Download PDF:

Precious Metals vs Real Yield

Our positioning on silver call options since July has been rewarded bigly as silver price almost doubled this year as the time of this writing. Although we are not early in the party, we have managed to ride most of the large price movement of late, including the rough 15% correction on the first week of August. Riding the first and second wave of the bull mania is relatively easy, but as prices goes further higher, we are maintaining a cautious stance and will pare our holdings at few target price level, with $30 and $34 level as our base camp. Investors should be reminded that silver prices are highly volatile and a correction of 20-30% has historically occurred both during the bull market and at the end of it.

Going forward, there are several themes that is worth highlighting, including the prospect of back up in yield for U.S. Treasury bonds. So far, the Fed has committed to buying large-scale purchase of government and corporate debt, which has kept a lid on yields. Going forward, Yield Curve Control (YCC) policy will keep yields of short- and medium-term Treasuries close to zero and become a headwind for the yield curve to steepen further. There are signs that it may have peaked at 69 bps in June and will trend downward from current level, despite recent surge at the long end. This mean investor should not short U.S. Treasury despite the supply glut from government issuance unless the Fed steps back from the market intervention and let price floats.

Relating this development to our position on silver, we monitor several high-frequency indicators to gauge the momentum in price changes and “fundamental” ratio that has mean-revert historically. First, as Chart 1 shows, silver price relative to U.S. money supply has reverted to almost its post-1986 average (gold and silver experienced a massive bubble in 1980). Second, the silver to gold price is still slightly below its post-1986 average and has much room to run further (Chart 2). An overshoot is almost always the case for precious metals, and we believe that the bull will continue in the next several months and quarters, with the longer-term price for silver hovering around $30-35/oz.

The counterargument against the bullish case for silver is that real yield of U.S. Treasury is now at two decades high and may mean-revert, making an end to the bull in precious metal prices (Chart 3 and 4). Although it is possible, we think it is unlikely that the Federal Reserve would allow U.S. government borrowing rate to spike significantly, as it would restrict U.S. monetary condition and increase borrowing costs for many still struggling enterprises. The Fed has undershot its inflation target in the previous cycle and may allow inflation expectation to go above 2% before thinking about raising rates, a scenario that is not in the horizon for at least another 3 years. Meanwhile, the Fed will finance U.S. government borrowing through QE program and keep a lid on Treasury yields. Over the past two decades, the size of rebound in yields have become lower amid central banks around the world buying government papers and the excess of private savings looking for safe-haven assets (Chart 5). In this cycle, we expect a rebound in yield would probably be capped around 1.5% while 10-year break even rate could go as high as 2.2-2.5%. This means that real yield could stay negative for a long time.

Investment Strategy in a Weak Dollar World

In the past decade we have seen a world where U.S. economic growth outpace Europe, Japan, and the more developed EM countries. U.S. stocks performance have surged while Europe and EM equities have been largely flat for a decade in dollar terms. Crisis in Greece and Italy have weighted Europe just as political upheaval and Balance of Payment crisis have haunted EM countries, such as the case in Brazil and Turkey. The effect of a stronger dollar hit rest of the world hard: 1) servicing dollar-denominated debt become harder as local-currency value depreciate against the dollar 2) commodity prices took a beating and depress income, not only for mining firms, but also for governments that rely on corporate taxes and mineral exports fee, and for consumers that saw real income stopped growing as fast as in the early 2000s 3) High cost of capital, measured by equity yield and corporate dollar bond yield, have make it expensive for firms outside U.S. to invest in capital stocks, hindering productivity growth.

We have long believed that dollar trend is the major driver not only for EM stocks outperformance, but also for their growth rate. In previous studies, we documented clear correlation between period of dollar strength and deterioration in EM growth rate and asset performance. With the dollar now still overvalued and trending downward, we expect this will be a tailwind for laggards in the last decade finally perform, such as European firms and Emerging Markets. Few of our core investment thesis outlined below:

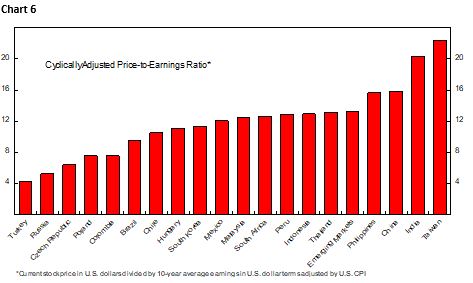

- EM stocks and currency will have a tailwind from a cyclical perspective. Look for entry point to long deeply undervalued countries such as Turkey, Colombia, Chile, and Mexico (Chart 6).

- Despite the political uncertainty and unorthodox government policies, Turkey is well-positioned to be a regional leader in the Middle East region. Turkish manufacturing is well integrated to European automotive sector and the wage advantage is large, considering the Lira depreciation in the past 3 years. Moreover, the country has undergone repeated crisis and equity valuation is currently near record low level (Table 1).

- Colombian equity, which is highly correlated with oil prices, is cheap and the peso is slightly undervalued. Granted, the long-term outlook for oil prices is bleak. Producers have plenty of spare capacity to pump more oil from the ground and Russia and Saudi need the export revenue to prop up their domestic economy. This tilted the balance to oversupply rather than a shortage, even in the case of geopolitical uncertainty in the Middle East. Cyclically, demand for oil will remain depressed as air travel is massively curtailed and global economic recovery has yet to fully materialize. However, the increase in demand resulting from rising living standard in countries like India, Indonesia, and Philippines likely put a floor on oil demand in the coming few decades.

