Download PDF:

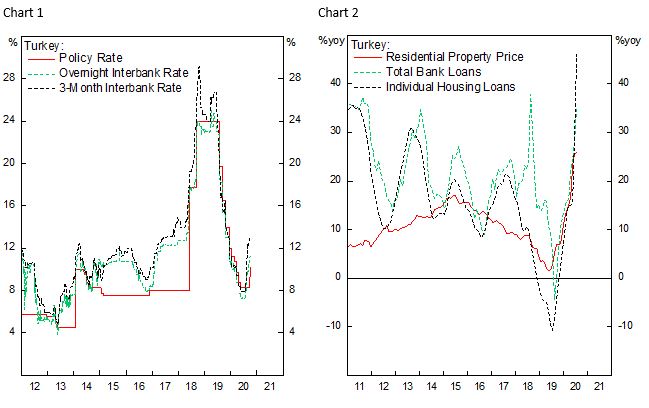

The Central Bank of the Republic of Turkey finally capitulated to market pressure and raised its policy rates by 200 bps last week amid a weakening lira. This is a reversal of its aggressive easing policy since the 2018 crisis, when the central bank has been under government pressure to bring its policy rates into single digit to prop up growth amid double-digit inflation, currently hovering around 12%. Last week’s decision, however, should not come as a surprise. CBRT has been tightening bank’s lending rate – which have historically point to the direction of its monetary policies – since August (Chart 1) and declining foreign exchange reserves have drained out the central bank’s ability to prop up the lira. There are few developments worth highlighting:

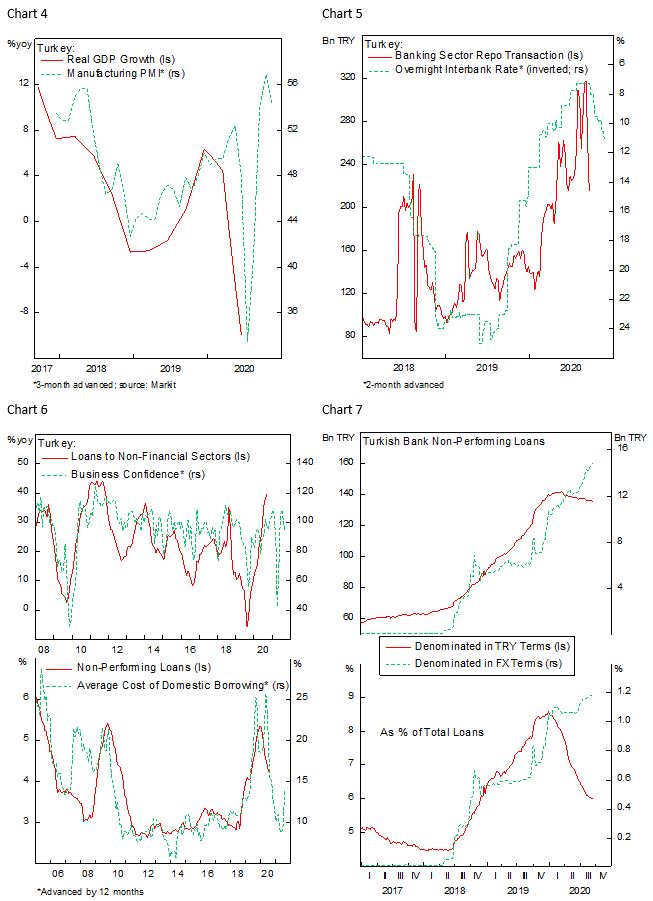

First, Turkish domestic economy has been on a mini boom amid the supportive monetary, fiscal, and pandemic situation since early this year – all of which make a monetary policy tightening more bearable. Residential property prices have surged 25% YoY on the backdrop of weakening lira and easy credit policies – total bank loans are growing at a rapid 35% growth, with the growth of individual housing loans even faster (Chart 2). Turkey have so far recorded a mediocre Covid-19 death rate relative to its population and the country is implementing an unusual lockdown policy – restricting only those above 65 and under 20 years old to stay at home – to support the economy (Chart 3). Granted, growth has dipped by 10% in the second quarter, but a strong rebound in the country’s manufacturing PMI points to a strong recovery in the third quarter (Chart 4); the country’s 2020 GDP is expected to contract by only 1%, among the better one in EM universe.

