Download PDF:

Last month, we outlined our outlook for the year ahead, where Chinese growth will continue to rebound strongly and global liquidity remain plenty. This month, we are taking six themes for the coming decade, with the focus on inflation, savings-investment dynamic, and transition to renewable energy. I hope you enjoy the read.

Theme #1: Decline in Global Savings Rate and Gradual Rise in Inflation

For the past four decades, globalisation and increase in working-age population have been a tailwind to global growth, increasing the world’s productive capacity that led to the trend of declining inflationary pressure (Chart 1). This increase in global labor pool translates to a decline in bargaining power for labor, as companies are arbitraging labor cost between countries (China) in deciding where to locate their manufacturing base, a loss to the unskilled and semi-skilled labor in developed countries (Chart 2). In the coming decade(s), however, these two drivers could reverse. First, globalisation has arguably peaked in 2007 before the financial crisis and 2018 U.S.-China trade war has shown the danger of being too reliant on overseas supply. Even if globalisation is not dead, it has at least stagnated. Second, the baby boomers that had entered the labor force in the 1970s are now gradually retiring, reversing the trend in global dependency ratio and hence savings rate, which tend to peak just before retirement.

The decline in savings rate will be a global phenomenon, but the largest driver will come from the fall in China’s savings rate, whose old-age will exceed its working-age population by mid-century (Chart 3). Similar trend could be observed in much of the developed world, with other East Asian countries, Western Europe, and even North America leading the way. If globalisation and decline in dependency ratio drove inflation lower in the past 40 years, then a reversal of these trend should at least bring inflation gradually higher in the coming decades (Chart 4). Gold tend to thrive in this environment, where the current situation is still deflationary, policy is loose, but inflation scare is high.

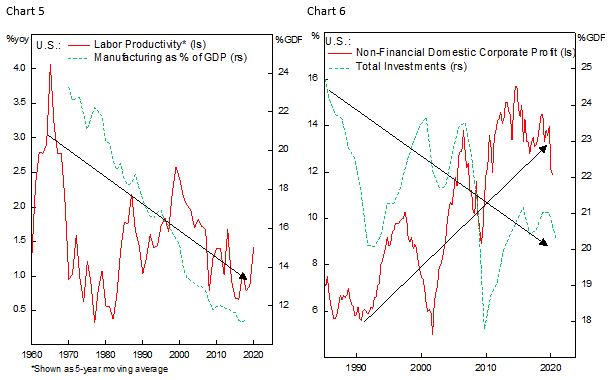

Theme #2: Stagnating Productivity Growth and The Phillips Curve

As developed economies become richer, higher share of its economy is taken up by the service sector, where productivity improvement is harder to realize than in the manufacturing sector (Chart 5), i.e. you could not improve the workflow of a hairdresser or equip him with fancier tools to enable him cutting his customer’s hair faster. This means that productivity growth will become increasingly anemic as a country grow rich. However, the decline in supply of labor is likely to push the corporate sector to increase its capital/labor ratio and improve productivity, meaning that investment should remain stable amid the decline in savings rate, reducing the global savings imbalance (Chart 6). Japan is a good example of how a country that lose 1% of its labor force manage to increase output per capita by 1% annually through implementation of technological advances.

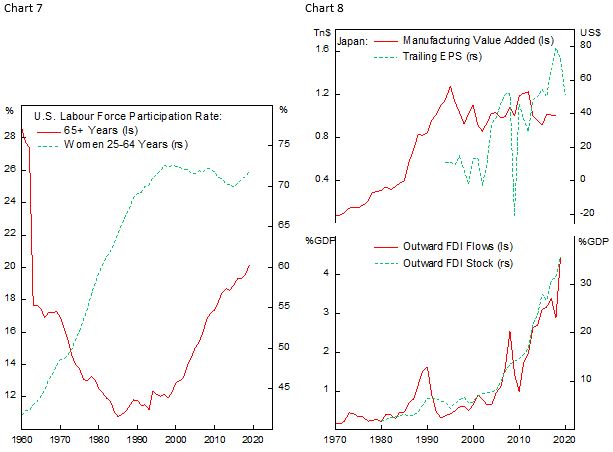

The discussion on labor supply-demand inevitably makes investor to wonder whether wages growth will finally rise after years of sluggish growth. In hindsight, there are several factors that resulted in the flattening of the Phillips curve. First, although some may find it dubious, better monetary policy arguably resulted in inflation becoming less sensitive of unemployment, as the central banks were quick to tame expectation or fear of inflationary pressure itself by raising rate, i.e. 2015 Fed rate hike when core inflation is below 2% target, preventing inflation to materialize. Second, the increase in women participation rate until the turn of the millennium and doubling of the share of old people who decide to stay in labor in the past two decades have both increase the supply of worker and acts as a valve to satisfy incremental labor demand, depressing u* (Chart 7). Third, with labor cost in the manufacturing sector arbitraged away in globalization, it is difficult for the wage-inflation spiral to occur. For example, Japan did not experience accelerating wage growth despite its low unemployment rate because of the country’s large outbound FDI allow it to benefit from cheap overseas labor in neighboring countries (Chart 8). The bottom line is that with longer life expectancy people are likely to be in the labor force for longer, while global labor cost arbitrage continues and shift towards low-cost producers, which point to continuation of weak wage growth.

