Download PDF:

The Money Flow: How the Money Goes Around

From a macro perspective, there is only three players that drive the economy and financial markets in a country: households, private corporations (including banks) and the government. Each player’s action impacts the other and altogether they drive the economic machine of supply and demand, and savings and investment.

The household sector is comprised of regular person and family like you and me, who earns income by working in the corporate sector and spend it on goods and service produced also by the corporate sector. But that is not the whole picture. Households also pay taxes to the government and enjoy the public utility maintained by the Federal and State government.

The corporate sector, on the other hand, receive their income by selling goods and services to both government and household, and spend their money on investments, paying salary to household sector, and paying taxes to the government. In majority of Western World, households and corporate play a sizable role of a nation economic activity.

Chart 1. Economic Sector Interaction

The sum of demands from corporates, households and government translates to aggregate demand in the economy, which we could quantify with GDP figure. Behind all these, money flows from one sector to another, whose amount is largely controlled by the central bank through monetary policy.

Chart 2. Economic Sector Interaction

The big question now is, what happen then during financial crisis or the current COVID-19 crisis? Understanding the linkage between sectors allow investors to spot opportunities in the financial market. First, as a result of lower consumer and business confidence (either through lockdown restriction or the fear of losing their job), majority of households will reduce their consumption and increase their savings to prepare for a loss of income in the future. Lower consumption is bad for businesses, who see their revenue fall and has to cut cost to maintain profit. This cost cutting exercise most often means laying off redundant employees or reducing their salary, which hurt the household sector further. A spiral of this cycle could evolve into a recession or even a depression.

To break the cycle, the government has to intervene in the economy and put a stop to the vicious cycle. Through national unemployment insurance, unemployed households will receive assistance from the government coffer, while a tax break or government-guaranteed loans will shore up corporate’s balance sheet. Those are the more traditional measures of help provided by the government during an economic downturn. But these aides are not without its cost. Government also suffer from much reduced income tax, corporate tax, and VAT income during the slowdown. As a result, government has to run deeper fiscal deficit and issue debt to finance its new spending.

Back in the old days, government tried to run fiscal surplus during good times and reduce the amount of debt relative to the economy. But nowadays, a combination of political pressure, excess private sector savings and low inflationary pressure has led to an increase of government debt financed by the central bank, which has the ability to print money. In short, government debt no longer has to be sold only to investors, but to the country’s central bank. This development creates an “easy money” mindset at a time when inflationary pressure is low. Government do have to counter excess in private savings by spending more when the economy is running below potential, but they also has to trim back spending and let the private sector take the lead when the economy is recovering as to not crowd out private investment. And how do we know when the economy is running close to potential the answer is by watching inflation.

The issue of central bank financing of government fiscal in Emerging Markets (EM) countries is that investors does not have the confidence on EM countries’ central bank and are concerned regarding debt sustainability. Done wrongly, central bank purchase of government debt could spook investors and trigger a renewed selloff, causing currencies to fall and yields to go higher. The fall in currency will burden FX-indebted firms further and might trigger a sudden stop in the country’s capital flow. Should central bank intervene in the market to prevent the currency from falling, reserves assets will fall and further put into question the country’s macro risk.

Now to the bottom line, what is the outcome of a crisis and what asset class benefits most in each phase of the cycle?

- Lower income for households, corporates, and government. This results in lower aggregate demand and slower growth condition.

- Consumer discretionary will suffer relative to staples. Materials and industrials likely underperform.

- Government fiscal deficit gets larger and public debt level higher.

- For most developed countries, bond yields will go down despite the larger deficit and debt, as private savings rises. In this case, government deficit only acts as a countermeasure to the fall in private sector demand. The dollar normally strengthens amid risk-off sentiment, although another hedging instrument might perform better, i.e. gold and JPY.

- For most emerging countries that is considered as fragile (running both fiscal and current account deficit), bond yield will spike due to investors asking for more compensation to default risk. Especially risky is countries with high public debt level before the crisis and experiencing slow real GDP growth, such as the case for Brazil. Countries with inadequate FX reserves and high external financing needs will also see its currency fall.

- Corporate leverage rises. Resulting from fall in equity values, firms will see their leverage increases at a time when income is falling. Firms might also issue longer term debt to replace commercial paper financing activities and finance working capital. The increase in debt level and borrowing cost is worrisome and might drive weaker firms into bankruptcy. This is the reason central bank has to intervene and brought borrowing cost lower for illiquid but solvent firms.

- Savings rate increases and investment falls

- Disinflationary pressure and risk haven demand mean bond yield likely head lower.

- As a result of central bank intervention to finance government deficit and asset purchase program, currency in circulation increases, devaluing fiat money relative to real assets. This is often said as “inflating the problem away”.

