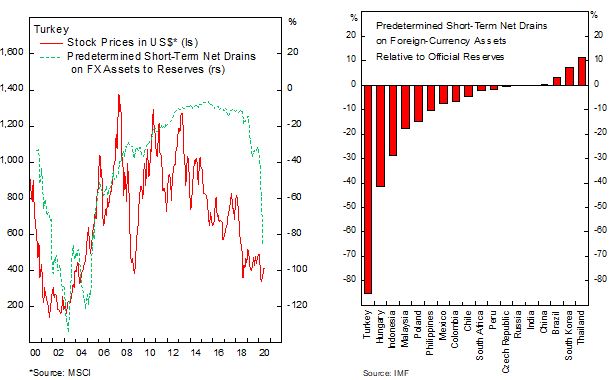

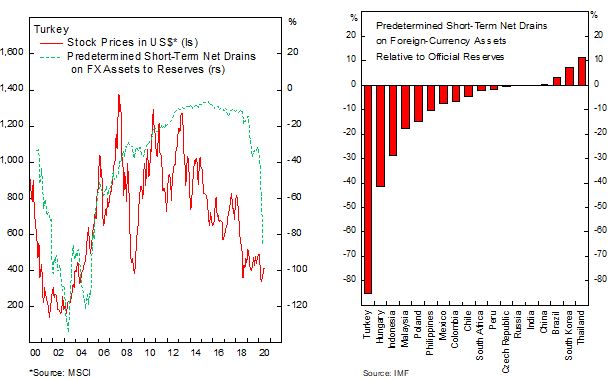

For the past several quarters, we have maintained a constructive view on Turkish assets, particularly on the country’s equity and currency, as valuations are already significantly depressed even before the COVID-19 rout. Percentile of equity multiples for Turkish equity is near its two decades low and the Turkish Lira is more than 20% undervalued, according to our fair value estimate. Turkish assets entered the rout this year from an already depressed level amid a weak rebound following 2018’s Balance of Payment (BoP) crisis. However, the controversial policy conducted by the Turkish central bank and their intervention in the lira have drained their reserves to a very low and dangerous level relative to their FX financing needs. Moreover, the central bank has been printing money to buy government debt as part of the government fiscal stimulus related to the COVID-19 pandemic. Below we discussed the good, bad, and ugly of Turkish market:

The Ugly:

- Our main concern on Turkish reserves adequacy remains, as the country is facing high external financing needs in the next 12 months. Turkish central bank has been conducting FX swap with domestic banks and foreign central banks to meet FX demand, including $15 bn swap with Qatar. This swap line, totaling $54 bn currently, contributed a bulk 60% of the country’s $90 bn gross reserves. With an estimated $77 bn in foreign currency needs, Turkish official reserves are inadequate for the central bank to both intervene in the lira and meet its financing requirements.

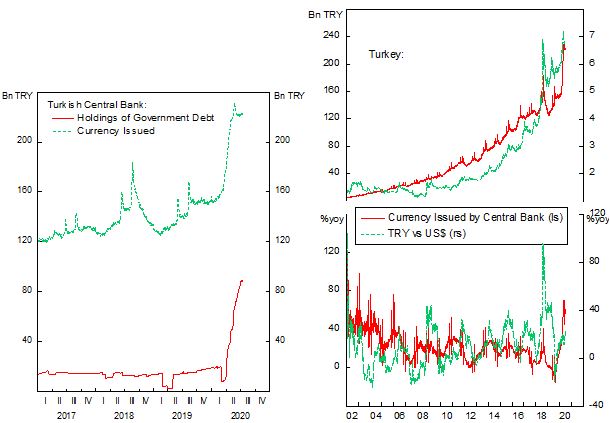

- Turkish central bank is aggressively printing money to buy government debt in the past few months, which may stoke further inflationary pressure and put the lira in jeopardy. The central bank holds TRY 90 bn, or 1.7% of GDP, of government debt, purchased by printing money. This will stock inflationary pressure and weaken the lira. However, the lira is very cheap in real effective terms, which should put a floor on further weakness. But should inflation run out of control again, another round of lira weakness could not be ruled out, creating a downward spiral of currency collapse and accelerating inflation. We think the central bank intervention will prove to be futile and lira will experience a significant correction from current “peg” of 6.85 per dollar.

