Download PDF:

EM equity has experienced indiscriminate sell-off during the peak of this year’s market rout, with losses ranging from 20% to 60% across 18 countries. Since its March’s low, however, few countries have staged a strong asset prices recovery, whereas others are still lagging and have barely recover half of their losses (Chart 1). The winners are East Asian bourse, with its more developed economy, ability to fight against the virus, and capacity for the government to stimulate the domestic economy. Meanwhile, the laggards consist mostly of Latam economies, where the disease is still raging, and the government is ill-equipped to launch large fiscal stimulus to shore up social spending and stimulate the economy. However, Latam countries will likely play catch-up in the coming months, as infection cases in the region seem to be plateauing and Chinese economic recovery has drove commodity prices higher.

In this piece, we scrutinize EM countries’ risk-return profile going forward, with the emphasis on a greater understanding of each countries’ vulnerabilities and its position relative to other EM economies. EM vulnerabilities are classified into two part: pre-existing (structural) macro vulnerabilities and pandemic-related concerns. A better comprehension of both macro drivers allows investors to project each countries’ likely path of asset price recovery and the associated risks inherent in each market.

Structural Macro Vulnerabilities

- Current account balance. As global trade was hit hard by the lockdown measures earlier in the year, EM countries that rely on commodity exports saw their current account balance deteriorated, putting pressures on their currencies, as was the case for Colombia, Chile, and Brazil (Chart 2). Meanwhile, countries running large current account surplus have seen their currencies depreciate by less than 5% YTD against the dollar (Thailand, Korea, Malaysia), or even appreciate slightly (Taiwan).

- Fiscal position. Although the fiscal position for majority of EM countries have improved in the past two decades, EM governments do not have the capacity to stimulate significantly as it was the case in U.S. and Europe. Government capacity, measured by fiscal balance pre-crisis and public debt level, is very restricted in countries like India, Brazil, South Africa, and Malaysia, all of which ran sizeable deficit prior to the crisis and had a public debt close to above 60% of GDP (Chart 3 and 4). The situation is likely to deteriorate even further for Brazil, which launched sizeable fiscal stimulus to short up its economy (Chart 5).

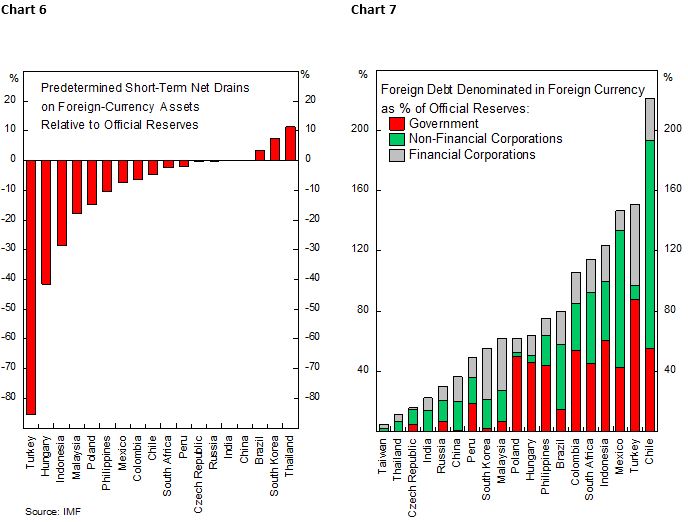

- FX reserves adequacy. With its current account deteriorating, several EM countries have also drained their reserves to meet foreign-currency financing needs, which depletes the countries ability to defend its currency if it was under heavy selling pressure. Indonesian and Malaysian reserves adequacy are low, while the condition in Turkey is becoming very concerning amid the drain from central bank intervention to keep the lira stable (Chart 6 and 7).

Aggregating all these structural measures give us a sense of how EM countries’ vulnerability rank relative to one another and their ability to withstand the crisis going forward (Table 1 and 2). Unsurprisingly, countries with twin-deficit populate the bottom rank in EM universe, which we discuss in greater depth in the following sections. Overall, countries with greater vulnerability have seen their asset prices lag their stronger counterpart but may also provide opportunities going forward as the risk of double-dipped crisis diminish (Chart 8).

