Download PDF:

In the past three decades the world has seen a dramatic digital transformation happening with the widespread adoption of internet, computers, and smartphones, which only accelerated when lockdown restriction last year pushed our life further into the digital realm. Demands of electronic gadgets, data centers, and networking equipment surged in 2020 as businesses and consumers equipped themselves to adapt to the new reality of working from home. Semiconductors, the most critical component of our electronic devices and hence backbone of all our digital life, saw a renewed increase in demand that outstripped the available supply as the global economy recover strongly, forcing auto to smartphone manufacturers to curtail their production or the planned release of a new model. The situation is particularly acute in the auto sector, where the shortage of lower-end chips has disrupted production globally. Meanwhile, semi supplies are not able to expand quickly, as it takes years and large capital outlay to build a new fab. Taken together, this means the current semi shortage potentially takes few more quarters to be resolved, and its near-term macro implications to manufacturing-heavy countries should not be overlooked.

The Demand and Supply Picture

Semiconductor demand has undergone through a decades-long structural rise in the past few decades, growing at an annualized rate above 5% since the turn of millennium albeit with its own cyclicality (Chart 1). Consumer electronics -such as PC, smartphone, and home devices – account for over two third of semiconductor demand and experienced a surged in sales last year amid the pandemic, while the auto sector took about 12% of the total semi demand annually (Chart 2).

There are few notable observations from the demand side that contribute to the current shortage situation:

