Download PDF:

This year, the coronavirus and lockdown restriction enforced globally have driven the financial market at large, far outweighing the impacts from U.S.-China escalating geopolitical rivalry, war in the Caucasus, and U.S. Presidential Election. These themes are likely to continue in 2021 and already some of its effects lingered permanently, as discussed below.

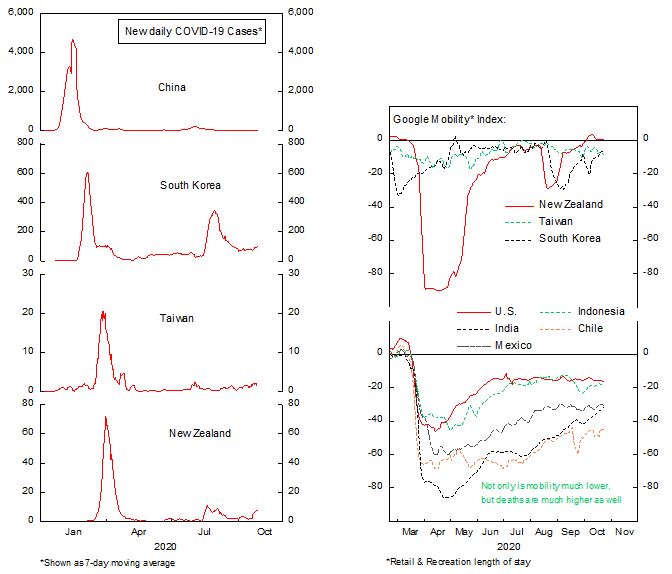

First on controlling COVID infections, we have taken a more pessimistic view. Both developed and emerging countries’ government proved to be inept in keeping the virus in check by tracing infection cases early when the number of cases was still low, with the exception of China, South Korea, Taiwan, and New Zealand. Now that the number of daily new cases are in thousands, or even tens of thousands in the case of U.S., India, and European countries, it is nearly impossible to control the spread without a mass lockdown, which is economically undesirable.

We think that another nationwide lockdown is unlikely, given the increasing resistance of the public due to lockdown fatigue, but rising infection cases do change consumer behaviors and is a negative to economic activities. For example, living in Montreal, some of my friends have completely forgo dining in a restaurant since April, even when the number of new daily cases was low in the Summer for fear of contracting the disease. This year, I have only got two haircuts instead of the average five by this time. These bode poorly for workers and businesses providing such services. Even with the availability of food delivery applications, spending on restaurant and bar is far below pre-pandemic level.

As someone who has a short stint as a medical doctor, and now an investment strategist, I have to say that the situation is not encouraging, both from healthcare and economic perspective. Most governments have wasted the efforts made during the first lockdown – which did suppress the number of infection cases – by failing to trace the leftover cases and bring the reproduction number (R) below 1. Without a coherent strategy and strict tracing policy, both the people and economy are at the mercy of the virus spread.

Rationally speaking, countries with still surging cases should implement another 14-days lockdown but this time do the tracing properly to avoid another spiral in new cases when the lockdown is lifted. However, I am not confident that this is politically palatable, which leave us living under the current environment until a herd-immunity is achieved, either through vaccine or sufficient antibody level in the population. The bottom line is that the ebb and flow of COVID-19 cases will continue to drive economic growth in each country in 2021, and investors might have been too optimistic in projecting strong GDP growth next year. The 80% economy is here for longer.

Chinese Growth, Chip Wars and Taiwan

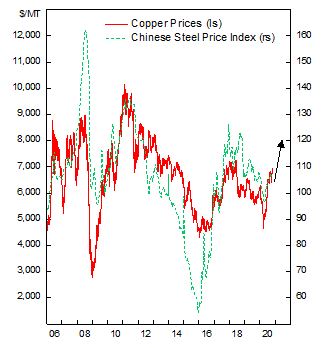

Chinese economy has rebounded strongly in the past two quarters and should further strengthen from rising domestic consumption. Credit growth remains strong and fiscal impulse will stay positive in the short-term. Policymakers’ focus on pushing domestic consumption amid weak exports in the long run will accelerate the deterioration in the country’s current account, driven by higher imports of goods and services. As a result, real GDP growth should fall but is becoming more sustainable. In the short-term, government-led investment push will dominate the recovery, driving commodity prices higher. Copper, iron ore, and steel price are likely to resume upwards, at least until the end of Q1 next year. Until then, Chinese growth and policy are unlikely to provide unexpected shock to the financial market.

Geopolitically, U.S.-China rivalry under a Biden presidency should be less intense and chaotic relative to Trump’s. Restrictions on Chinese imports of chips could be eased, but human rights concern on Xinjiang issue might escalate. Biden is likely to work with the Western consensus in mind and coordinate with allies to counter China’s growing power. On top of these, the Taiwan issue will remain on the front page, as China could not afford to lose its territorial integrity (and face) while U.S. is putting both feet in the water as part of its “Pivot to Asia” strategy. Already, this week U.S. approves $2.37 billion weapon sales to Taiwan.

