Download PDF:

Various quarantine measures imposed across EM countries to curb the spread of COVID-19 has put government, corporate and household at an unprecedented amount of pressure. Unlike in U.S. and Europe, where outsized government fiscal stimulus is being rolled-out to help consumers and corporates to weather liquidity pressure during the lockdown period, the responses by majority of EM government have been tepid and slow. Differences in balance sheet strength among corporate sector, household’s ability to cope with temporary downturn, fiscal balance and public debt dynamic, banking sector health, and external financing requirement will all determine the survival and path of recovery for EM countries’ asset prices. Some observations are in order:

• EM corporates have a more conservative balance sheet and lower leverage compared to its DM counterpart, making it more likely to survive period of liquidity crisis resulting from falling revenue due to various lockdown measures. On aggregate, more than half of EM countries hold ample cash balance exceeding their short-term liability needs (Chart 1). In other words, these firms could still service their short-term debt and working capital need without relying on operating cash flow. From this perspective, Mexico, India, and Turkey face a much higher liquidity risk.

The good news is that Mexico and India, although being one of the more highly levered across EM (Chart 2), have a much lower debt servicing cost as a share of its income (Chart 3). This means that even if operating income fall by 50%, their firms are still likely able to service the debt. On the other hand, South Korean and Chinese firms, suffering from earnings contraction amid last year’s trade war, are increasingly at risk of being caught in the middle of a spat between U.S and China, which may see rising risk premium amid headwinds in earnings growth. The fall in currency value and increasing borrowing cost also put Brazil and Turkey in the spotlight, the later whose economy is still recovering from 2018 crisis before the pandemic happened.

Gradual lifting of quarantine measures and release of Q2 financial report will shed more light on the damage to firm’s bottom line and their solvency risk. The still increasing spread of COVID-19 infection in countries like Brazil, India, Indonesia, South Africa and most Latam countries likely delay the resumption of business activity and weigh down equity prices. Other than observing the infection trajectory for these countries, investors should also monitor renewed weakness in respective countries’ currency and financial condition, which may push firms with weaker balance sheet into bankruptcy. As for trading opportunities, Indonesian corporate dollar bonds stand out in our assessment, as the country faces one of the highest increases in dollar borrowing cost despite having cash balance above short-term liabilities and is one of many EM countries with low leverage profile (Chart 4).

• Households across EM countries, the majority of which work in informal sector with scant welfare protection (Chart 5), have also suffered from a double whammy of the lockdown. Apart from losing their income, rising food prices has also further dent consumer demand. The good news is that broad-based Inflation continue to tumble despite the falling local currency, contrary to previous EM crisis. In countries with historically high inflation rate, such as Brazil, Indonesia, and Mexico, almost all category of prices continued to suffer from disinflationary pressure, with food prices the only exception. The fall in CPI inflation is contributed mostly by the deflation in transportation prices, hit hard by the lockdown measure and falling oil prices. As the lockdown measure is gradually lifted globally, we are likely to see accelerating inflation across EM countries from rising import cost and rebound in demand. From the perspective of consumer demand, Emerging Asian countries with higher savings rate, acting as a buffer for lost employment income, will likely stage a faster rebound relative to its Latam counterpart (Chart 6).

• EM government, many of which are already running fiscal deficit and have high public debt level, has a limited capacity to stimulate the economy relative to its DM counterpart. The combination of falling tax revenue and rising welfare expenditure resulting from the crisis will see many of the fragile EM government fiscal break the 3% deficit threshold, most of which will be financed by debt. All these put a spotlight on the “usual suspect”. On sovereign dollar bond issuance, Turkey stands out as the government borrows heavily in hard currency (Chart 7). Among large issuer of local currency debt, sovereign risk is also increasing significantly in Brazil and South Africa (Chart 8), both of which suffers from massive currency depreciation and spike in local currency and dollar bond yields. Meanwhile, Indian government bond yield and currency have been relatively stable during the rout despite high borrowing level. For trading opportunities, we like a speculative long on Brazilian and Mexican bonds, currency unhedged. Both countries stimulus has been small, which should limit the increase in government debt and both currency and bond prices have fell to a very attractive level (Chart 9).

• Banking sector: Russia and India deserve a more careful attention. The shock in oil price and production curb will likely stress Russian government finances and limit the recovery of its highly oil-dependent economy. Separately, the blow up in Indian shadow banking sector in the past few years has also resulted in a significant rise in NPL, requiring higher provision and weighing Indian banks ability to distribute credit to support the rebound in businesses. Maintain underweight Indian equity in a managed EM portfolio (Chart 10 and 11).

• External vulnerability: Chile, Mexico, Turkey, and Malaysia are at a higher risk of balance of payment crisis due to its inadequate reserves relative to short-term financing needs and high foreign-currency liabilities (Chart 12 and 13).

Bottom line:

Mexico, Brazil, India, and Turkey’s corporate sector have a higher risk of liquidity crisis, which may become solvency risk. Indian banks are entering the crisis with an already weak balance sheet, which may restrict credit and prolong the recovery. Emerging Asian countries will likely lead the recovery in demand, as their household sector has a relatively high savings rate and buffer during the quarantine period. Inflationary pressure will gradually come back once the lockdown restriction is lifted and oil price rebounded, but a spiral in inflation is unlikely. Sovereign risk is elevated for Turkey, Brazil and South Africa due to investor’s debt sustainability concern, but we believe that the macro profile before the pandemic was much better than in early 2000, which warrants a more positive but careful monitoring.