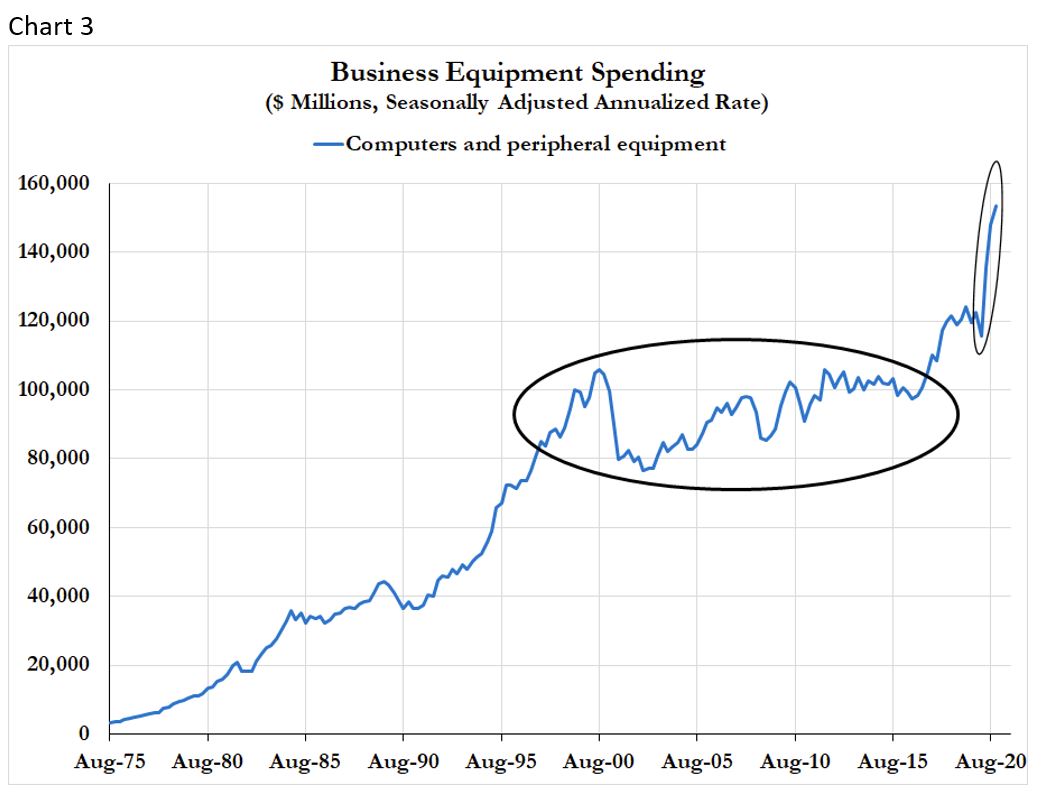

- First, after a sluggish demand between 2000 and 2016, business equipment spending on computers and its accessories has seen broken out to new high with annual spending currently 50% above its 2000-2016 average (Chart 3). Sales for top 5 brands for PC and monitor rose 55% and 8%, respectively in Q1 2021 compared to a year earlier, according to IDC. In addition, the strong demand for computer and monitor is not only concentrated in corporate demand, gaming PCs and monitors are also recording 27% increase in sales last year, benefitting specialized producers such as Nvidia and AMD.

- Second, the adoption of consumer electronics is also broadening with the advancement of “smart” wearable and home devices, on top of the robust demand for smartphones. Sales of smart home devices recorded a 4.5% rise for 2020 and continued to grow 12%yoy in Q1 this year, while shipments of wearable devices increase 28%yoy growth last year. Although roughly about half of households in the developing world have already had at least one smart home device, penetration in emerging countries is still low and some are still in a single digit. Meanwhile, sales of top 5 smartphone brands are still recording a strong 26%yoy growth in the first quarter of the year. All this point to a continued

- Third, innovation in the auto sector results in various features being added to a car, such as sensor, GPS, smartphone connectivity, etc., all of which requires specialized chips to manufacture. The shortage in past few quarters in the auto industry is mainly due to producers cutting their orders for parts last year as they were expecting vehicle sales to be sluggish amid the pandemic. As a result, semi producers shift their production to accommodate the strong demand from buyers in the consumer electronic sector. However, stronger than expected recovery in the developed world has translated to vehicle demand rebounding strongly, which caught auto manufacturers short of chips component for its car. This has become a strain for the auto industry and forced them to slow production or even close their factory (Chart 4), despite most of their demand being concentrated in lower-tech chips, as semi producers are already operating at full capacity.

- Finally, the current shortage is worse than previous episodes due to the global adoption of lean inventory practice and “just in time” manufacturing system in the past decade, prioritizing efficiency over resilience of its supply chain. Although this means that producers are able to better tailor its production to market demand and reduce inventory, it also means that stronger than expected demand could translate to a shortage in the medium term, especially when the spare capacity of its suppliers is already low (Chart 5).

Amid the strong demand seen in past year, semi supplies from top producers – TSMC, Samsung, and Intel – are not able to catch up just yet. As a capital-intensive business that is facing high demand volatility, semi producers are not willing to expand capacity unless demand is forecasted to be strong beyond a 5-year horizon, and the supply glut in 2018 has stoked this concern further. Meanwhile, building a new semiconductor fab takes years and sizeable capital spending, which means that semiconductor prices are widely volatile as any supply shortage is unlikely to be solved quickly (Chart 6). Pat Gelsinger, the new CEO of Intel, forecast that chip shortage in the auto industry could take at least 2 years to ease.

The tit-for-tat ban during Trump’s administration also plays a role in worsening the supply picture, as restrictions on semi sales to Chinese communication firms – the like of Huawei and ZTE – result in stockpiling of chips by Chinese producers, while U.S. were also cut off from lower-tech chips made by SMIC due to the Federal ban on the firm.

Another important risk factor for semi supplies is the current drought in Taiwan that potentially hamper the country’s chip production amid falling water reservoirs in several factories. The Ministry of Economic Affairs earlier in April implemented rationing of water supply, requiring companies to reduce water usage by 15%. Semi manufacturing is a water intensive process – TSMC factory in Taichung consumes 200.000 tons of water per day – and the country accounts for 60% of global foundry revenue, making the current drought, if prolonged, potentially derail global electronics manufacturing (Chart 7).

When Will The Shortage Ease?

