This year has been particularly difficult for most investors as there are few places to hide from inflation and rising cost of capital. Both equity and long-term bonds are down over 20% YTD, and even the value of cash is being eaten out by inflation, which rose as high as 9.1% y/y back in June. Since early this year we have taken a bearish view on risk assets amid the outlook for slowing growth and tighter monetary policy by the Fed, but for the past several months we have been wrong in calling the Fed Pivot too early amid inflation prints keep on surprising to the upside, even as leading indicators are showing signs that various components of inflation are coming down and growth is slowing faster than expected.

In this month piece we outlined ten predictions for the next year, based on the ongoing economic trajectory and growing geopolitical risks in both Asia and Europe. Although it is nearly impossible to predict the outcome of Russia-Ukraine war and the Taiwan issue, recent developments point to the risk of escalation as neither the Russian nor the Chinese government could afford to be seen as weak by their domestic audience.

- The End of the Era of Cheap Money: Drought in Startups Funding

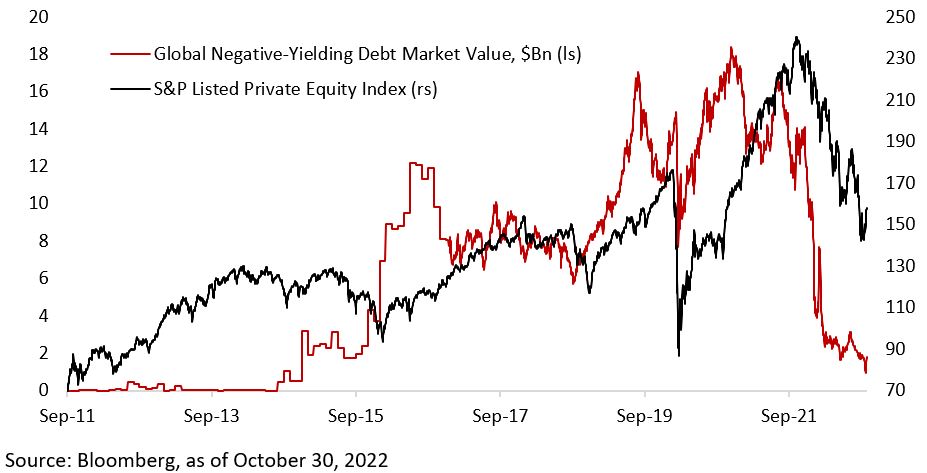

It was akin to waking up from a dream. A long, wonderful dream where one could borrow at a negative rate – meaning that borrowers are getting paid for taking credit – and money was being thrown to anyone with grandeur ideas of conquering market share in any industry, especially in the tech sector. At one point of time in the dream, wealth was created out of thin air by the young people who were obsessed by trading virtual coins and digital pictures at an increasingly elevated price. Making profits was as easy as growing tulips.

That was the state of the investment landscape over the past decade. An era of easy money that started with rounds of quantitative easing (QE) following the Global Financial Crisis in 2008. But that chapter is now ending, and investors no longer think that lending at a negative rate makes any sense. Risk-free bond yields have risen from as low as 0.5% thirty months ago to 4% currently, eight times increase, which drag down valuation for all assets. Currently, the worry lies in the value of private equity holdings of pensions and institutional funds, which have yet to reflect the valuation downgrade of its public market equivalent. As cost of capital increases, startups will likely face a drought in funding, especially as venture capital and private equity firms try to avoid a down round.

2. China Lashes Out: Taiwan and Semis

In today’s world, chips permeate all aspects of our life, from powering our smartphones, TVs, laptops, up to ballistic missiles. War is no longer decided by which side has more tanks, fighter planes, or infantry. Drones and smart-missiles that could lock in target with high precision are increasingly changing the balance of power in the battlefield. This made access to advanced chips a matter of national security that both the West and China could no longer take for granted. In October, the U.S. announced a new export control that prohibit the sale of advanced chips and equipment needed to make them to China, while also effectively banning U.S. citizens, residents, or green card holders to aid China develop its own semiconductor industry and catch up to the West. This matters greatly to China, who is still highly reliant on imports of advanced technology to power its industry, despite efforts to push for home-grown innovation. With a single company in Taiwan producing 92% of world’s most advanced chips, the geopolitical stakes could not be higher.

3. Deep Recession in the U.S.: S&P 500 Bottoms Below 3000.

Leading indicators have continued to deteriorate in recent weeks with both manufacturing and service PMI falling below 50 – the expansion/contraction threshold. Meanwhile, our growth tax indicator continues to indicate significant tightening in monetary conditions, which historically led to a fall in S&P 500 earnings. The scatterplot below shows that the current level of growth tax is consistent with a 20% drop in S&P 500 earnings, which would translate to forward earnings of around $180. Applying a 15x forward earnings multiple – slightly below historical average of 16x – would translate to S&P 500 trading at 2700.

