Download PDF:

The global economic boom unfolding in the past year is showing signs of moderation, with data from China – the first country to suffer and come out of the pandemic – currently signaling a contraction in manufacturing activities. It is very likely that the U.S. and Euro area will also see a deceleration in growth numbers in the coming months, although the stalling speed is difficult to forecast (Chart 1).

More importantly, after cutting the reserve requirement ratio in July reflationary efforts by Chinese authorities have so far come short and the weakening economy is weighing the performance of its cyclical stocks. Meanwhile, global liquidity is set to tighten as the Fed and ECB taper bond purchases, adding downside risk to EM assets. Taken together, slowing world economy bodes poorly for EM equity earnings, especially those sensitive to the fluctuation in commodity prices, and tightening global liquidity could push the dollar higher and multiple lower.

We continue to advocate overweight China and EM Asia in an EM portfolio while underweight commodity intensive Latam bourses, for several reasons:

- Table 1 shows the performance of EM country stocks relative to EM benchmark. EM Asian bourse historically outperformed during Chinese easing cycle due to its diversified economy and less reliance on commodity prices. We expect a replay of such episodes with few exceptions related to the currently high energy prices.

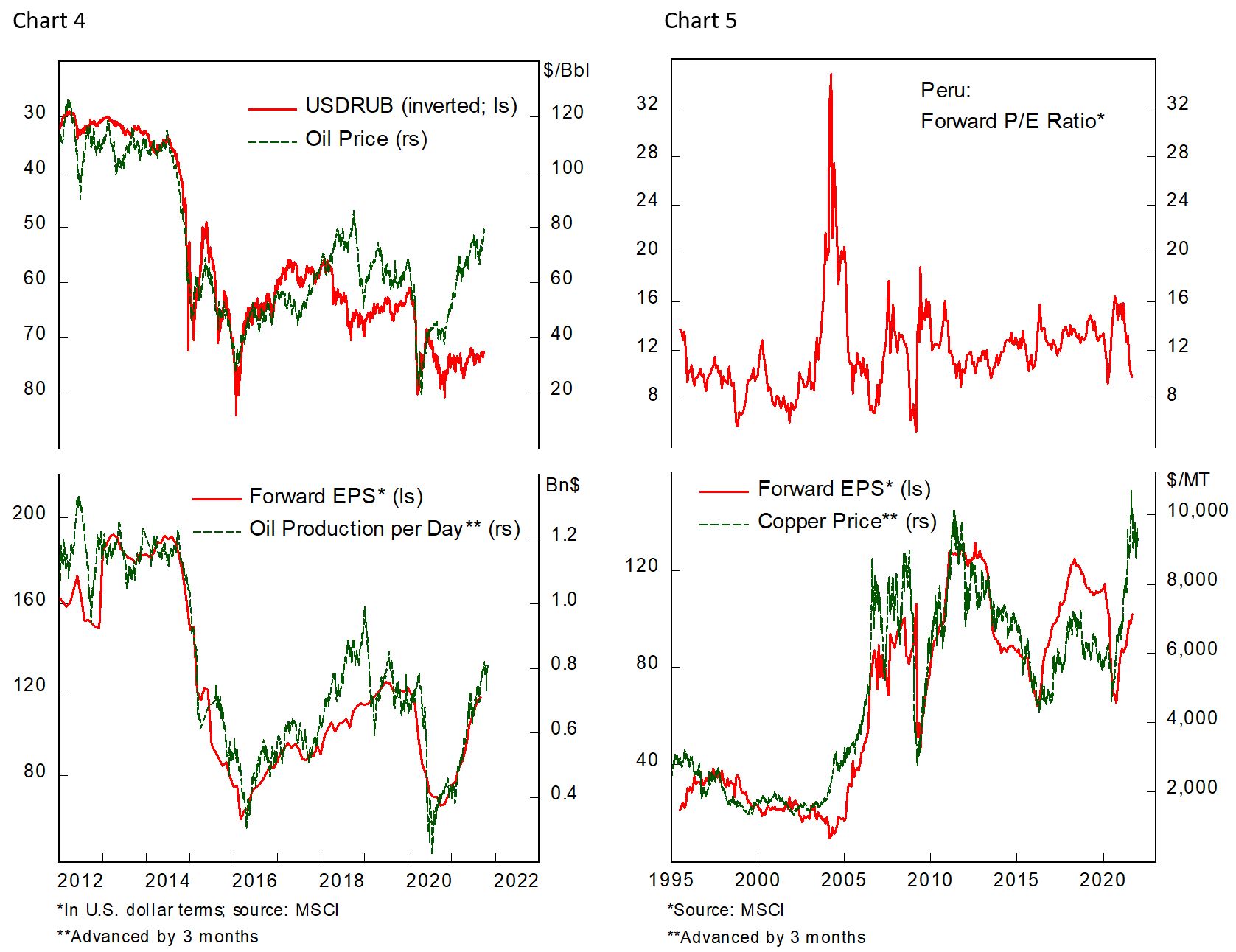

- Chinese growth slowdown bodes poorly for industrial metals demand – copper and steel in particular – while the effect of any policy reflation in the coming months will only be felt with a lag. Brazil, South Africa, Mexico, Chile will suffer most during correction in industrial metal prices due to their high correlation to changes in commodity prices (Chart 2).

- Shortages of goods and high energy prices will drag down manufacturing activities globally, as highlighted by the factory shutdown by auto manufacturers and fertiliser producers. This will compound the problem for Brazil and Turkey, which are already facing renewed inflationary pressure due to rising energy prices. On the positive side, Russia should fare relatively well as it capitalizes the high oil and natural gas prices.

