Download PDF:

South African government released its medium-term budget plan late last October, highlighting the steps it will take to bring the country’s spiraling public debt under control. South African assets had been bombed out this year, which offers attractive investment opportunities from a tactical point of view. However, structural outlook remains bleak and the country require a comprehensive reform to attract foreign investments and bolster its growth profile. In the medium-term, investors should pay attention to the deterioration in the country’s fiscal situation, which will be the pressure point for the country’s asset market.

The Good…

- South Africa has managed relatively well against the pandemic compared to other EM countries, in terms of both health and economic damage. The government was fast in imposing a strict lockdown restriction in March when there were still few Covid-19 infection cases and so far, a second wave of the virus has been avoided (Chart 1). The ability to suppress the virus from spreading out of control has allowed economic activity to recover faster compared to other countries (Chart 2) and the government’s R500 billion (10% of GDP) fiscal relief package announced in April has helped to support household income during the lockdown and in providing health care services related to the pandemic (Chart 3).

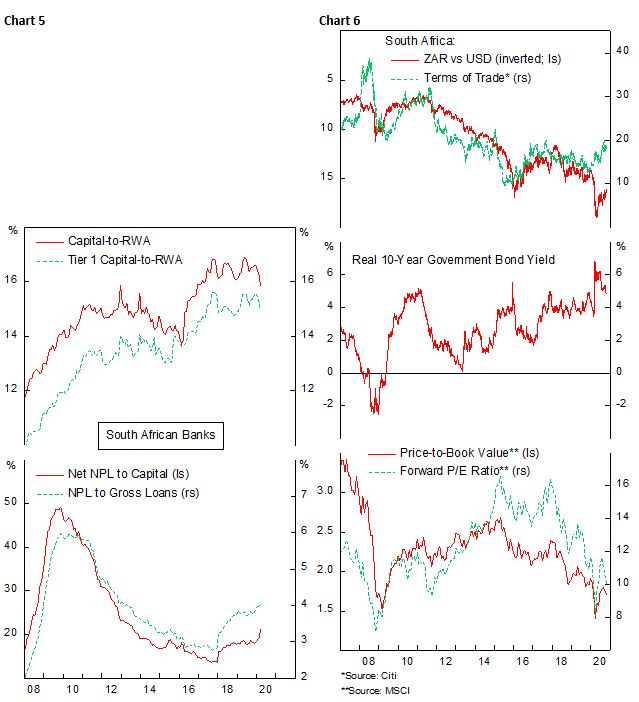

- An immediate Balance of Payment or banking crisis is unlikely. South African forex reserves are more than adequate to cover the country’s short-term external financing needs (Chart 4), the country’s banking sector has built ample capital buffer after the financial crisis, and asset quality is higher compared to 2009. During the peak of GFC, bad loans are equivalent to 50% of banking capital; the number currently stands at only 20% (Chart 5).

- Investors have dumped South African assets indiscriminately during the market rout this year – foreign ownership of South African government bonds declined from 37% to 28% – which has significantly improved risk/return profile (Chart 6). Our model estimate shows that the ZAR is about 15% undervalued, driven by the improvement in the country’s terms of trade, while the country’s real bond yield is among the highest across EM universe amid a low inflationary backdrop. Currently, equity valuation is near its historical low level and earnings are making a bottom. From a historical point of view, the downside risk of investing in South African assets are limited, but investors should keep in mind few caveats.

…The Bad…

- The deterioration in South African fiscal situation is a chronic problem and the country has been having difficulty to reign its growing public debt since the GFC, a problem compounded by lower structural growth rate and inflation (Chart 7 and 8). The pandemic has worsened the fiscal situation further, with the government currently running a 10% of GDP deficit so far this fiscal year out of a projection of 15.7% of GDP deficit. According to the medium-term budget plan, South African government is set to undergo a fiscal tightening program, with the aim of running a primary surplus and stabilization of public debt level at over 95% of GDP by 2025/2026 fiscal year (Chart 9) through a freeze in public sector wages that has grew rapidly in recent years (Chart 10).

- Under President Ramaphosa term since 2018, South African government has pushed for an additional investment spending – without cutting other expenses – that has widened the country’s fiscal deficit even prior to the pandemic. Education, health care, and investment spending are all set to rise, both in nominal terms and as a percentage of GDP (Chart 11). However, as Chart 12 shows, 70% of the fiscal revenue has and will be spent on compensation, household transfer, and debt-service cost, leaving little for discretionary spending that could be directed toward productivity-enhancing investments. Moreover, the government is still focusing on helping its ailing SOEs, highlighted by its recent decision to allocate R10.5 billion (0.2% of GDP) to bail out South African Airways, putting into question whether the government is serious in doing public sector reform. In a more positive light, the government is opening the way to allow municipalities to buy electricity from other sources and the procurement of 12.000 MW new capacity from independent power producers, while at the same time rehauling Eskom, to address the country’s electricity shortage (Chart 13).