U.S. Post-Election Bull Market and Growing Corporate Risk Profile

The hope for another fiscal stimulus before the election is dead, but another round of stimulus is coming regardless of the election winner, with the Democrats having larger package and greater state support. Market is likely to become euphoric in the short-term, as Biden’s presidency will unleash an infrastructure building across the country and accelerate the energy transition toward clean energy, which help accelerate economic growth. Our bet is that long-term yield will be pressured upwards, as government fiscal deficit could be larger than private sector savings, and it would be difficult for government to rein in public spending.

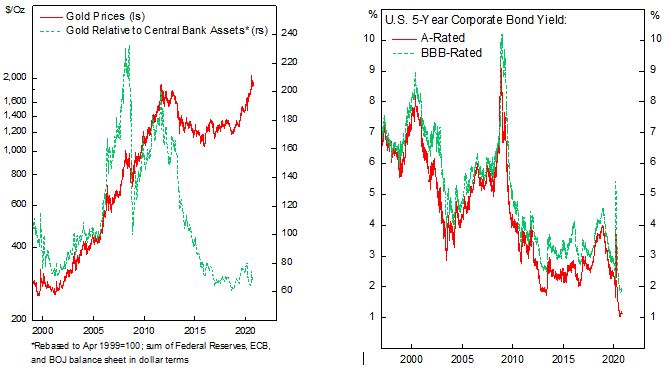

Meanwhile, Federal Reserves’ balance sheet should continue to expand in the next decade to finance the fiscal deficit and support the bond market. With the corporate sector highly leveraged and repos taking over traditional bank lending, the market is highly procyclical and only the Fed could backstop tightening liquidity through expanding its balance sheet. Fed’s commitment and action to print money to purchase public and private debt has so far remain reassuring, which structurally bodes well for precious metal prices. Note that gold prices only correct dramatically in 2013 once Fed is thinking on raising rates and contracting its balance sheet, creating a massive selloff in risk assets globally.

On bonds, we do not think it make any sense for investors to buy corporate bonds, where the nominal yield for A-rated 5-year corporate is only slightly above 1%, BBB-rated at 1.8%, and both are negative in real terms, while the balance sheet structure of private non-financial corporation has become much riskier. In short, investors are paid nothing for taking credit risk. Moreover, time is not on their side for hardly hit sectors such as travel, hotel, restaurant, and other service-oriented businesses. Their already high leverage, combined with collapsing revenue will inevitably force them towards bankruptcy, barring any government help. Commercial MBS (CMBS), airlines, and cruises should remain under (increasing) pressure.

A resurgence of inflation would also be bad news for the financial market, even if policy rate remains at zero. In this scenario, long-term bond yields should go much higher, making refinancing more expensive for the highly leveraged corporate sector. On top of that, the rise in yields, in turn, translates to lower Equity Risk Premium (ERP) and should drive equity multiples lower. The bottom line is that unexpected inflation risk is dangerous for equity prices, as bond market could get spooked and equity multiple adjust downward.

EM Drivers, Country Selection, and Sovereign Bonds

One unifying drivers of EM assets are the dollar (Fed policy) and Chinese growth. Weaker dollar boosts liquidity in the Eurodollar system and encourage funds to go to the periphery in search of higher yielding assets. The stronger EM currency means EM corporate could pay their dollar-denominated debt easier and their collateral value increases, which spur greater lending. Meanwhile, strong Chinese growth drives up demand for commodities, which bodes well for earnings of commodity exporter countries.

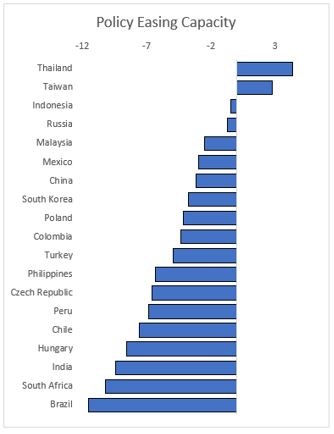

To assess the capacity of EM countries in facing a prolonged economic slump, we rank these countries based on their policy support capacity – measured by real policy rate (%) plus government balance (%GDP). Asian countries, except India, rank well according to this metrics, with Indonesia, Mexico, and Chile as our favorite. Chilean equities are heavily concentrated and correlated with copper prices, whose price have surge of late. The divergence between Chilean stocks and copper price we identified last year has only widened further, creating opportunity for investors. Meanwhile, both the MXN and Mexican stocks are cheap even prior to the pandemic; the dollar weakness should supercharge the rally in the next few years. Indonesian and Brazilian equities are also interesting to some extent, but the later is very prone to external shock due to its low policy rate and poor fiscal condition, which may pressure the BRL from appreciating.

On EM fixed income, we remain constructive on local-currency bonds, especially for Indonesian government bonds, which has the highest real yield across the universe and public debt level relative to GDP remains below EM average. There is also some juice left on long Mexican bond trade, although much of the easy gain has probably been realized.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.