Downlaod PDF:

Earlier this week we published our long-term global themes, outlining the possibility of stronger inflationary pressure and the danger it poses to corporate sector. Meanwhile, we also publish our next year outlook last month, where we argue that Chinese growth will rebound strongly and liquidity will remain plenty, buoying asset prices. With our recommendation to stay bullish on the market and our country pick weighing heavily on commodity indexes, our portfolio has fared well this year, with our leveraged position on Mexico, Chile, and Turkey returning double-digit return. Meanwhile, our effort to hedge the portfolio beta through shorting U.S. equity has so far proven to be costly, with the U.S. markets having its best month in November.

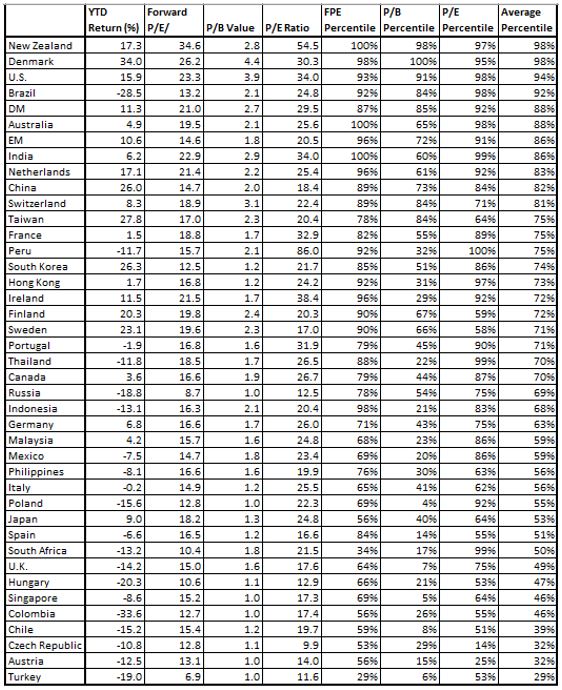

However, we are sticking to our view that a correction for the U.S. market is overdue (at the time of the writing, S&P 500 is trading at 3661 level). There are signs of exhaustion on the bullish trend, confirmed by the market slight pullback after the announcement of a bipartisan proposal close to $1 Tn stimulus by U.S. senators. In the worst day of the market rout in March, we monitored percentile of global market equity valuation that proved to be useful in assessing how much more the downturn could go. With the market rallying sharply since, we are repeating the exercise to see how dear global equity valuation has become, summarized in the table below. Close to 70% of the market is trading above its 50th percentile, driven by the forceful fiscal, monetary support globally, and a weaker dollar. This is the reason we are paring back our position on our core position and wait to see a better market entry point, especially for Mexico that has seen over 200% gain since initiation early this year.

We remain bullish and dismayed by the resistance for Chilean equity and currency to go upward despite the surge in copper price, creating a further divergence between the two that has historically been very well correlated. The referendum next year and poor handling of the pandemic might have so far deterred portfolio inflow, but we think the country’s equity could easily double in the next year should current trend persist. More recently we also reinitiated our long position on Turkish equity, after the government and central bank revert to more conventional policies in rate setting and tempering its dispute with EU. Turkish equity and the Lira are among the cheapest in EM, heavily under-owned, and could be the largest winner from global reflation effort. However, risk remain related to its poorly inadequate international reserve assets.

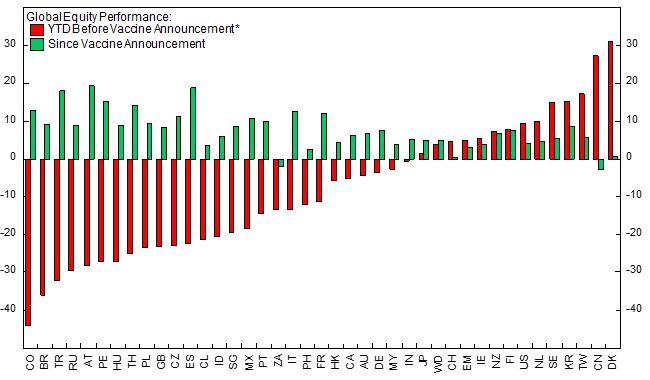

On developed country assets we are bullish on Japanese and British equity, mainly due to valuation and cyclical reason, but we think the return/risk is better among EM countries mentioned above. British equity has been battered badly until last month after the vaccine announcement, which has spurred rotation to a more commodity-heavy and cyclical sector/countries.