Theme #3: Corporate Sector Deleveraging

Low interest rate and easy monetary policy pursued by global central banks in the past decade has pushed corporate leverage to record high relative to the economy without increasing its interest burden, a tailwind to corporate profits. However, if inflation indeed comes back and interest rate is pushed higher, the corporate sector will be forced to deleverage, with many pushed to insolvency. For example, a 2.5% increase in the cost of borrowing, i.e. 10-year BBB-rated corporate yield from 2.5% to 5%, would significantly reduce the group’s interest coverage ratio from 3 times to 1.5 times. The situation would be much worse for zombie firms, which in the past decade have survived mainly due to easy monetary policy (Chart 9). There are three ways for the sovereign/corporate sector to prevent this balance sheet recession: 1. Cut spending and save, 2. Inflate the debt away, 3. Inflate asset prices.

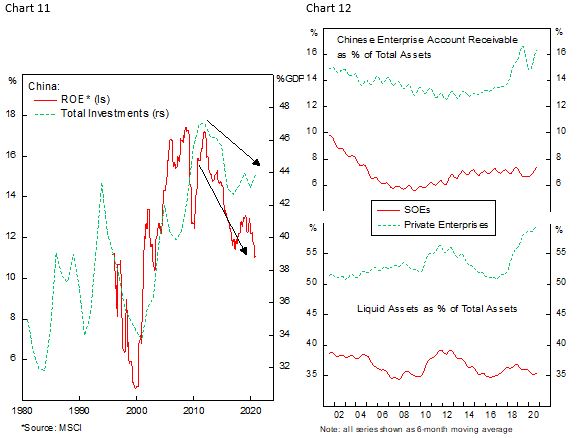

The situation is worse in China, where real growth rate likely continues to downshift as the country’s investment and savings rate decline (Chart 10). Already there is a visible downshift in Chinese corporate profitability since the GFC, which will drag investment rate further down (Chart 11). The saving grace is that capital control and high domestic savings have so far prevented liquidity crisis in Chinese banks and corporate sector. For long, credits have been priced too cheaply and misallocated as creditors assume loans to SOE would always be backed by the government. This misallocation of resources results in excess capacity, falling prices and margin, and difficulty in repaying their debt for Chinese SOEs. This also implies that Chinese banks’ health is likely overstated, with NPL number masked by bad loans that are repurchased from shadow intermediaries and evergreening of delinquent loans. This starve the more productive private sector from credit and slows real growth. Since 2017, there are signs that the private sector is having difficulty to collect payments from Chinese SOEs, as proxied by growing account receivable that is not seen among SOEs (Chart 12).

Theme #4: China as Global Consumer

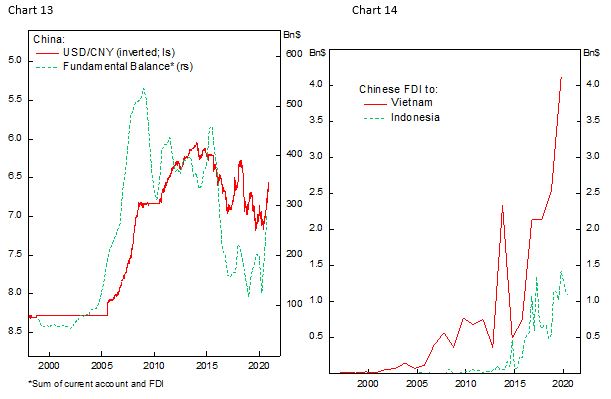

With savings and investment rate declining and the Chinese government push to stimulate domestic consumption, China is likely to increasingly turn from global producer into global consumer. The country’s current account and trade balance most likely will turn deficit this decade, putting a lid on CNY’s appreciation (Chart 13). This shift benefits countries with lower cost of production, especially in the South East Asia. Already Vietnam and Indonesia experienced FDI surge from China this decade, these are two fast-growing countries in ASEAN with cheap labor cost, high savings rate and rapid pace of capital accumulation, all of which are conducive for offshoring of manufacturing base (Chart 14).