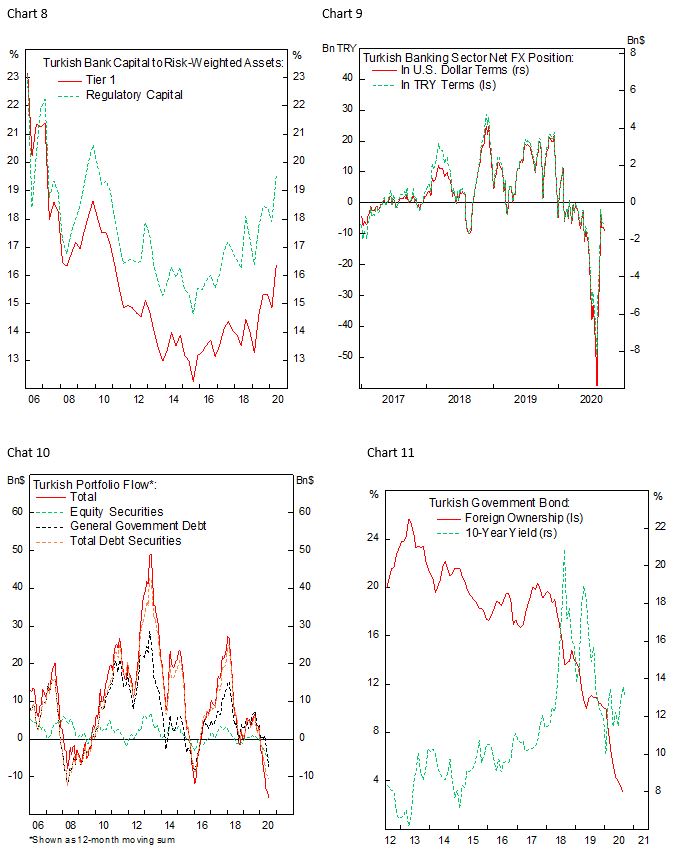

Second, the tightening of interbank and repo rates increases the banking sector funding cost and will force banks to curtail credit, which will have a significant impact to the real economy and the banking sector (Chart 5), in which the latter often triggers a financial crisis. Credit growth will likely moderate going forward and non-performing loans will increase at the margin (Chart 6). So far, the combination of weakening lira and a domestic credit boom has resulted in TRY-denominated NPL going down from its 2019 peak while FX-denominated NPL has steadily risen, albeit at a still low rate (Chart 7). Should the CBRT continue to hike its policy rate, which we think will be the case, we may see a reversal of the trend in TRY and FX-denominated non-performing loans. The saving grace is that Turkish banks are well capitalized, and its net foreign exchange position has drastically improved from the distressing level months ago (Chart 9)

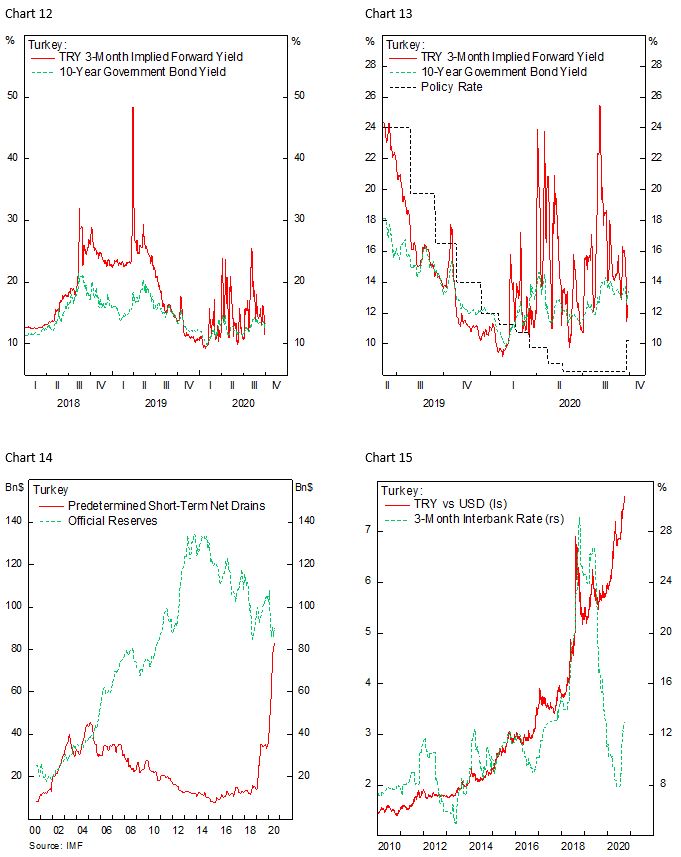

Third, capital flight from Turkey has reached its extreme, far worse than during the GFC. Half of the capital outflow is due to foreigners’ mass-selling of Turkish government debt (Chart 10), resulting in foreign ownership of Turkish public debt below 4%, a far cry from 20% five years ago (Chart 11). Part of the reason behind this is President Erdogan policies in tightening lira offshore supply to fight against short seller, making it expensive to hedge lira exposure for foreigners (Chart 12). After announcing the rate hike last week, Turkish banking regulator also increased the limit of banks’ FX transaction exposure from 1% to 10% of its equity, a sign that President Erdogan’s rhetoric in fighting against short sellers are moderating. It is encouraging that TRY forward implied yield have since declined by 400 bps and the 10-year sovereign bond yield also dropped (Chart 13).

Investment Conclusion

Turkey is still far away from being out of the hole, but last week’s policy actions are a step in the right direction. Official reserves remain low and inadequate to cover short-term external financing needs while policy rates are also still too low considering current inflation level (Chart 14 and 15), as discussed in a previous report. The central bank needs to regain its credibility in setting monetary policy and avoid backtracking its policy once the TRY stabilizes. Amid the gloom surrounding Turkey, however, investors need to be reminded that the lira is cheap, according to our fair value assessment (Chart 16), and a reversal of unorthodox policy and an already extreme capital outflow this year are all supportive for the lira to strengthen from current level.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.