Download PDF:

Brazilian manufacturing sector’s recovery has been surprisingly strong post-pandemic, outpacing other EM countries, despite the still poor health care situation and strict lockdown restriction nationally. However, the strong rebound has not been followed proportionately by the country’s asset prices, contrary to the development seen in Mexico (Chart 1). The country still records contracting manufacturing PMI, but Mexican equity, bonds and currency have all outperformed its Brazilian counterpart. We argue this is mostly due to investors’ concern on the impact of large monetary and fiscal easing done by Brazilian government and central bank in fighting against the virus, which drains the country ability to stimulate further should a prolonged malaise occur.

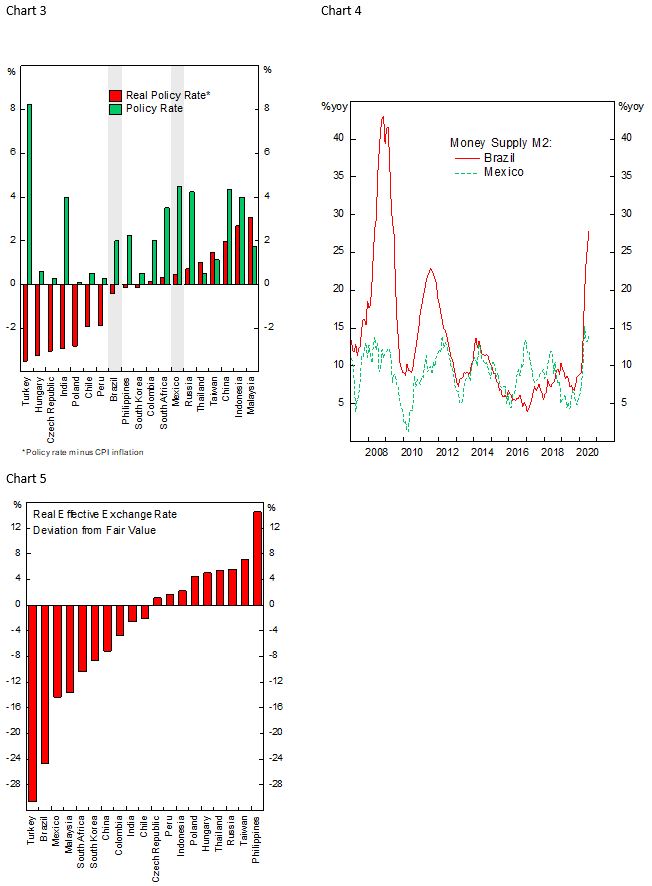

First, in the current policy easing round Brazilian central bank has eased much more aggressively than its Latam counterparts. Since 2019 the BCB has cut rate by 450 bps (250 bps YTD) compared to 375 bps (275 bps YTD) by Mexican central bank, a factor that has been a tailwind for the appreciation Mexican Peso relative to the Real (Chart 2). As a result of this aggressive easing, Brazilian real policy rate turned negative and its 2% nominal rate is no longer attractive for carry trade. Mexican policy rate, on the other hand, is still among the highest in EM and its real policy rate is still positive despite the recent tick up in inflation, providing a floor for the peso (Chart 3).

Granted, Brazilian economy is in a greater imbalance prior to the pandemic and should require larger support for its domestic economy, but the all out policy response by the central bank creates worry that a premature tightening might be necessary to prevent the real from sliding further during period of increasing risk aversion. Of late, Brazilian 2-year government bond yield has already crept to 4.25%, or 225 bps above the current SELIC rate; Mexican policy rate is expected to stay at current level in the next 12 months. Meanwhile, Brazilian money growth is also surging to almost 30% year-on-year growth (Chart 4) and the BCB has been financing the fiscal deficit through government bond purchase in the secondary market. Both are headwinds for the real to strengthen despite being cheap, according to our fair value assessment (Chart 5). Mexican central bank has refrained from buying government bonds and the country’s money growth is much more restrained.

