Download PDF: Indonesia Research

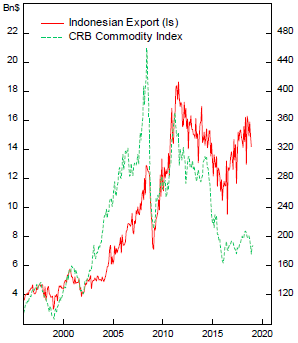

| Two decades after the Asian Financial Crisis that created a havoc in Indonesian economy and politics, Indonesian role in global trade has been stagnating… |

| … and is still very much influenced by the fluctuation in commodity prices, although at a lesser extent. |

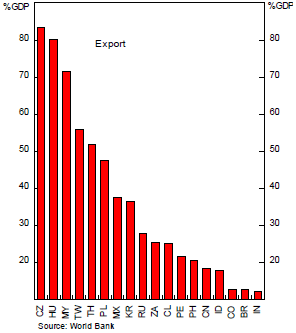

| Relative to other Emerging Market countries, Indonesia’s integration to the world economy is relatively low. |

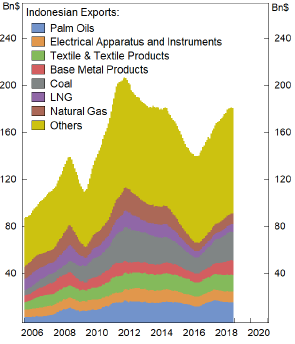

| Indonesian exports are currently still dominated by raw materials and other low value-added goods, with less than 10% of its exports being electronic products. |

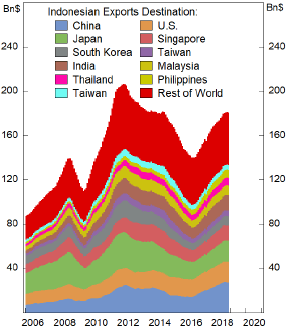

| Global Financial Crisis has also shifted the main destination of Indonesian export from Japan to China, contributed by the increasing demand of palm oil, coal, rubber and oil & gas. |

| However, these products tend to be unrefined and has a low value added since China has a large capacity to process the raw materials themselves, unlike electronic exports from U.S., Korea and Taiwan. |

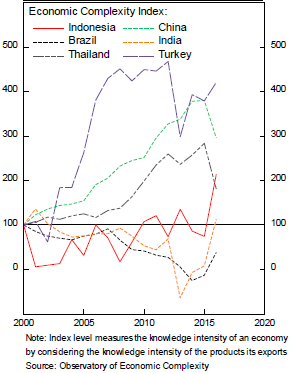

| Although the trend of its knowledge base is trending higher. |

| Several obstacles hinder Indonesian economy to progress toward higher value chain: low labor quality, unfriendly government regulation and lack of reliable infrastructure. |

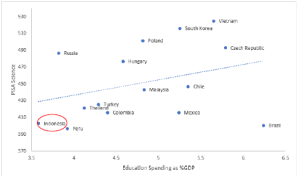

| Although the government has been increasing education spending in past years to improve teaching quality, the amount is still very low compared to its peers and the efficiency and implementation have been disappointing. Inspections by Department of Education find that both teachers and students are often absent during school hours, as often reported. As a result, educational attainment is one of the lowest among EM countries. |

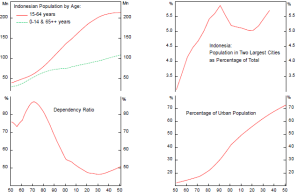

| The next two decades will be the sweet spot of Indonesian demographic profile, but the low education results in unproductive worker concentrated in low value-added sectors. |

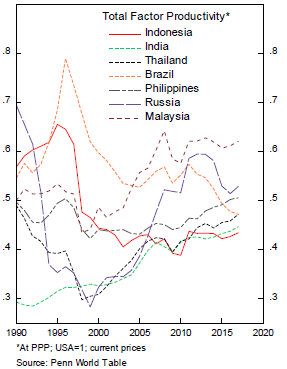

| Indonesia’s total factor productivity has been stagnating since the Asian crisis and lagging India, Thailand and Malaysia. Low openness, restriction on trade and investment, import tariff hinder the transfer of technology and manufacturing know how, reducing TFP. |

| University graduates are taking a higher share of the unemployed population, although the rate is declining. Informal employment has also declined but remained high at 58% of total employment due to rigid labor regulations |

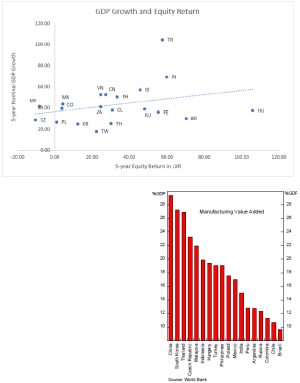

| Foreign Direct Investment to Indonesia is on the higher side among EM countries, highlighting the growth potential of the country, next to BRIC and Mexico. |

| Rules capping the government deficit up to 3% GDP has limit the accumulation of public debt.

