Market has been trading lower since mid-August peak and we are revisiting our recommendation on sectors given the sharp moves in cyclical and defensives of late. Below are our sector view with a brief rationale and supporting charts.

Healthcare: Overweigh (2-4%)

Pro: uncorrelated to the cycle and historically outperformed due to earnings resilience during downturn. Valuation is still cheap at 30th percentile on CAPE and forward earnings basis.

Cons: overbought

Strategy: there is plenty of room to further outperform in the coming 3-6 months, remain overweigh.

Consumer Staples: Overweigh (1-2%)

Pro: Margin resilience during growth downturn and defensive.

Cons: High cost and wage pressure might temper staples’ margin during the current cycle, but little signs so far (grocers could still pass cost increase to consumers, despite trading down behavior observed). Valuation is near record high level on forward earnings basis, but reasonably cheap based on cyclically adjusted earnings.

Strategy: keep modest overweigh and prepare to cut down allocation once equity market looks to bottom. Still some room to outperform if deep recession ensues, good hedge strategy.

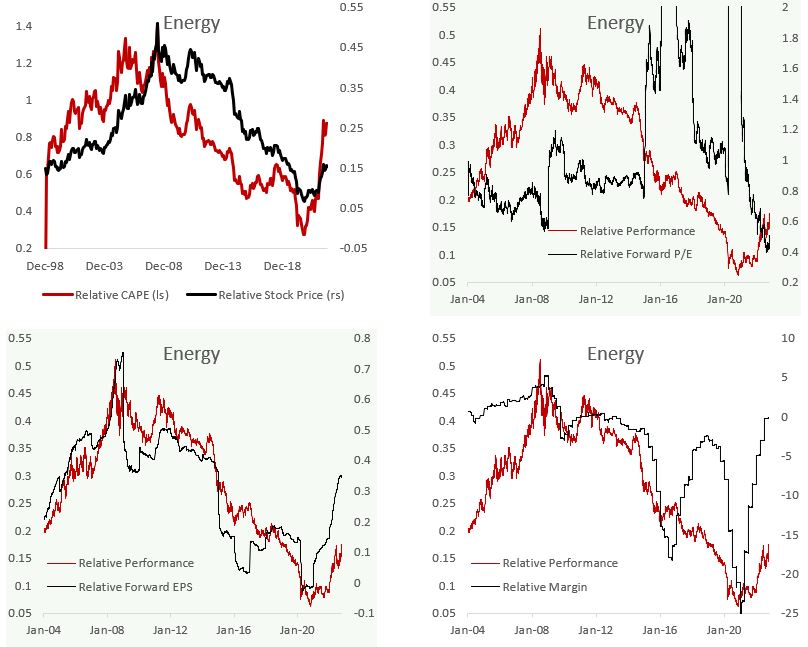

Energy: Overweigh (1-2%)

Pro: medium and long-term supply outlook, SPR refill, valuation and attractive yields.

Cons: near-term demand outlook is deteriorating, strong dollar and yield, U.S. policy to bring prices down.

Strategy: go slight overweigh despite worsening economic outlook as OPEC+ set to counter falling demand by supply cut and the potential for further SPR release will be limited.

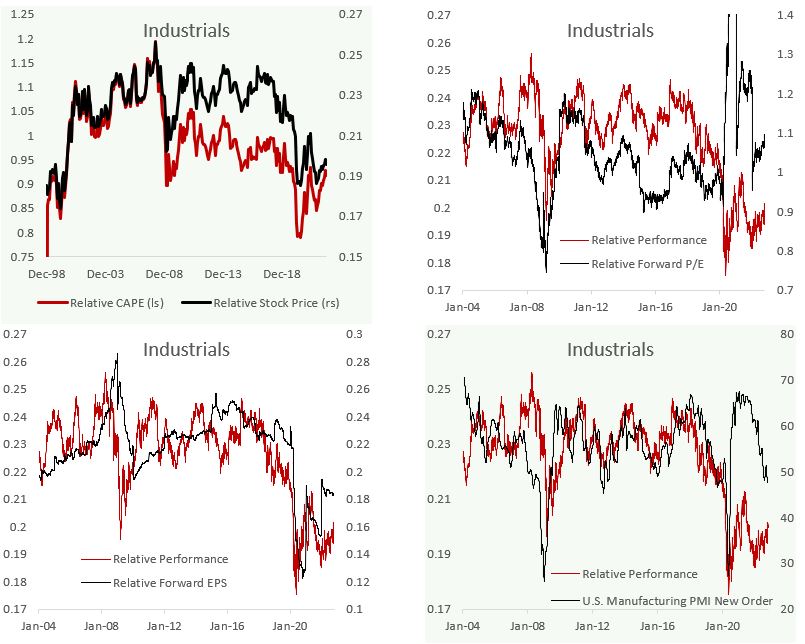

Industrials: Neutral/Overweigh (0-2%)

Pro: valuation is slightly cheap based on cyclically adjusted earnings; earnings have been outperforming benchmark and might continue to do so if recession disproportionately impact consumers rather than corporate. Technical is breaking the resistance.