Pandemic-Related Concerns

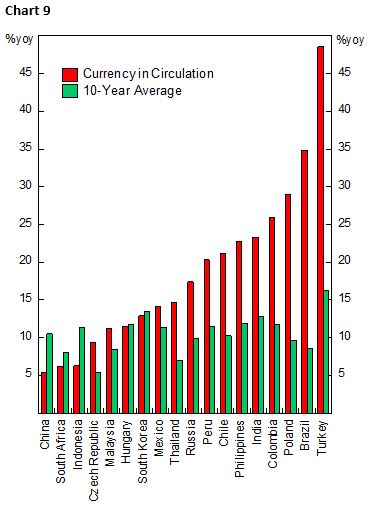

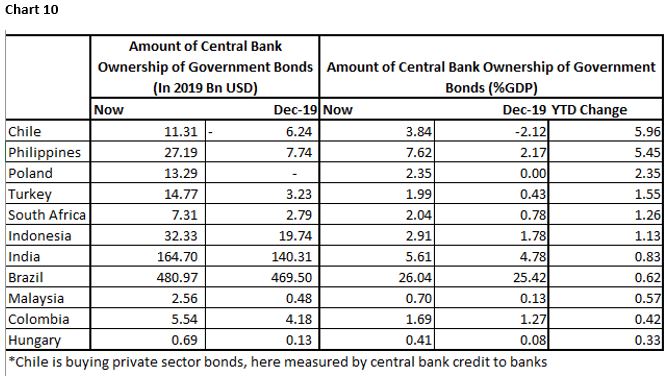

- Money Growth and Government Deficit Financing by the Central Bank. Acknowledging that EM government lacks the room to stimulate through market debt issuance, EM central banks have financed government’s fiscal stimulus by buying their respective local government bonds, many of them in the primary market by printing money aggressively (Chart 9). Quantifying the central bank purchase of government bonds and the increase of currency in circulation as % of GDP, we ranked EM countries based on the amount of “MMT” that the central bank has been doing (Chart 10). There is a case for concerns with regards to Turkey, South Africa, and Indonesia, where the country’s central bank has been buying government debt and the central bank credibility may come into question.

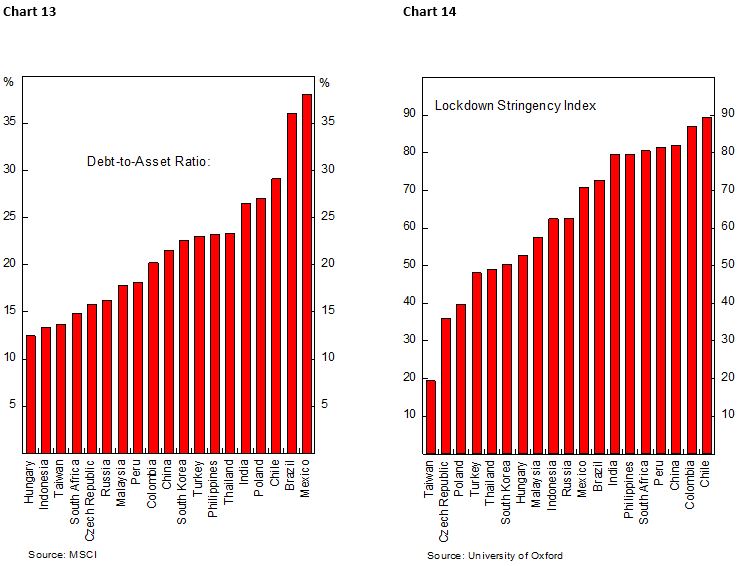

- Increasing Debt Burden Among Corporates and the Risk of Extended Lockdown. Brazil, Mexico, Chile, Turkey, and Philippines particularly stand out due to their combination of above average debt ratio and elevated borrowing cost (Chart 11, 12, and 13). Several public firms have had already entered bankruptcy proceeding and banks have seen their non-performing loans rate rises. Should an extended period of lockdown deprived firms from continuing their operation, it is likely that the situation will worsen for countries with stringent lockdown measures (Chart 14 and 15).

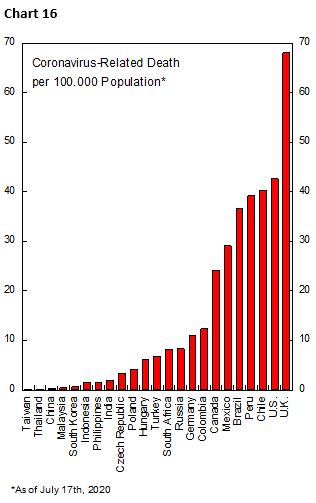

- Coronavirus Infection and Death Cases. Contrary to pundit’s prediction earlier this year, in which many expect EM countries to suffer greater fatality rate due to health system concern and unpreparedness to face the virus, majority of EM countries has so far suffered far less fatality rate relative to the size of its population compared to developed countries (Chart 16). This should be unsurprising as population in EM countries tend to tilt on the younger side, which has significantly lower case-fatality rate than people above 60 years old, many of which resides in European countries. This fact alone may justify many EM government to partially reopen the economy.