- Real asset prices will go up due to the lesser value of a dollar. Commodity, precious metal, real estate, and stocks will likely perform well in this situation. Remember that stocks are ownership of a business, whose price adjust to inflationary pressure and hence could be considered as a real asset.

Investment Ideas

1.Do not short broad U.S. equity market and fight against the printing press. U.S. equity market is developing signs similar to the millennium bubble amid low rates and supportive fiscal stimulus that support consumer spending. Moreover, after adjusting for currency in circulation, S&P500 level, while not cheap, does not seem to be elevated. While at some point in the future the market will pay more attention to valuation, shorting the market could be a very expensive lesson as long as money and liquidity remain plenty.

2. Shorting Treasury bonds seem to be an appealing idea as economic activity recover. However, Fed’s commitment to keep rates low and purchase of government bonds will pressure borrowing cost to remain low. This also mean that 10/2 spread might not reach its 2-3% peak in this cycle if the Fed does not allow yield to go higher. We have a short bias, but a low conviction on this thesis.

3. Commodity and precious metal bull run are in the making. Buy gold and silver. Both metal prices after adjusting for currency in circulation remain at the lower end of its historical range. Although prices have rallied significantly in the past year, much more upside is available, in our view. A tripling in prices for both metals from current level is not impossible and had happened during the 2000’s. Silver is likely to be the biggest winner should this scenario unfolds, as its price relative to gold is still near historical low and a further run is very likely.

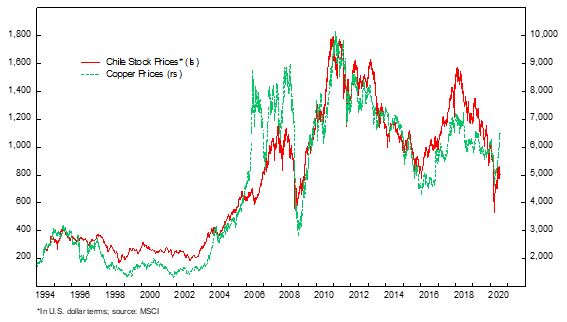

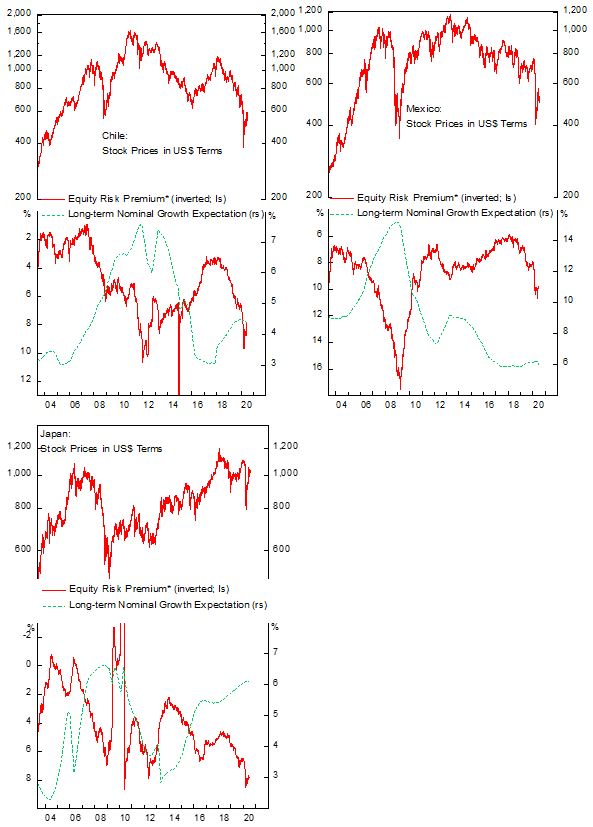

4. Buy equity, especially Chile, Mexico, and Japan. Chilean equities benefit directly from Chinese reflation effort (copper/gold ratio) and fiat money devaluation that drive commodity prices higher. Moreover, the market has been underperforming copper prices significantly and offer attractive buying opportunities even if copper price rally stops at the current level.

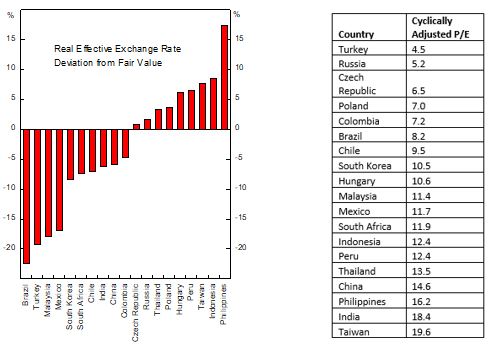

Mexico and Japan are also cheap based on various valuation metrics below, although not as attractive as Chilean and Turkish stocks. We downgraded Turkey more recently, after closing on a sizeable gain from a leveraged long position this year, as the political and reserves adequacy might be an issue and put pressure on the lira.

Copyright © 2020, Putamen Capital. All rights reserved. The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.