- A derating in Chilean assets have seen its equity price hovering at less than half of its 2018 peak. The slowdown in Chinese growth rate and hence downward pressure on copper prices have a large trickle effect to Chile’s domestic economy. Moreover, low social safety net and inequality issue has finally led to a social unrest in October last year, triggered by an increase in metro ticket price. The constitutional referendum that will be held on October 25th also put into question whether the market-friendly policies that has separate the fate of Chile relative to other Latin American countries will be reversed. However, with global economy on the path to recovery and copper price has shot back to pre-pandemic level, Chilean equity will likely play a catch up and is very attractive at current valuations (Chart 7 and 8).

- Lastly, we like Mexican stocks due to the country’s integration to the North American market through USMCA trade deal that will likely benefit from offshoring of manufacturing base from China. Mexican equity and currency are also cheap, likely already reflecting the poor short-term outlook resulting from the pandemic.

- We think the bear market in commodities are over and cyclical rebound is in the making (Chart 9), with the dollar trending further lower. In the last decade we have seen the soaring of stocks related to electric vehicle (TSLA), electronic gadgets (AAPL), chips (TSMC), and various other advancement in technology, including solar energy, wind turbine, and battery technology. We are likely to see an accelerated demand for these goods in the coming decade, pushing the cost of components for these high-tech goods higher. All these should bode well for industrial metals such as copper and nickel, which are mostly mined in emerging market countries.

- For the long-term story, look for the next China/India in the coming decade. Our first pick is Indonesia, which has grown above 5% rate annually in the past two decades and has a large, 250 million population with the majority still in productive age. Indonesian equity is attractive, according to our Global Equity Strategy model, and Indonesia’s Cyclically Adjusted P/E (CAPE) ratio, at 13x, is much cheaper than other high-growth Asian countries such as India, China, and Philippines (Chart 6). In the past two decades, Indonesian government has largely capped its fiscal deficit below 3% and public debt level as % of GDP is lower relative to other EM countries. Meanwhile, the central bank has became more orthodox and has a bias to maintain stability at the expense of boosting growth through cheap credit. Whereas Chinese and Indian banking systems have liquidity and often solvency problems, Indonesian banks’ Capital Adequacy Ratio (CAR) is much above BASEL III standard and loan-loss provisioning has been aggressive. The bottom line is that Indonesian private and public sector have both undergone through a reform since the Asian crisis and are much less vulnerable.

The discussion above all points out to investment strategy. How should investors allocate capital in their portfolio? We divided our holdings into 4 major asset class: equity investment, hedging assets, commodities, and fixed income. We are currently in the early cycle of an upturn, hence investors should maintain a more aggressive stance and put more weight in equity and commodity holdings, with our recommendation specifically:

- 50% diversified stock holdings and private equity investment

- 25% hedge assets (U.S. treasury, gold)

- 15% commodities and commodity-related stocks

- 10% fixed income holdings, with majority invested in select EM government bonds

Although we have outlined a bullish scenario for risk assets so far, investors should continually watch for the emerging risk, both from geopolitical perspective and the resulting effects of Fed’s aggressive policies.

- The largest party spoiler would be the revenge of inflationary pressure resulting from easy fiscal and monetary policy, and new direction of government policy should Biden win the presidency. Fiscal support has so far support consumer spending and increase savings rate. However, a continuation of aggressive fiscal support under Democrat proposal and Fed’s asset purchase (QE) program will accelerate the rebound in investment spending. A left-leaning policy such as tax increase and redistribution policy will also lower savings rate, which theoretically should boost consumer spending and put upward pressure on inflation. Should inflation come back after more than a decade of easy monetary policy, the Fed may have to increase its policy rate earlier than expected, a scenario in which both bonds and stocks would have a hard time.

- U.S.-China war is a possibility, especially over Taiwan and the South China Sea. Both countries have so far show restraint, but emerging nationalism in both countries may put politics on a more aggressive stance, especially if the economy weaken again. We are not a political analyst, a known unknown such as shooting/proxy war could not be ruled out.

- The Chinese government has repeatedly tightened fiscal and monetary stimulus once the economy is on its early phase of recovery in the previous cycle, fearing that the easy credit has been channeled to unproductive investments and may result in a debt-fueled bubble in the property sector. Weakening of China’s economy is bad for the world and Emerging Markets in particular, with consequences for commodity prices and global yields. Currently, there are signs that Chinese government has passed its peak in providing stimulus to the economy.

- Lastly, we observed concerning development in the bond market, where borrowing cost has been kept at a very low level amid high credit risk of the related firm’s business operation. The combination of high probability of default and low yield due to Fed’s QE program means bond investors are not well compensated for the risk inherent in the fixed income space. This might also be the reason that equity valuation has been soaring. Cheap bond financing reduces the share of profit going to debtholder and enrich equity holder, at the backdrop of U.S. private equity firm stuffing more and more leverage into U.S. corporates in the past decade.

As a closing remark, we want to show one chart that we think is important to forecast equity return in the EM and DM space in the coming decade (Chart 10). If our thesis on the weaker dollar cycle is correct, investors may be rewarded 10-14% annualized return in the coming decade by investing in EM equity compared to 6-10% in DM equity.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.