Assessing and quantifying the demand for semi in real time is difficult, as consumer spending on electronic devices vary with the economic cycle and release of new products. However, demand in the near term likely already peaked for two reasons. First, broadening vaccination campaign should allow workers to come back to office and reverse last year’s trend where office workers are rushing to upgrade their PC and buy a second monitor for home use. Moreover, businesses and consumers that need to upgrade or add PC and other electronic devices should have done so last year when lockdown restriction was at its tightest, hence demand should revert to normal this year. If semi demand from consumer electronics ease, then production could be shifted to meet the need of the auto sector and allow vehicle production to rebound in the coming months.

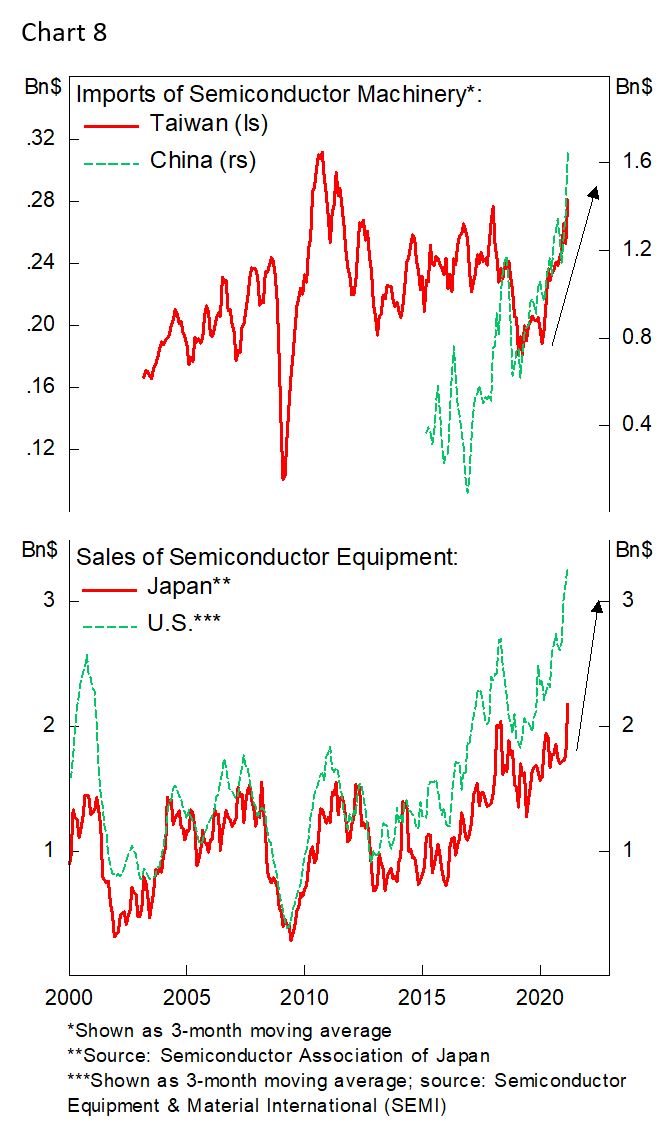

For the longer-term supply outlook, major semi producers this year announced significant increase of their capital expenditure to expand capacity and further develop the 5 and 3 nm technology into broader application. Taiwanese and Chinese imports of semiconductor machinery are already seeing a sharp rise in past months, mirrored by the rising exports of such machinery from U.S. and Japan (Chart 8). All this should translate to a rise in supply in the coming 2-3 years.

Market Implications

- The chip shortage bodes poorly for car manufacturers and the countries with large auto manufacturing base, such as Mexico, Germany, and the Eastern European countries. This potentially result in both revenue and earnings undershooting consensus and weigh the trade balance of these countries. Used car prices may stay elevated amid tight supply of new vehicles.

- Consumer electronics could be the next in line, with Samsung postponing updates to its flagship model this year.

- Slowdown in medical devices production, the rollout of 5G infrastructure

- Increase in pricing power of semi firms. TSMC is holding instead of cutting prices of its older generation chips.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.