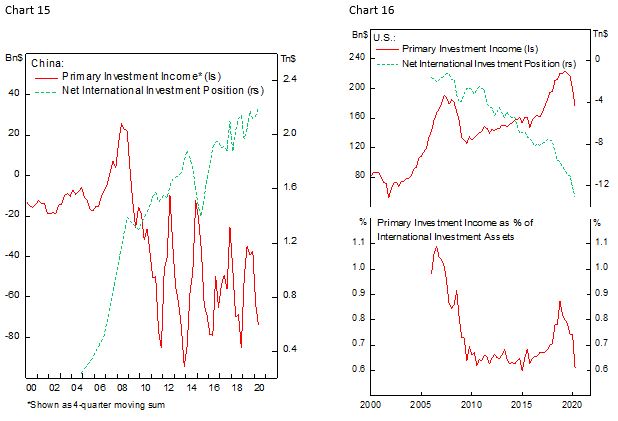

To finance its current account, China will have to liberalize its capital account control further and attract foreign capital. Although China has a massive $2.2 Tn Net International Investment Position, its investment income account is negative due to a large portion of its foreign assets concentrated in safe and low-yielding U.S. government bond (Chart 15). This contrasts with U.S., whose NIIP stands at minus $13 Tn but has a positive investment income flow (Chart 16).

Theme #5: Fiscal Policy, Bond Yields, and Global Liquidity

In the past decade we have seen private sector savings exceed government dissaving by the tally of several hundreds billion and more recently exceeding a trillion (Chart 17). This chronic excess savings in the economy has pushed term premium lower in the past four decades and brought down long-term government yield as well, with the Fed QE unable to boost term premium sustainably higher (Chart 18-20).

In the first theme, it was argued that private savings rate would come down in the coming decades, resulting from deterioration in dependency ratio. Meanwhile, government deficit is unlikely to decline enough to offset the decrease in private sector savings due to the burden from aging-related expenditure, including health care cost and pension. It will potentially shift policy further to the left and increase government spending, bolstering inflationary pressure upward. This could mean that long-term yield will face an upward pressure, first from the higher inflation rate, and second from increase in real interest rate and term premium. At some point, this increase in dollar borrowing cost will pressure EM sovereigns and corporates that have been borrowing heavily in foreign currency.

In the short-term, liquidity injection and easy monetary policies mean equity valuation multiples should remain elevated and junk corporates yield depressed. However, the peak of policy stimulus is likely behind us and will reverse going forward, bringing equity multiplier lower and junk yields higher (Chart 21). Only then, after the tide of liquidity revert, the market would know who has been swimming naked.

Theme #6: EV and Green Energy Revolution.

Increasing number of countries are pledging to be reduce its emission1 significantly by the middle of this century, with some targeting to become carbon neutral. Chart 22 shows EIA projection that demand for energy will increasingly be met by renewable sources, such as hydropower, wind, and solar. The world transition to green energy requires significantly more metals, especially copper, to produce electricity. Wind turbine and solar panel require 4-6 times the amount of copper to produce one MW of electricity, potentially adding 5-6 Mn Tonnes of copper demand up to 2050 (Table 1 and Chart 23).

But more exciting is the rise in demand from electrification of vehicles. An internal combustion engine car requires on average 23 Kg of copper, whereas EV require 3-4 times that amount. With a conservative projection that EV sales are expected to reach 11 Mn units (9% of total vehicle production) by 2035, it potentially adds more than 1 Mn Tonnes copper demand annually, a number that is set to increase over time (Table 1).

Tallying the number together from renewable energy and EV alone, net copper demand will continue to increase by 1-2 Mn Tonnes annually, or 5-10% of current production figure (Chart 24). This bodes well for countries with large copper reserves and are able to increase their production, such as Chile and Peru, which produce over 40% of world’s copper supply annually. The high importance of these two countries, alongside Congo, to satisfy green energy infrastructure demand could mean that they will become the geopolitical battleground in the coming decades, similar to Middle Eastern countries in the 1970s.

The loser from this “green revolution” will be oil-exporter countries (Saudi Arabia, other GCC, Norway, Russia), which all have seen their current account deteriorates since the oil shock of 2015 (Chart 25). These countries fiscal and growth are highly dependent on maintaining high oil prices, but they are also pressured to cheat and pump more oil to cover their deficit. With plenty of spare capacity that could be brought alive, it is unlikely for oil price to sustainably rise above $50/Bbl. It is also interesting to see how long Gulf countries such as Saudi and Kuwait could maintain their peg against the dollar, as their currencies are very expensive in real terms, unlike its floating counterpart (Chart 26).

1https://www.carbonbrief.org/paris-2015-tracking-country-climate-pledges

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.