Download PDF:

Downgrade Chile and Peru to Underweight

Our recommendation to trim exposure to Chile and Peru is driven by three things: downside risk in copper price, rising political risk, and aggressive tightening by both countries’ central bank.

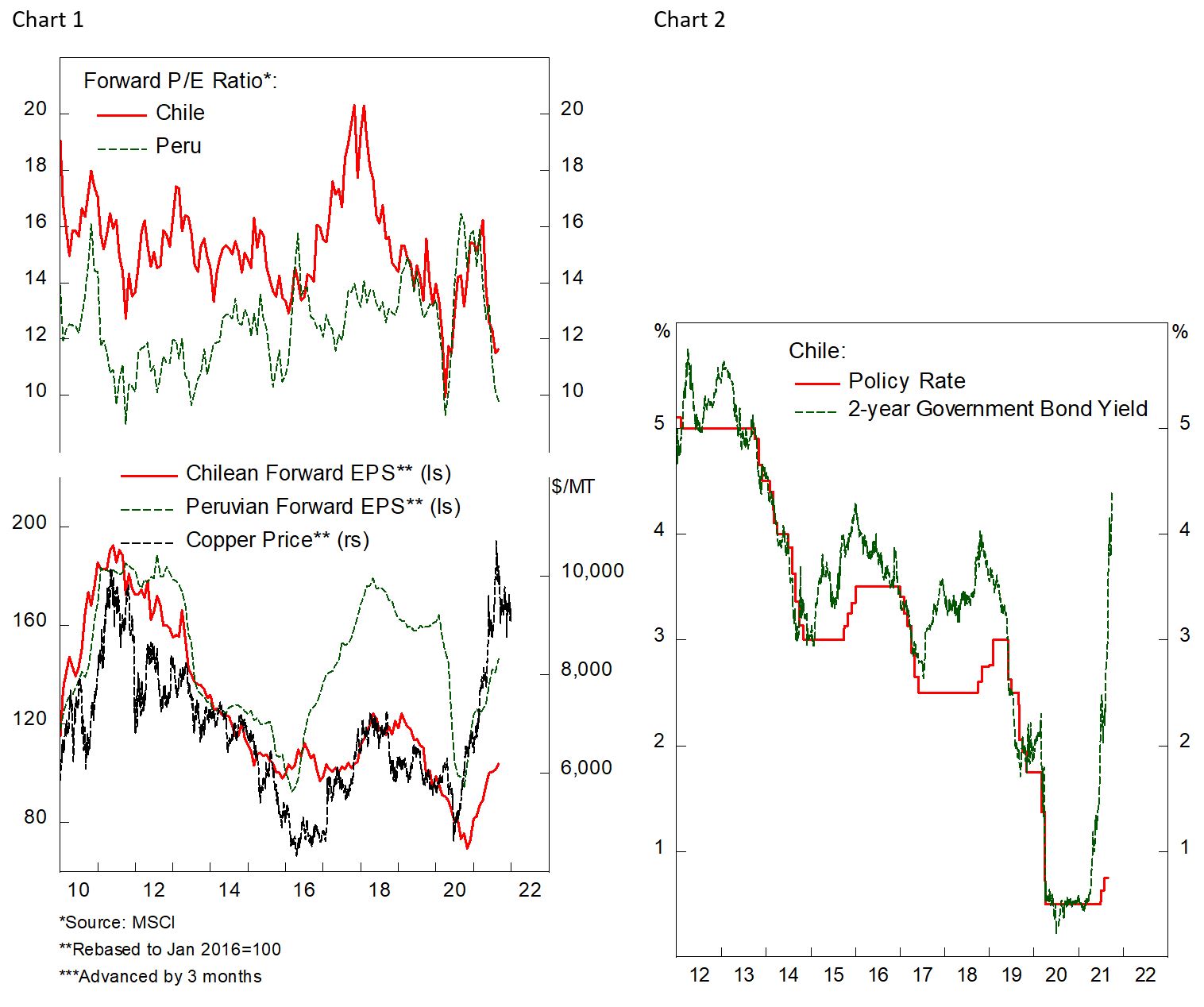

Slowdown in Chinese growth is going to weigh on commodity intensive Latam bourse heavily through the decline of industrial metal prices. Stocks and currencies of both Chile and Peru – the first and second largest copper producers in the world – are heavily influenced by the movement in copper prices. The risk is that with copper price currently trading at 40% premium compared to pre-pandemic level and demand leveling off while supply normalizes, a sizeable correction is likely in the short term. This could push equity prices lower as earnings tumbles, despite the cheap valuation (Chart 1). Moreover, strength in the dollar and rising real yield will further put downward pressure on industrial metal prices.

Meanwhile, rising political risk across Latin America and the region’s leftward shift has translated to higher cost of borrowing for these countries and bode poorly for their growth and investment outlook. For instance, investors have pull out their capital out of Peru en masse earlier this year following the victory of left-wing government, Chilean assets have been massively derated since the 2019 protest, and Brazilian democracy is put into a test by President Bolsonaro.

- The Peruvian sol is hovering at all time low while stocks are trading at only 10 times forward earnings amid the fear of drastic shift of the country’s economic model and governance. However, downside risk to Peruvian assets remains as sentiment is becoming ever more bearish, more recently highlighted by the government warning that miners should pay higher taxes or face nationalization. Deterioration in the country’s rule of law and attractiveness to private capital should keep risk premium on Peruvian assets elevated, at a time when the downside risk from lower copper prices and higher taxes weighs its earnings outlook.

- Chile is facing a divisive presidential election in November that warrants a more cautious stance. After failing to secure a majority in the constitutional body earlier this year, the fate of the incumbent centre-right party – currently polled second – to stay in power is questionable. The stake is high, as a drastic left-turn in executive power risk the country “safe haven” status in the region further put into question and potentially trigger another episode of capital outflow, not unlike what happened in Peru.

Lastly, both countries’ central bank has been raising rates to battle inflationary pressure, and borrowing rates are rising to a historically elevated level. Expectations for Chilean central bank to raise rates are rising fast as the government try to engineer a booming economy as November’s election loom, potentially forcing monetary policy to be tightened drastically afterward (Chart 2). The higher lending rates, however, will eventually choke domestic growth at a time when global cycle is already turning south.

Downgrade Brazil to Underweight

Brazil is among the more fragile EM countries and has historically suffered most during period of slowing global growth. Despite recent upheaval in domestic political environment already putting a dent on Brazilian assets, negative earnings outlook and deteriorating investor sentiment towards the country should mean Brazilian stocks underperforming the EM benchmark.

First, tailwind from rising commodity prices is reversing. Soybean and iron ore prices – Brazil’s major commodity exports – have corrected over 20% and 50%, respectively. Deterioration in the country’s terms of trade will translate to softer exports, fiscal revenue, and equity earnings in the coming months (Chart 3). Although valuations of Brazilian stocks are cheap, earnings expectation for Brazilian stocks has already turned negative amid the sharp fall in iron ore prices and will continue to lag, which makes Brazilian stocks currently unattractive.

Second, Brazilian borrowing rate has surged to above 11%, which means stock multiple will be pulled downward (Chart 4).

Lastly, political risk will continue to weigh Brazilian assets at least until next year’s election, as highlighted by the massive volatility during the rally President Bolsonaro did earlier last month. With his probability of winning next year’s election becoming slimmer, it is not unlikely that the president will try to hold to power through unconstitutional means and stoking negative reaction from the market.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.