Download PDF:

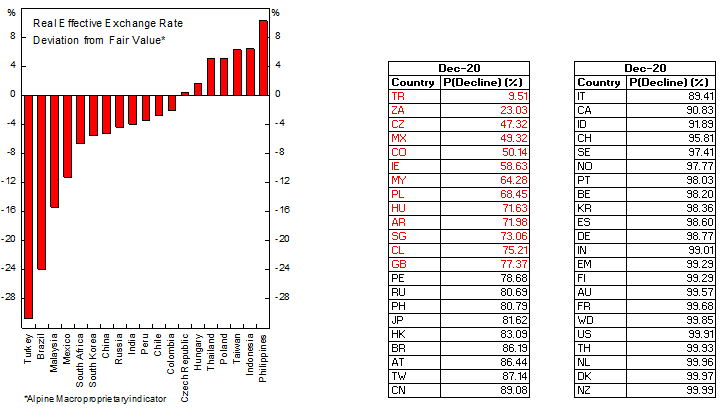

With the year almost ending and asset prices have rebounded strongly, we are becoming increasingly cautious on adding position to our core portfolio holdings and prefer to stay on the sideline until the next correction, at the risk of missing further upside moves. Technical and valuation point to an overbought and overvalued U.S. market alongside a very concentrated long position on commodity, especially copper. As this month’s piece outlined, we remain structurally bullish on select countries, such as Turkey, Chile, and Mexico and hold concentrated position on these countries’ equity unhedged.

Our recommendation to long copper from earlier this year to benefit from the cyclical forces has been well rewarded, but now we are net short on copper and are looking for a better entry point and moderation of speculative position before going net long again.

On equity, we believe there are still juice left on Mexican stocks and increase our core holding of Turkish and Chilean stocks, all currency unhedged. All these three countries stand to benefit the most from a global growth recovery and both their currency and equity are cheap.

Lastly, we are shunning U.S. high yield bonds in favor of EM sovereign dollar bonds, but maintain a bullish stance on equity vs bond.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.