- The bad news is that even assuming that the government is able to fulfill the tall order of reigning the growth of public sector wages and avoid another growth slump, debt service cost is still expected to rise in the coming years. South African fiscal improvement stopped under the presidency of Jacob Zuma (2009-2018), whose administration is characterized by mass corruptions among politicians, the plundering of the state’s wealth, and a reversal of the country’s borrowing cost. To prevent South Africa current situation into a debt crisis, it is urgent for public spending to be curbed significantly and reoriented towards growth-enhancing investments. With the current budget plan, where non-discretionary spending is still taking the majority of fiscal revenue and debt-service cost is set to rise further, the prospect of South African government is poor and bond yield should face a building upward pressure (Chart 14).

…And The Ugly

- Following a rapid development between 1950 and 1980, South African growth then drift significantly lower in the eighties as anti-apartheid movement intensified and increasingly supported by international pressure for South African government to end the system, resulting in a period of social upheaval nationally and a decline in the country’s saving and investment (Chart 15). It was only until the early 1990s when Mandela was released from prison and apartheid legislation was repealed that South African economy continue its growth trajectory, but domestic savings rate never rebounded during those years to the level seen in the eighties. In fact, it has slowly drifted lower in the past thirty years and is currently among the lowest across EM, resulting in a much slower of capital stock accumulation and productivity growth. The country did enjoy a successive period of rapid growth in the 2000s up to the GFC, but since then the country’s capital stock has stagnated while productivity has been trending lower (Chart 16), all of which bode poorly for the country’s growth outlook.

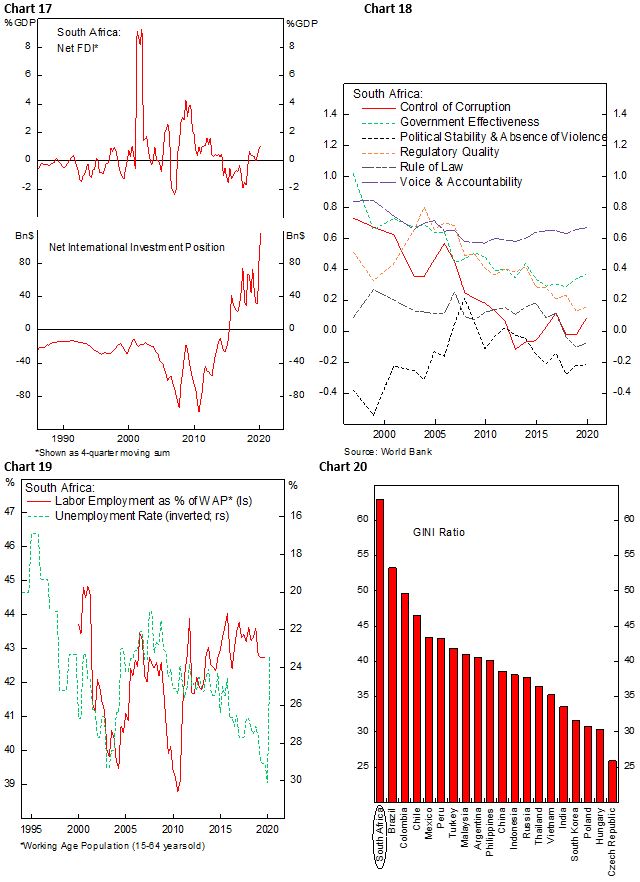

- The low domestic savings rate means that South Africa is dependent on foreign investments to build their capital stock. Foreign Direct Investment was high in the 2000s leading up to the GFC but since then has reversed as the country’s macro profile deteriorates during Zuma’s presidency. A more dramatic picture is South African positive Net International Investment Position (NIIP) – meaning that South African investors own more investment abroad compared to foreigners in South African assets, an abnormality for EM countries – which has continued to surge this year (Chart 17). This highlights the unfavorable business climate and lack of attractive investment opportunity in South African domestic market. Indeed, various governance indicators for South Africa have worsened significantly in the past decade, pressuring the government to conduct a comprehensive structural reform to attract badly needed foreign investment to the country (Chart 18).

- Lastly, the slow economic growth has created to few jobs for South African, whose population has doubled in the past three decades, resulting in a large portion of its working-age population unemployed. The official statistic shows 30% unemployment rate early this year, but our estimate of the true figure is closer to 55%, with the difference explained by exclusion of discouraged workers (Chart 19). Joblessness among half of working-age adults – especially among the younger population – is worrying from both economic and political point of view. Adding to the problem, South Africa is also one of the most inequal country in the wonrld (Chart 20), a heritage from its apartheid era, which fuel the feeling of maltreatment among its majority of black population. This combination of slow economic growth, high unemployment rate, and rampant inequality is a perfect recipe for social upheaval should the government fail to get the country of the vicious cycle of savings and growth and create a fair and balanced economic growth.

Bottom line: less risk-averse investors should tactically long ZAR against the dollar in anticipation of improving global growth outlook and further weakness of the dollar. As a high beta EM currency, the Rand will benefit the most from a synchronized global growth in 2021. Meanwhile, stay neutral on South African local-currency bonds despite the high real yield, as the fiscal outlook is poor, and uncertainty remains on whether the government will able to reign its spending. We upgrade our recommendations for South African equities to Slightly Overweight.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.