Subsidies has been declining as well and channeled into more productive expenditure, such as increasing infrastructure spending that will raise output growth. Streamlining of land acquisition process by the current administration has also expedited infrastructure projects. State Law No. 17 2003 limits the budget deficit to 3% GDP and government debt to less than 60% GDP. During the 98’ crisis, 90% debt to GDP ratio results in government taking over corporate debt and banking crisis. |

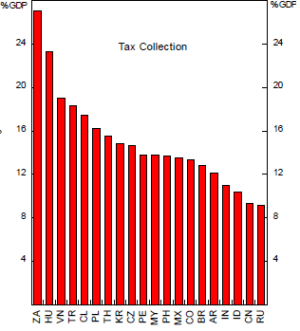

| Government tax collection could be increased to fund infrastructure projects and education that would support higher long-term growth. |

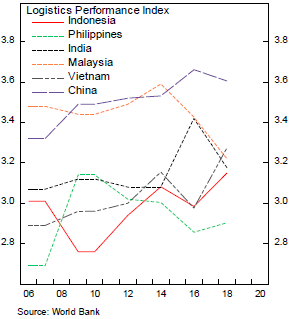

| Due to its islandic geography, Indonesian logistics costs are among the highest in Asia, 25% GDP relative to EM Asia range of 13-20% GDP |

External Risk

| Unlike in 2015, higher portion of Indonesia’s deficit is financed by FDI that is less prone to hot money outflow.

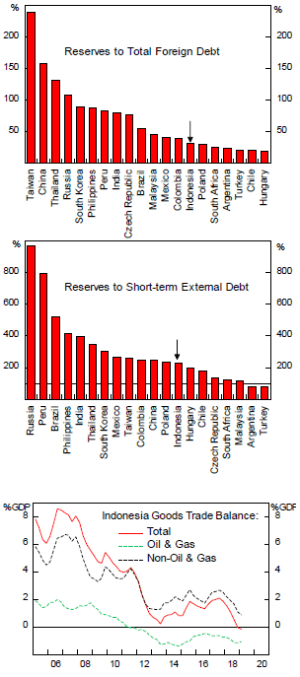

As a net energy importer, subdued oil price is good news for both inflation and current account. FX reserve is adequate but is on the lower side among EM countries. |

| International reserves have mostly fluctuated between US$ 100-130 billion since 2011. Deterioration in external risk profile is mostly due to increase in short-term external debt in the last decade, from US$ 35 bn in 2011 to 54 bn in 2019Q1 |

| High foreign holding risks yields to go much higher during period of risk aversion |

| Mismatch in funding currency and revenue has been minimized by issuing more domestic currency bonds

Corporate balance sheet is relatively strong and has lower leverage than peers, FX corporate debt is concentrated in manufacturing and commodities sectors that has natural hedging tendency through FX revenue. In 2015, regulation requires hedging at least 25% of corporate net FX liabilities, if it has a foreign debt maturing within 6 months, and also maintaining short term liquidity ratio (fx asset/liab) above 70% and have credit rating above or equal to BB- to borrow externally. |

Long-term Stuff

Investment Thesis: Long Indonesian & Short Indian Financials

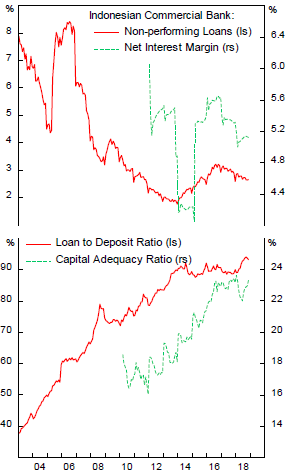

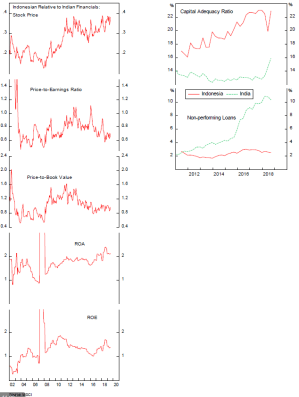

| Indonesian banks balance sheet is much more robust today with NPL coming down after the commodity bust, especially coal, in 2015. After the trauma of 98’ crisis, Indonesian banks have been very prudent in lending and provisioning that capital adequacy is among the highest in the world at 23% of risk-weighted assets.

It was also argued, on the other hand, that the high Net Interest Margin in Indonesian banks have slowed credit intermediation to the private sector, hampering growth of the economy. Both Indonesian and Indian financials are trading at elevated multiple relative to EM due to the superior profitability compared to other sectors historically. Profitability and Solvency of Indonesian banks are better than the Indian counterparts, mainly due to the relatively conservative lending practice among the top 5 SOE and private banks. Indonesian banks are also trading at a discount relative to Indian: PBV multiple are trading at 2.74x compared to 2.83x for India and P/E are trading at only 17.6x compared to 25.1x for the later, largely due to heavy provisioning of Indian banks of late.

|

Copyright © 2019, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.