Download PDF: Monthly_202001

In this first publication for 2020, we are outlining our bullish view on selected EM countries which will likely benefit as investors diversify from U.S. equities. It has been pretty much a consensus by now that risk assets will likely to do well this year, with some strategists betting on the value/growth and EM/DM turnaround. Despite agreeing that risk assets are likely to do well, we continue to be selective on our country allocation, preferring those with depressed earnings and valuation profile, as they likely to benefit most from the current global growth pick-up.

First, we have three big ideas worth pondering, centered around Emerging Markets countries, which has been undergoing a gradual but broad change:

- EM as a Driver of World GDP Growth.

EM countries will be on a transition from a trade-based economic growth to domestic-driven growth, as highlighted by the flat/declining net exports of most EM countries in the past two decades. Moreover, except Latin American countries, many EM countries investment growth has been exceeding their consumption growth. Accumulation of capital goods is the key to boost productivity and growth and the countries charted below seem to be potential winner in the next decade.

According to our calculation, with world GDP at US$85 Tn and growing at 2% rate (adding $1.7 Tn annually), the combination of Indonesian, Indian, Russian and Turkish ($ 6.1 Tn economy in total) growth alone will contribute roughly 20% of world’s growth. Including China on the list brings the contribution to world’s growth to 75%. These five countries are likely to take greater role in determining world’s geopolitics and economic cycle outside the U.S. Moreover, the increase in share of “middle class” households and favorable demographic/labor market profile in EM countries relative to DM should drive consumption growth relying more and more to EM countries.

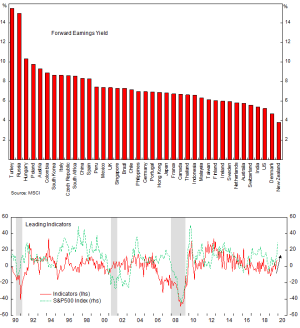

At the time of the writing, Russian and Turkish equity market is trading at the cheapest valuation among the five countries, with Russian equities heavily tilted toward energy companies. Trailing P/E ratio for India, Indonesia, China, Russia and Turkey are as follow: 23, 18, 14.5, 6.2, 8.4 times. Among them, we favor Turkish and Indonesian equities, in which both are well diversified and have a higher long-term earnings growth potential. Indian equities, meanwhile, are promising on a long-term period but will likely moderates within the next 12 months as valuation is steep and earnings are weighed down by the current slowdown.

Bottom line: Alongside U.S., Japan, Germany and U.K., we believe these countries deserves a core position in investors’ equity portfolio.

- Continuation of Bull Market in Commodities Bode Well for EM Equities.

Infrastructure spending in EM and FM countries, transition toward green energy (electric cars, battery storage) and demand for technological goods will all drive up demand for commodities, especially copper and nickel. In the next decade, it is likely that we will see acceleration of these trend, which will, in turn, benefit net commodity exporter countries such as Chile, Peru, Indonesia and several African countries. This decade, many EM countries’ growth has disappointed as exports have suffered from a sluggish commodity price. Moreover, growth has been mainly driven by consumption, which have less multiplier effect relative to investment-driven growth, which we think will take a greater role going forward. Indonesian and Russian government has been pushing for a massive infrastructure building across the country, which bode well for current growth profile and raise the population living standard. Supported by the declining government borrowing cost and room to expand fiscal expenditure, in the case of Russia, the effect of government-led investment is will be positive for the country long-term outlook.

However, we should also assess the impact of higher commodity prices to each of EM countries, as the current trend of higher oil price is a positive for Russian fiscal and Balance of Payment condition, while hurting net energy importer such as China, India and Turkey. Our bullish call on copper prices, should it be proven to be correct, is likely a massive tailwind for Chile and Peru.

We could argue that a commodity bull-cycle in already in the making and likely to create trickle-down effect into domestic EM economies, which in the end is reflected in the country’s stock prices. Although we argued that many EM countries are now net importer of commodities, but EM overall, including Chinese stocks, seem to correlate well with commodity prices. A pick-up in Chinese growth will raise the demand for commodities, which then indirectly benefit consumers in countries such as Indonesia, Chile, Peru, Brazil, Russia and other net commodity exporters, allowing them to buy more goods from China. The cycle repeats until the inventory build up becomes excessive and unwind, creating a 2-3 years cycle we have seen since the 2008 financial crisis.

On the equity side, we have been researching the reason of underperformance of EM relative to DM, finding that most EM firms/sectors have significantly lower leverage compared to its DM counterparts. This results in lower ROE of EM equities and the market is rightly pricing it with lower P/B value. However, we are arguing that the decline in borrowing cost across EM countries will eventually shift firms’ capital structure toward greater debt share, improving ROE. Should this happen, a rerating of EM equities is likely.

- Emerging Markets Country Profile Are Improving and Its Assets Are Massively Under-Owned.