4. Inflation Turns into Deflation for Some Categories of Goods, Disinflationary Process Continues

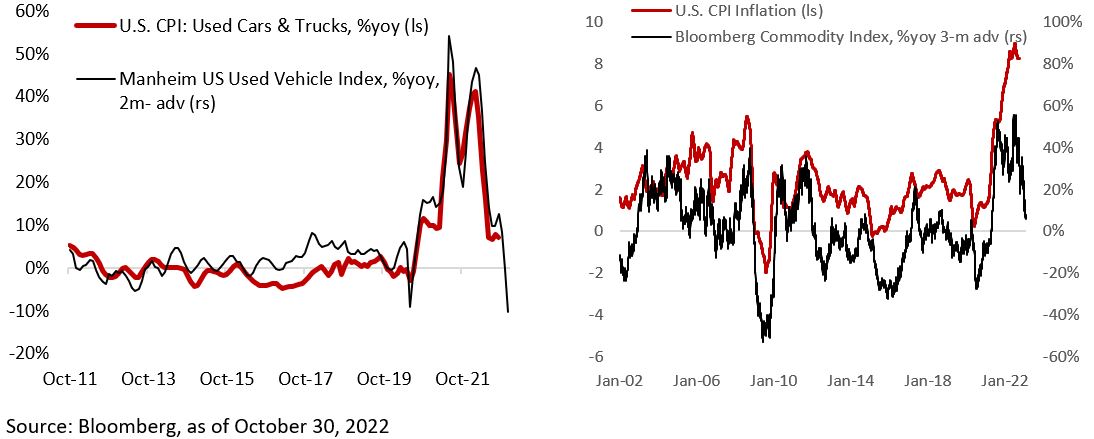

Inflation has been higher for longer this year even as the Fed continues to deliver sizeable rate hike. Increases in wage demand have translated into the fear that inflation expectations are becoming unmoored, which would complicate Fed’s job in bringing inflation closer to its 2% target. The upside surprises on headline inflation, however, have been mainly driven by the increase in shelter cost, food prices, and more recently medical service cost. Meanwhile, prices for some categories of goods, such as used cars, have turned into outright deflation. Shelter cost inflation, which account for 30% of the CPI basket, will also likely cool down by the middle of next year, as recent rental price index from Zillow indicates. More importantly, the lagged impact of monetary policy to the real economy has yet to be fully realized. With commodity prices tumbling (oil, copper, iron ore, etc.) on a year-on-year basis, headline CPI inflation should also turn lower in 2023.

5. Unemployment Rate in the U.S. Jump to Above 6%

Strong U.S. economic growth and weak recovery in labor force participation rate have widened the imbalance of supply/demand for labor this year, with data from Bureau of Labor Statistics showing that there were two job openings for every unemployed person as recently as in August. However, we think that the U.S. will undergo through a deep, rather than shallow, recession in 2023, which would translate to a cooling in labor demand. Already, we are seeing companies in the more cycle-sensitive sectors laying off their employees of late. On the supply side, we expect more people to join the labor force as the cost-of-living crisis bites. Our growth tax indicator continues to point to a much higher unemployment rate in the 18 months ahead.

6. Russia Loses the War in Ukraine

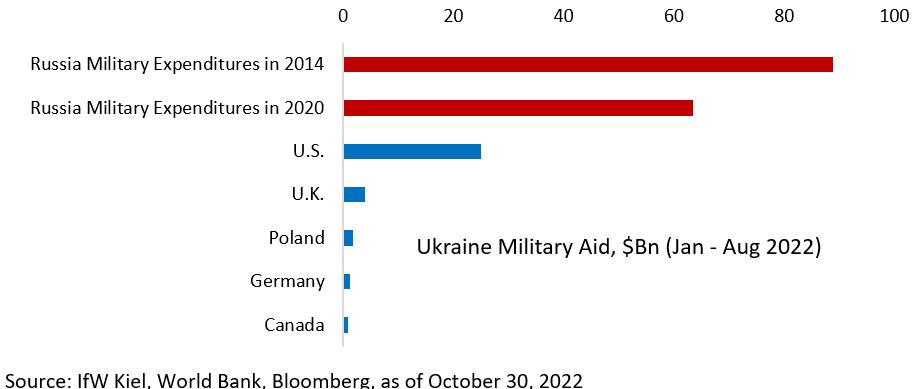

Eight months following Russian invasion of Ukraine, the balance of power is increasingly shifting in the favor of the latter amid gains in the battlefield and continuation of support by Western democracies. Crucially, the economic and financial impacts of the war are increasingly contained, with oil falling from $120/bbl to $80/bbl and European gas storage rising to above 90% capacity, alleviating the fear of a cold Winter season ahead. There is no doubt that elevated oil prices enhance Russia’s ability to finance the war, but the exodus of Russia’s best and brightest should worsen the country’s long-term growth trajectory. Moreover, reports from the battlefield highlights the lack of training and weapons of Russian army, at a time when Ukrainian army continues to receive advanced weapon arsenal from the U.S. and Germany. It will be increasingly difficult for President Putin to frame Russia as the winner of the war he started to his domestic audience.

