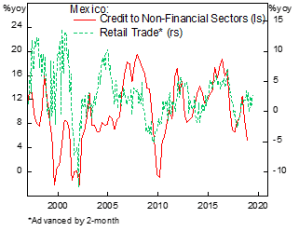

- Financials are especially attractive among Mexican stocks. First, the cyclical nature of the sector and current bottoming of the cycle has put relative valuation is on the cheaper side of the trading range since 2004, providing support to multiples. Earnings outlook is likely to improve as well: the dramatic decline in government borrowing cost should translate to much lower bank funding rate and credit growth is set to go higher.

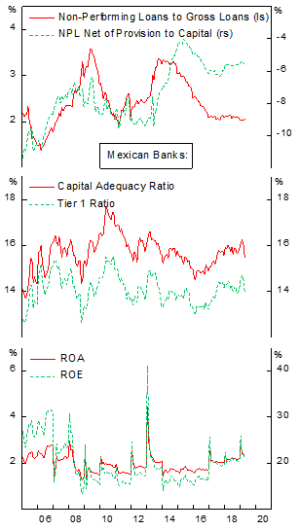

- Banking NPL has ticked up slightly, albeit at a still very low level, as a result of the downturn. An easier financing access and income growth should put a lid to NPL growth. Provisioning in the banking sector also remains aggressive and capital ratio is well above the minimum requirements. There is little sign that the banking sector is under stress and the risk of capital flight is low, assuming the peso remains stable.