Particularly hit hard in EM is Latam countries, with poor social safety net, indebted government, and large informal employment. The region’s fatality rate relative to its population is more than double other EM countries’ average, despite its much younger population. Since the death statistic is more accurate than confirmed cases number, and the “true” fatality rate of COVID-19 infection is estimated to be around 0.5-1% rate, then it’s likely that 5% to 10% of the whole region’s population is already infected, which make the case for a herd immunity more likely should the disease not being contained.

Few Countries to Monitor…

South Africa

- The country is already at a dire state prior to the covid-19 crisis, with large fiscal and current account deficit, on top of concerns on a sizeable public debt level. The state has been weighed by its indebted SOE (Eskom) and unable to provide more fiscal stimulus despite worsening health care situation.

- The country has not grown in the past decade and the domestic condition is ripe for social unrest, with unemployment reaching above 20% even before the pandemic. The country GDP may be among the worst hit in EM and only slowly recover once the crisis subsides.

- The country has not been printing money aggressively, but central bank has so far purchase 0.7% GDP of government debt, which if goes indefinitely may shaken investors confidence in the central bank and put pressure on the Rand.

Brazil and Mexico

- Brazil has undergone a fiscal reform prior to the pandemic, which has unwound much of the progress. High public debt level and 6% deficit has not deterred the government from launching a large fiscal stimulus, which will deteriorate the fiscal position further. All of these is the opposite of the situation in Mexico, where fiscal deficit is low and public debt level is much below its Brazilian counterpart. Moreover, fiscal stimulus related to the pandemic has been low, which arguably provide little help to the domestic economy but put the government at a stronger footing to drive growth going forward.

- Brazil’s money growth, triple the country’s 10-year average, is also a cause of concern. Mexican central bank has so far restrained from buying government bonds, contrary to Brazilian central bank that has purchase 4.5% of GDP worth of government securities, mainly to finance the fiscal stimulus announced by the government.

- Higher real policy rate in Mexico makes the Mexican Peso more attractive for a carry trade relative to BRL. Although both countries have similar leverage picture, the perceived relative safety of Mexican corporates have resulted in lower borrowing cost, which ease the monetary condition by more for Mexican firms.

India

- The country is weighed by the shadow banking crisis since 2018 and growth has been decelerating prior to the pandemic. The government fiscal situation is a cause of concern, with deficit above 7% of GDP and public debt level of 70% of GDP, albeit being mostly issued in local currency. This put the country with very limited room to launch large stimulus to shore up its economy and ramp up social spending amid stringent lockdown measures.

- Similar to other fragile EM countries, the central bank has financed 1% of GDP worth of government borrowing by printing money.

Turkey

- The central bank’s monetary easing is over done. Real policy rate has been cut to negative, and money growth has spiked. The central bank has been conducting “MMT” buy issuing local currency to purchase government bonds when its creditability is already very poor. This is very negative for the TRY.

- Foreign reserves are awfully insufficient. Reserve adequacy is already very low by all conventional indicators (relative to imports, foreign debt, and money supply, etc.), and the central bank has been using its reserves to support the exchange rate. Moreover, the country’s pre-determined short-term net drain (due in 12 months, including foreign currency loans, securities, FX deposit liabilities and CBRT’s financial derivative activities with resident and non-resident banks) has spiked sharply. This means that resources the CBRT has to defend TRY are nearly depleted.

- Turkey is among the few EM countries where inflation is still very tightly linked with currency performance. This creates a potential downward spiral where TRY weakness leads to higher inflation, which in turn begets further currency depreciation. This has been a key motivation behind the CBRT intervention, but market forces will eventually prevail.

- The positive side is that Turkish assets have reflected the risk inherent in the country’s macro environment. The Lira is one of the cheapest currencies in EM and Turkish stocks are trading at a depressed valuation. Moreover, the country’s current account has improved significantly after the 2018 crisis, lowering the risk of an imminent balance of payment crisis.

Investment Conclusion

Remain positive on two high-beta play in EM: Chile and Mexico. First, both countries’ fiscal situation remains healthy even after accounting for stimulus announced related to covid-19 relief. Second, money growth, although rising, are not “out of control” and the central banks have been more restrained in financing government stimulus (Mexico is doing none so far and Chile central bank in June announced special asset purchase program of $8 bn, or 2.7% GDP, for 6-month period). Third, both equity markets and currencies are cheap for both countries. Lastly, lockdown stringency is high in Latam amid rising infection cases, making the region the biggest gainer in light of potential vaccine success.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.