Download PDF:

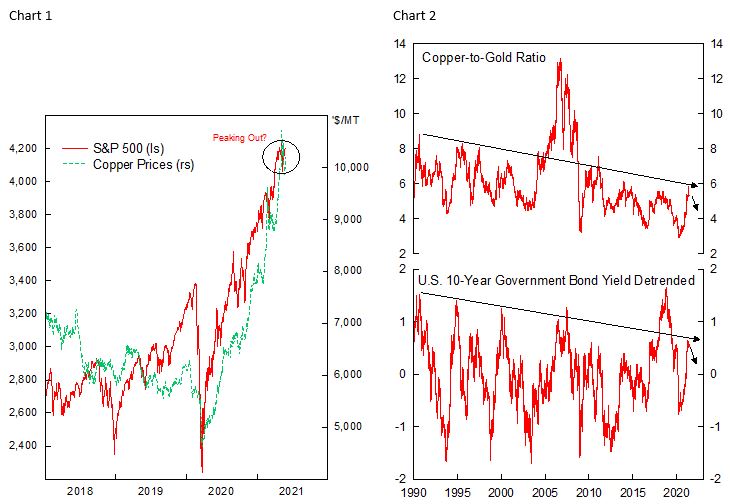

Blow-out number of various economic indicators coming in the past weeks – PMI, retail sales, inflation – suggest that the global cycle is peaking out and the strongest period of growth is in the rear-view mirror. In the short-term, the risk assets rally that began in March 2020 is likely to take a breather or even correct from currently overbought level. S&P 500 and copper prices have refused to go up despite the strong number coming out of U.S. and China in recent days (Chart 1), most likely amid the fear of hawkish policy guidance from the Fed – which some members finally thinking about the timeline for tapering its QE program – and contraction in Chinese credit impulse, which has historically been a precursor to major growth slowdown with significant impact to commodities and global risk assets.

From a cyclical perspective, copper-to-gold ratio and U.S. long term yield – two of our favorite indicators – have been back to the top of its historical trading range (Chart 2), which normally herald a peak in the cycle before reversing downward. In this light, investors should start taking profit on stocks, risky bonds, and commodities and hedge for downside risk. This is especially the case for developed market equities, whose earnings are already above pre-pandemic level and have elevated multiples. Given the explosive rally in the past year amid plenty liquidity and fiscal support, there is plenty of froth in the market – proxied by the meme stocks such as AMC and GME, and also crypto – that could be the source of riot in the market. We are positioned accordingly.

Normally during periods of growth slowdown, both U.S. Treasury yield and the dollar turns lower as expectation for rate hike diminishes and capital flows back into safe-haven currencies such as the dollar. This time around, we believe that 10-year Treasury yield could decline below 1% alongside a weakening dollar (similar to in 2017), for few reasons: 1) the Fed is likely to become even more dovish in a disinflationary environment and push back its tapering agenda to a later date 2) the dollar remains overvalued, 3) its yield advantage is eliminated, 4) widening twin deficit should push it lower., 5) net speculative positioning on the dollar is no longer at the extreme short (Chart 3).

Despite our believe that dollar will continue its decline, we think base metal prices potentially correct significantly from current elevated level (Chart 4) that was driven by strong Chinese imports and temporary supply constraint due to the pandemic, which worsen the already stagnant supply picture. As Chinese marginal demand of commodities plays a huge role in determining global prices, current fiscal and monetary tightening bodes poorly for base metal demand. More importantly, speculative positioning on copper remains stretched and the Chinese authorities have explicitly crack down speculation of metal prices of late, although its direct impact to prices is questionable.

Our cautious view on commodities, however, does not alter our recommendation to overweigh Latam equities, as valuation remain very cheap and earnings have much further upside based on current commodity prices. Recent political shift in the region has led to underperformance of its asset market, but we expect the bull market will continue as major events – Peru`s second round election, Colombian protest, Chile`s November election – passed.

Should our base case scenario play out – weaker dollar and lower yields – the rally in precious metals will continue as lower real yield pushes up its fair value. Chart 5 shows the tight correlation between U.S. Treasury yield rate of change and Chinese credit impulse, which point to roughly 100 bps decline in yields in the coming 12 months. Slowdown amid still high unemployment rate and slack in the labor market should allow the Fed to be patient before raising rates, supporting yields lower.

Meanwhile, as the growth momentum tapers out and worries on inflation abates, breakeven inflation rate could temporarily decline too, mimicking the pathway post-GFC, before turning higher as optimism builds. Taken together, real yield should be much lower twelve months out. We are forecasting a 10-year real yield of -1.7%, which would be consistent with gold price of US$ 2150/Oz (Chart 6).

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.