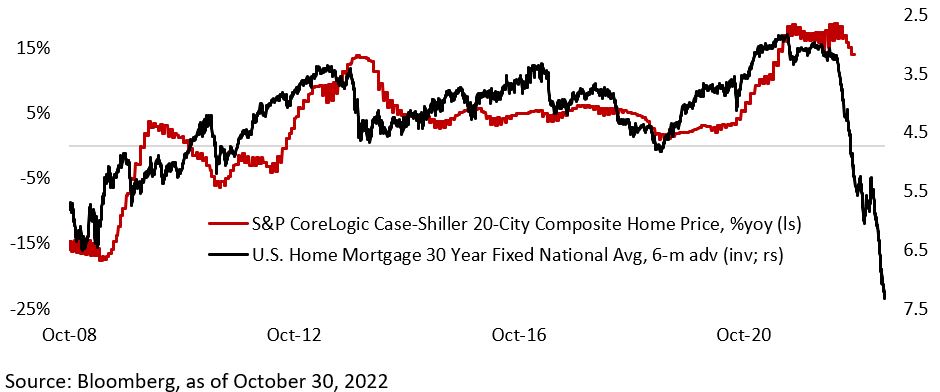

7. House Price Correction in the Developed Economies

Following a boom during the pandemic amid record-low mortgage rate and demand for larger living space, real estate activity has been cooling rapidly this year as 30-year fixed mortgage rate rose from 3% to above 7.3%. High-frequency indicators are pointing to a slump in housing starts, sales, and prices in the coming quarters. As consumers battle against higher prices of daily necessities and wages fail to catch up with inflation, their capacity to spend on housing has been significantly curtailed. More importantly, the fundamentals are against higher house price amid elevated price-to-income and price-to-rent in the developed countries. Limited income and rent growth mean prices will have to be the one to adjust for the ratios to revert to historical averages.

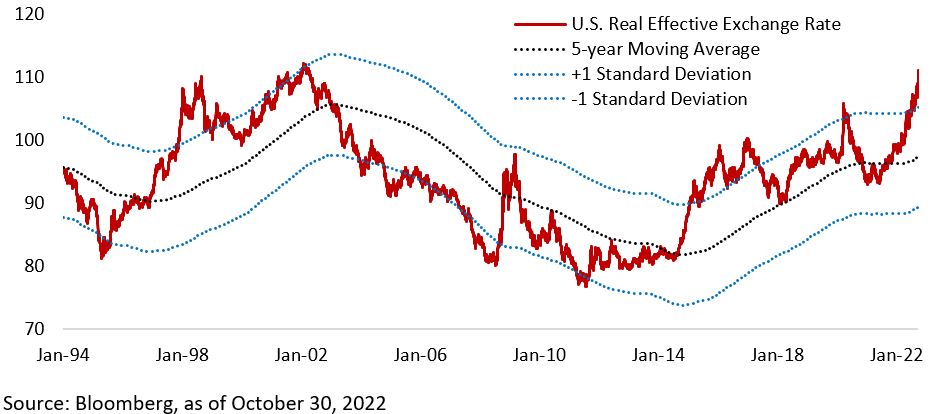

8. The Dollar Loses its Luster

The greenback has advanced over 15% over the past year in real terms relative to its trade partners. A more aggressive Fed, capital flow into U.S. assets, and weak growth outlook across Europe and China have all exacerbated the spike in the dollar, which currently is overbought and trading at an expensive valuation. There are two primary factors that could reverse this trend. First, the market is increasingly pricing a Fed Pivot as the whole yield curve becomes inverted. A narrowing of yield differential between the U.S. and other central banks should ease the attractiveness of the dollar and make holding foreign assets more attractive. Second, growth outside U.S. could start to pick up in 2023. Chinese credit impulse has been picking up momentum and Europe seem to be able to avoid the worst-case scenario related to the energy crisis. A weaker U.S. growth relative to other regions historically coincide with periods of a weaker dollar.

9. U.S. 10-year Treasury Yield Fall Below 2.5%

Still on the theme of a Fed Pivot, we believe Treasury bonds are among the most attractive assets to own going into the next year. U.S. economic growth is slowing rapidly and the Fed may be nearing a pause in the tightening cycle. Should a recession occur in the U.S. and inflation continues to move lower, as we expect, there is significant room for the Fed to cut policy rate below the 2.5% neutral estimate. Copper-to-gold ratio, which historically moved alongside long-term yields, currently points to a fair value for U.S. 10-year Treasury below 2%.

10. Turkish Lira Crashes, Drop Below 25 Against the Dollar.

The country is not immune from inflation, which rose to 83% y/y in September, but its policy response is certainly unique. The central bank of Turkey has continued to cut interest rate to 10.5% from its recent peak of 19% in September 2021, when inflation was still at 19.3%. Unorthodox monetary policy, government guarantee on Lira deposit, and FX interventions have dominated Turkish macro landscape since the currency crisis that began in 2018. With the probability of changes in policy low, the Lira will likely slide below 25 vs the U.S. dollar in 2023.

Copyright © 2022, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.