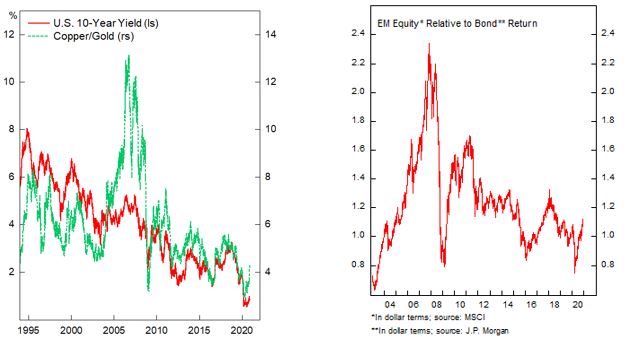

We are reiterating our view that the outlook of risk assets going into the new year remain very strong, as copper/gold ratio and U.S. long-term yield continue to rise, but a pullback is overdue amid overbought condition in commodity and equity. Although many pundits argue on the lack of catalyst for a correction, we are afraid we are entering a “Minsky” moment as of this writing, where call/put ratio is at all time high and complacency could be seen in almost every risk assets. In addition, mania plays such as Bitcoin and EV producers are rampant and retail participation is high. Investors should be cautious on averaging up, and we prefer to stay on the sideline with our current position to wait for a better entry.

The often-cited reason behind the massive rally in growth stocks is that declining yields have non-linearly increase the present value of future cash flows of these stocks and the justify current price level. But investor needs to be warried that inflationary pressure could come back more rapid than is expected, as we argued in our 2021-2030 global themes publication early this week. Should this scenario happen in the next 2-3 years, which we put a 60% odd, long-term bond yields would back up and growth stocks should underperform. Overall, this scenario would trigger selloff in risk market. It is ironic that global central banks have been trying to push inflation higher, but when it is indeed the case, it is doubtful that the market would response positively.

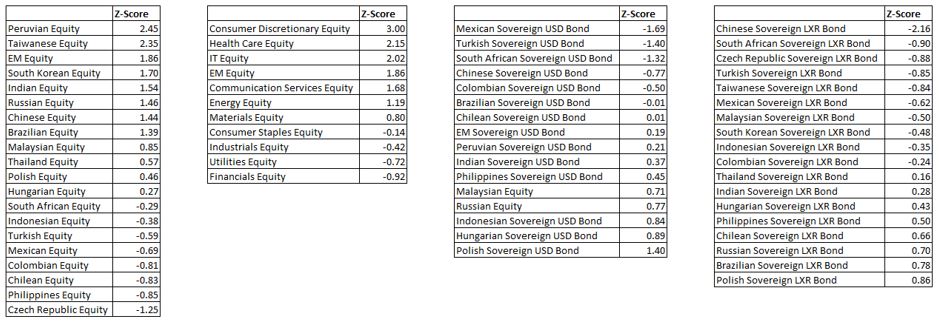

On the last note for this month, we are monitoring the Z-score (or deviation) of EM equity valuation, USD-denominated bond, and LXR-denominated bonds, and rank them from the least attractive (top) to the most attractive (bottom) from a historical perspective. This is not meant as a recommendation, but rather to see which asset market has performed best/worst relative to its 10-year period average.

Bottom line: remain bullish on risk assets but preserve cash position and wait for a better entry point to further accumulate risks. Commodity plays should outperform its growth counterpart, and U.S. equity should underperform going forward.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.