Thoughts on EM vs DM Rotation

We have noted before that EM companies have less leverage than DM, especially U.S. firms. If after the pandemic DM/US companies shift their focus to strengthen balance sheet, this will have many consequences that support our thesis on EM outperforming DM:

1. From the business side, ROE will be lower. The pandemic shows that increasing efficiency at all cost is no longer justified, which put EM firms in a better light. Breaking the DuPont equation again:

a. Leverage= the downward leverage adjustment will be more pronounced in DM than in EM, where net leverage is already low and even problematic such as in South Korean firms due to cash hoarding.

b. Asset turnover= turnover will be lower due to larger balance sheet. EM firms balance sheet will likely stay unchanged, whereas DM/US will see larger cash balance, accounts payable and receivable.

c. Margin= higher operational cost is likely as there will be inefficiency coming from increasing health standard, multiple sourcing of goods to diversify supply chain, etc. The impact will be greater for firms in higher value-added chain (assembler/DM) than in lower one (manufacturer/EM). But both EM and DM are likely to face headwind on this factor.

Except for the margin factor, the business factor favors EM to DM firms.

2. From the financial side, earnings growth will be much slower due to significant slowdown in buybacks. The lower EPS growth justify lower valuation multiple, putting more pressure on DM firms where investors put a higher expectation on growth. However, at the same time bond yield is much lower, which benefit both EM and DM firms and may justify unchanging forward P/E ratio going forward. If anything, the net impact should be higher EM valuation coming from lower yield environment and perhaps unchanging valuation for DM/US firms (slowdown in EPS but lower yield environment).

3. From sector/cyclical point of view, I think we want to be more positive on cyclical stocks where valuation is dirt cheap on the back of rising Chinese stimulus and improving growth profile.

a. Commodity price recovery has been showing encouraging trend (below).

b. In my view, EM is the strong balance sheet and DM is the weak balance sheet. However, in the short-term, fiscal help (employment subsidy, loans guarantee) for DM/US firms are significantly higher, whereas EM firms get barely any help from government. It is a remarkable achievement if EM firms to survive this crisis, as revenue crash and financial condition tightened.

All these likely led to rerating of the multiples gap between EM and DM firms, the case we made in our EM Valuation report. Price-to-book of DM firms will have to shift downward if ROE decline.

Risk and Portfolio Strategy

We remain positive on risk assets in the medium term, given the improving economic condition as the lockdown is lifted. On a global risk/reward trade off, it is clear to us that investors would do well by buying risk assets in the current environment, as treasury yield is near all time low and copper/gold ratio is at a historical support (Chart 14 and 15). We see further asset rally in Q3 with few notes: 1)U.S.-China geopolitical risk especially related to Hong Kong and Taiwan. It also remains to be seen whether China could fulfill its promise to buy U.S. agricultural goods and other exports in-line with the Phase 1 agreement.

2) We see little risk that another mass lockdown will be implemented even in the face of surging COVID-19 second wave. However, we couldn’t rule out this scenario as the medical development on vaccine is still uncertain and to early to judge, on whether an effective vaccine will be found and could be produced at a mass scale before the next flu season.

3) Since the past few years, we saw increasing risk in “Tech Battle”, which will weigh U.S. stocks in particular due to high weighting on IT sector. Increasing regulation on privacy, freedom of speech vs hate speech, data portability and other issues are all likely to be a headwind for the giant tech firms to grow globally. A GDPR-like rules could be implemented in the IT sector, separating content and distribution channel that will increase competition and reduce margin for Amazon retail segment, Netflix/Disney+, and to certain extent, Facebook and Google.

On a micro basis, we acknowledge that many firms have suffered greatly from the reduction in cash flow and tightening financial condition, but we believe that EM firms in general, less levered than its DM counterpart, have a higher buffer to weather the liquidity crisis. After April’s rally, EM valuation is no longer “dirt cheap”, but is still attractive. Moreover, EM currency has undergone through a massive correction against the dollar, and few are offering attractive trading opportunities, such as ZAR, BRL and MXN (Chart 16).

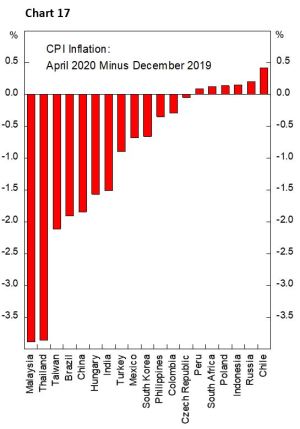

On a macro basis, inflationary pressure has not erupted across EM countries despite the currency fall (Chart 17), which will likely translate to real effective exchange rate correcting upward due to nominal appreciation rather than rising inflation. Furthermore, the rise in sovereign bond yield has been milder than previous crisis and has abated significantly in recent weeks. The weakest link in terms of sovereign risk is Turkey, as reserves adequacy is low, and the country is facing a sizeable short-term financing requirement.

Our portfolio currently holds levered strategy focused on Mexico and Turkey equity market, with occasional hedging using S&P 500 futures. This allows our portfolio to enjoy the upside when we want exposure to beta and be market neutral when we think downside risk is increasing. The strategy has been working extremely well this year, with a return of 37.2% YTD, after suffering large losses at Q4 last year. This strong performance brings our portfolio return slightly above our all time high.

We will continue to focus on our investment process, believing that decent outcome will be achieved on average by maintaining discipline on our investment decision. The quantification of Market-Implied Cost of Equity (MICE) has also greatly enhanced our input in determining risk/reward for each market. We encourage a more quantitative readers to delve into details in our MICE section of the website.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.