- Most EM countries are still in tightening mode with many policymakers concerned of rising inflationary pressure and impact of Fed tapering, which could be as early as next month. This means stocks multiple should continue to face a headwind as earnings growth moderates (Chart 3). Already, Brazilian earnings growth expectation is turning negative due partly to the correction in iron ore prices.

Recommendation:

Overweight all EM Asia, but underweight India. Table 1 shows EM Asia do well during Chinese easing cycle, but we think Indian stocks outperformance is late. Expensive valuation for Indian equity makes it more vulnerable to correction.

CEE – Remain Overweight. Valuations are cheap and currencies are benefitting from the hawkish monetary policy relative to the Euro. These bourses should outperform during broad correction in EM assets due to its low beta.

Russia – Overweight. Benefits from the high oil and natural gas prices, and better discipline among the OPEC+ cartel means prices could be elevated for longer (Chart 4). Cheap valuation and receding political risk post-election provide a buffer for both stocks and the Ruble.

South Africa, Mexico, Colombia – Neutral. These countries normally underperform during global downturn, but not as poorly as the countries listed as underweight below. Colombia will benefit from high oil prices, but production has been in a structural decline since 2015. Unlike Russia, however, the country’s stock market is much less sensitive to changes in oil price due to its significantly less energy weight in the stock index.

Turkey, Chile, Peru, Brazil – Underweight.

Turkey is facing renewed pressure on the Lira as it cuts policy below inflation rate this month. Although reserves have improved marginally, strength in the dollar will put pressure on the country’s balance of payment. As a large energy importer, Turkish domestic inflation rate likely to spiral further due to rising prices, which will sap consumer and business confidence and potentially translate to policy mistake by the government.