The Bad:

- Turkish inflation ticks slightly higher in May (11.39%) and June (12.62%), but monetary policy has been put on a tighter leash, as the Central Bank did not cut policy rate as was expected last month. This is a positive news for the lira, as investors have been worried about too aggressive policy rate cut, signaling that monetary policy may turned more hawkish going forward. Policy rate hike could not be ruled out as the central bank fights against inflation and currency attack.

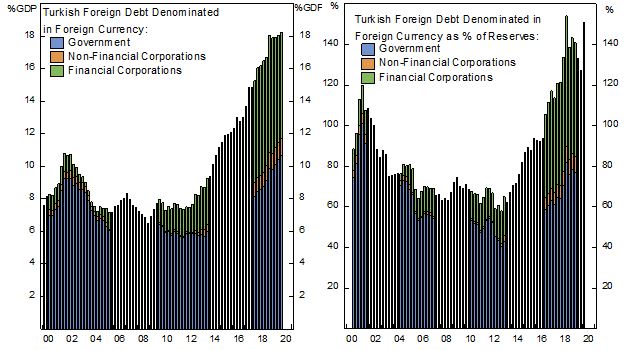

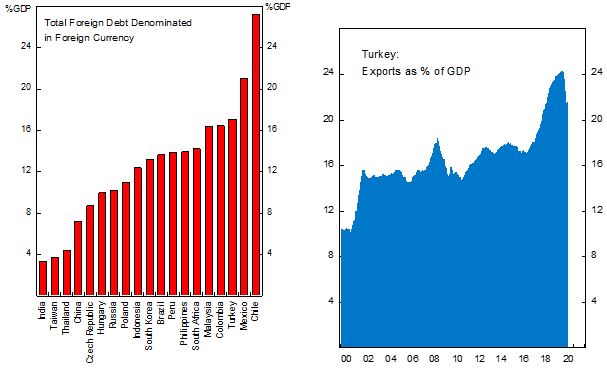

- Turkey stands out among EM as one of the countries with highest foreign debt borrowing relative to its economy, half of it contributed by government FX debt issuance. This currency mismatch makes the country prone to dollar liquidity squeeze, as happened in March.

- As a moderately open economy, Turkish manufacturing and tourism sector have been hit hard by the pandemic. However, the relative success for Turkey to bring the infection cases under control has allowed the economy to remain partially open. Moreover, Turkish firms are well-integrated with European manufacturing sector, which has been resuming its activity of late.

- Turkish government is embarking on an unorthodox policy to restrict market access and availability of the lira in the international money market to stop the lira from depreciating further, such as the recent short selling ban on stocks and the lira for six international banks. The country has backtracked from it since after a pushback from MSCI and other institutions regarding the country inclusion in EM universe. Currently the country weights only 0.5% in the MSCI EM benchmark.

The Good:

- Resulting from the 2018 and COVID-19 crisis, Turkish assets have been battered down and is currently trading at a very depressed valuation. Percentile of equity multiples for Turkish equity is near its two decades low and the Turkish Lira is more than 20% undervalued, according to our fair value estimate. As a high beta play in EM, Turkish asset prices likely to benefit most from the easing of monetary policy and growth outlook improvement.

- As country with high level of FX debt relative to the economy, Turkish stocks and currency are highly sensitive to the fluctuation in the dollar, which we expect to grind lower. Cheaper dollar will likely ease the pressure for the lira and make it easier for corporates to service their foreign-currency debt.

The bottom line is that despite cheap assets valuation, we are getting cautious on Turkish equity and pared our holdings significantly due to the lira risk. We will enter the market once the reserves issue is improving and speculative attack on the lira abates, or the after the lira corrected. Another alternative is to hedge long Turkish equity position by shorting the lira against the dollar.

We will monitor the central bank policy carefully, as their intervention in propping up the lira is draining their reserves and unsustainable. Should the central bank forego this policy, the lira may weaken. However, should they turn hawkish and rise the rate to counter inflationary pressure and attack on the lira, the domestic economy will got hurt, which may also weaken Turkish asset prices. A tricky balancing act indeed.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.