Cons: historically underperformed during growth downturn, driven by both multiple and earnings.

Strategy: remain neutral for now

Info Tech: Neutral (0%)

Pro: Earnings growth will continue to structurally outpace benchmark, massive drivers of buyback.

Cons: Valuation froth remains (60th percentile based on CAPE) despite significant fall YTD, tight Fed policy continue to be a headwind.

Strategy: hold neutral position vs benchmark and prepare to increase weights once monetary policy reverse. The sector should outperform during cyclical downturn, but monetary policy remains the highlight currently.

Communications: Neutral (0%)

Pro: relatively cheap and multiples have fallen significantly YTD.

Cons: sector dominated by large, ads and consumer-based tech stocks (Google, Netflix, Facebook) that likely suffer in recession.

Strategy: remain neutral vs benchmark. Note that sector composition shifted drastically after 2019 reclassification of tech stocks.

Financials: Underweigh/Neutral (-1% to 0%)

Pro: potential to outperform if credit cycle is avoided, attractive valuation on both cyclically adjusted and forward basis, systemic risk is lower post-GFC reforms.

Cons: tail risk of blow up in CLO market, potential for consumer weakness and overshoot in NPL.

Strategy: remain underweigh

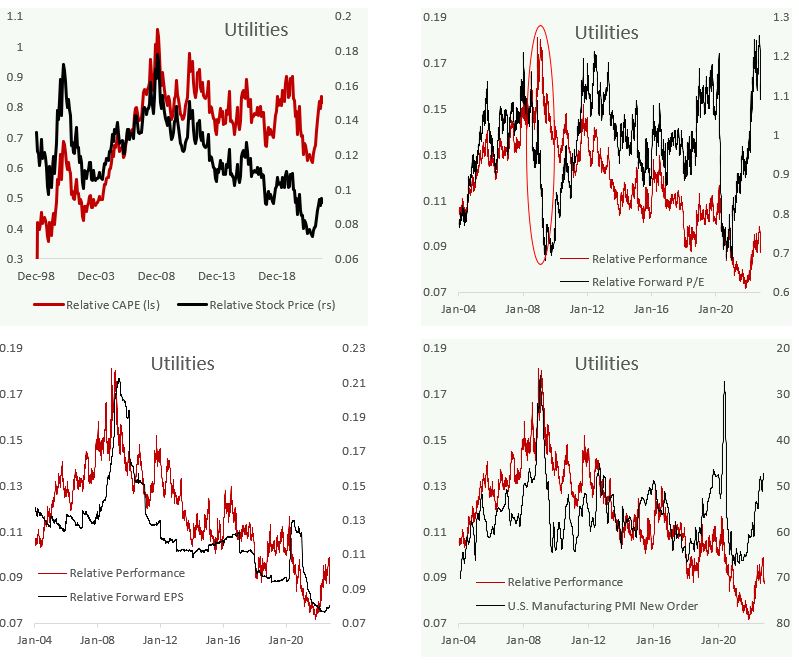

Utilities: Neutral/Underweigh (0% to -2%)

Pro: defensive and cash-like characteristics during downturn, oversold, there is room for further outperformance in deep recession scenario.

Cons: expensive on both cyclically adjusted and forward basis, structurally underperformed the market

Strategy: go underweigh to give place for higher cash balance and other defensives

Materials: Underweigh/Neutral (-2 to 0%)

Pro: attractive medium-term supply/demand outlook, tailwind from green infrastructure, valuation is reasonably cheap (for a reason).

Cons: cost pressure at a time when spot prices are falling, double whammy on margin. The sector is unlikely to outperform as long as dollar and yields is strong.

Strategy: keep underweigh to neutral for now and go to overweigh once global cycle bottoms (next year) and Chinese growth is rebounding.

Consumer Discretionary: Underweigh (-4 to -2%)

Pro: AMZN’s cloud exposure, hard to think other.

Cons: scream expensive based on CAPE and forward earnings basis, margin pressure as consumers cut back on discretionary spending, TSLA risk. Will likely underperform until few months before the cycle bottom.

Strategy: increase underweigh position to tactically benefit from the still expensive valuation and earnings risk. Go to neutral/overweigh once market bottom

Sector Charts

Copyright © 2022, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.