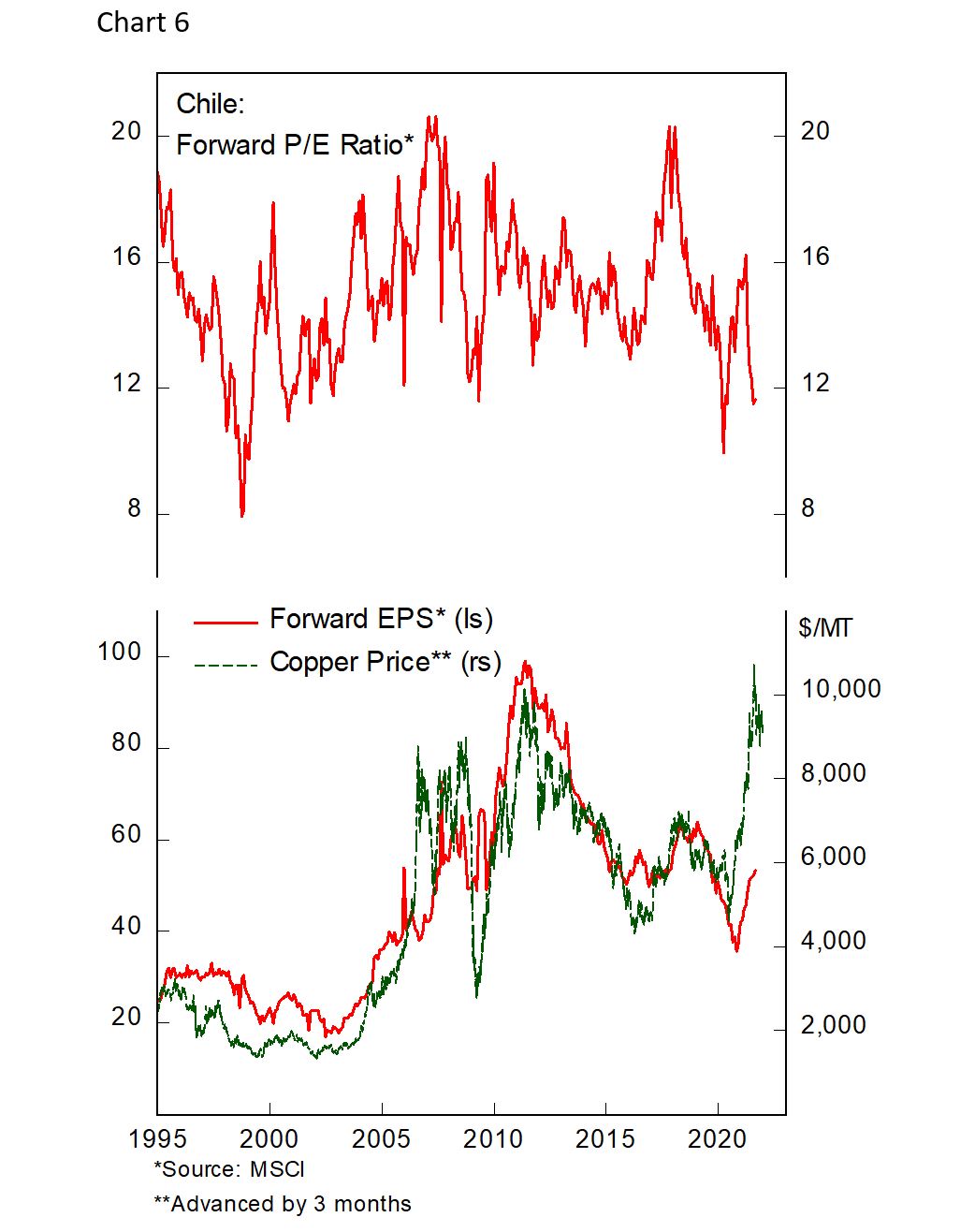

Chile is facing presidential election in November. After failing to hold majority in the constitutional body earlier this year, it remains to be seen whether the incumbent centre-right party – currently polling the second – could stay in power. The stake is high, as a drastic left-turn in executive power risk the country “safe haven” status in Latin America further questioned and potentially trigger another round of capital outflow, similar to what happened earlier this year in Peru. Moreover, despite stocks being cheap compared to its history and the peso undervalued, correction in industrial metal prices will weigh Chilean assets (Chart 5).

Peruvian assets have been derated massively since the winning of the left-wing government. Sentiment remains bearish amid the government warning that miners should pay higher taxes or face nationalization. This revenue would be used to fund new social programs at the expense of miners’ profit, which account for sizeable portion of Peruvian index (Chart 6).

Brazil. No view change since our last piece. Forward earnings estimate is now lower than trailing earnings, highlighting the downside risk to earnings from lower commodity prices.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.