Second, resulting from the large fiscal stimulus announced earlier this year, Brazilian government deficit has deteriorated to above 10% of GDP, worse than during its latest crisis in 2015 (Chart 6). This is on the backdrop that Brazilian public debt is among the highest in EM at 90% of GDP – a number that is projected to grow to 98% of GDP this year (Chart 7). Last month the government announced its 2021 budgetary targe, in which primary and overall fiscal deficit are expected to be around 3% and 6% of GDP, respectively, with no emergency spending related to COVID-19 and no new social welfare program included in the proposal.

In contrast, Mexican government entered this year’s crisis from a much healthier fiscal condition. Under President Lopez Obrador administration, the government has committed to running fiscal deficit below 3% of GDP and the announced pandemic-related stimulus has been relatively muted at around 3% of GDP. The Mexican government this month also announced its 2021 budget, with spending projected to be flat and primary balance at zero. The lack of willingness to spend by AMLO administration means that the fiscal contribution to growth will remain muted next year, with GDP growth more dependant on global economic recovery.

Aside from the urgency for the Brazilian government to control its public debt, the path of reforms undertaken by the current administration is faltering. Investors had also been hopeful that last year’s success on the government pension reform will mark the beginning of a set of reforms overdue to bring the government’s balance to a sustainable path; COVID-19 and political gridlock have shattered that belief. The feud between Bolsonaro and its aides – in trying to curb the spread of the virus and manage the economy – have resulted in the government losing two top economic officials and two health ministers since the pandemic began. Although the case for President Bolsonaro impeachment has decreased significantly as he aligns himself with the powerful centrão political bloc in exchange for political appointments, the country still does not have a coherent strategy in managing the economy and health care situation. In a recent poll conducted by Necton and Vector Barometer, less than half of politicians think the tax reform is going to be passed this year, a significant decline from 78.6% earlier this year.

Lastly, it is necessary to highlight the health care situation and the impact of the resulting lockdown implemented in each economy. Both economies are among the worst hit by the pandemic; Brazil and Mexico record -9.7% and -17.1% QoQ, respectively, in Q2. Both countries have been gradually easing the lockdown restriction despite rising cases and death tolls (Chart 8 and 9), and their governments seem to have given up in trying to reign the virus’ spread. Considering the relatively younger population in both countries and COVID-19 deaths per capita figure, this means that it is non unlikely that a fifth of the population has been infected (0.3% “true” death rate and 65/100.000 deaths, see chart 10), opening the way for herd immunity should the situation does not improve in the coming months.

Macro wise, both countries’ trade surplus has widened this year (Chart 11). Imports have seen larger contraction relative to exports as currencies fall and economic activities slow due to various lockdown measures, reducing the dollar needs of the economy. Brazil, however, has seen its PPI surging dramatically to 25% YoY growth, erasing most of the country’s export competitiveness coming from weaker BRL (Chart 12). This is likely due to the surging soybean prices – which made up a quarter of Brazilian exports – from increasing exports to China (Chart 13 and 14). Meanwhile, Mexican exports have also recovered strongly of late as vehicles exports to the U.S – a quarter of Mexican total exports – rebound. In sum, the recovery in global growth, combined with domestic easing of lockdown restriction, will likely bolster Mexican and Brazilian currencies going forward.

Investment Conclusion

We have a constructive view on both the BRL and MXN due to its cheapness and the prospect of synchronized global upturn that will likely bolster both countries’ exports. Brazilian and Mexican local-currency bonds are also attractive, yielding 7.3% and 5.8%, respectively. Record low nominal and negative real yields across G7 bonds will eventually push more inflow into the high-yielding sovereign bonds in EM; capital flow to EM fixed income has so far been strong and outpaces flow to equities (Chart 15). Meanwhile, the relatively restrained fiscal and monetary easing done in Mexico relative to Brazil, and much healthier fiscal condition, point to the likely further outperformance of MXN relative to BRL and their respective local-currency bonds.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.