EM countries profile has greatly converged toward their more developed counterparts in the past two decades. There has been fewer country in crisis and contagion is less likely as most countries have been building significant buffer (international reserves) and capital in the banking system has been greatly increased toward Basel III standard. Russia, for example, was very vulnerable back in 1998, as highlighted by the ratio of its reserves relative to foreign debt, but has became safest in this decade. In fact, we think Russian government bond yield is likely to undergo a gradual shift downward toward levels equivalent to other countries with current account surplus such as South Korea and Thailand.

Inflation across EM has also been on a structural decline since 2015 and likely to stay under control as floating exchange rate acts as a buffer to shocks. Countries historically fighting against high inflation, such as Brazil, India, Indonesia, Mexico and Russia, are now having sub-4% inflation rate. This allows the central bank to loosen monetary policy, driving credit and growth higher.

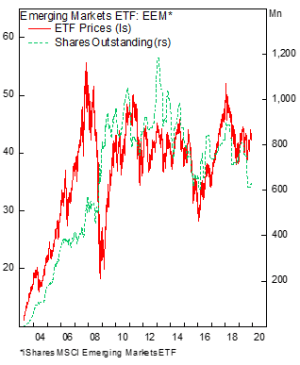

More importantly, the underperformance and higher risk of investing in EM countries have dimmed investors interest in this asset class, leaving more opportunity for investors with greater risk tolerance and ability to synthesize both economic and financial data into investment conclusion. Sometimes, a simple mean-reversion thesis and a small allocation on a crisis-stricken country could result in sizable gain for investor’s portfolio. We believe that under-owned and under-represented EM equities in global portfolio limit the downside of foreign outflow from EM countries and is likely to trigger strong inflow should EM countries’ macro profile stay stable (inflation, public debt, government deficit, etc.) as earnings yields remain high.

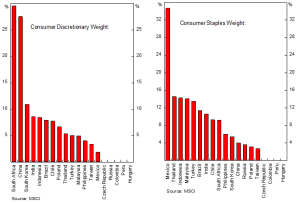

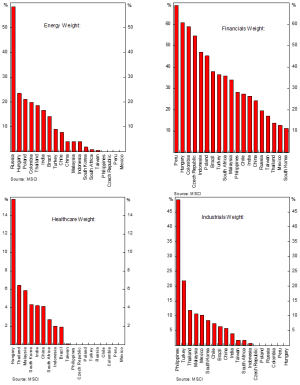

EM Country-Sector Weights

In the charts below, we provided data on sector weights of all EM countries that is useful for us in understanding the growth/value dynamic of each country. For example, our current thesis on higher commodity prices lead our attention to countries with higher material sector weights, such as Peru, Russia, Mexico, Brazil and Chile. From this list, we narrow them further into those with tailwinds from monetary and fiscal stimulus, after adjusting for the country macro profile and cycle.

New Year, Same Strategy

The market rally at the end of last year, truce of U.S.-China trade war, improvement in manufacturing PMI globally have all confirmed our thesis that global cycle is accelerating again, and it is time for investors to take a risk-on stance. We are accumulating high beta play on portfolio, with close to 100% equity and short yield position as a tactical move. U.S. and German bund 10-year yield is likely to creep higher from here in the next 6-12 months as investors concerned of recession comes down further and the seek for yield continues.

We also become increasingly bearish toward U.S. equity, as recent rally has made it even more expensive relative to the world. We think investors have baked in excessive expectation on the earnings growth of U.S. technology companies and headwinds from regulations on data ownership, anti-competitive acquisition and consumer protection will limit the capability of incumbents to monetize their users’ data. As highlighted by the GDPR effects to research firms, banks and brokerage, the risk of stricter regulation and consumer protection rules should not be underestimated.

The dollar weakness of late, which we think is the beginning of the bear cycle ignited by the slowing growth of U.S. economy and tendency for the Fed toward dovish stance on monetary policy, will likely continue as world’s growth pick up and U.S. stabilize this year. It should bode well for EM firms with high amount of dollar debt and those experiencing a recovery from external-driven shock.

Select Country Review

Brazil

Underweight Brazilian equities as valuation is demanding and monetary condition is more likely to tighten from here. The combination of tighter/neutral fiscal policy and tighter monetary policy will put a cap on earnings growth of Brazilian firms. Moreover, the truce in U.S.-China trade war will hurt Brazilian exports of soybean, which accounts for over 4% of Brazilian GDP.

Chile

We have been bullish on Chilean equities, even before the October shock, and are forecasting 35-55% gain of Chilean stocks in this year, 10-20% from earnings growth due to increasing copper prices and 25-35% from normalization of valuation multiples. Currently Chilean stocks are trading at a historically depressed level and has not reflected the rally in copper prices and easing of monetary condition.

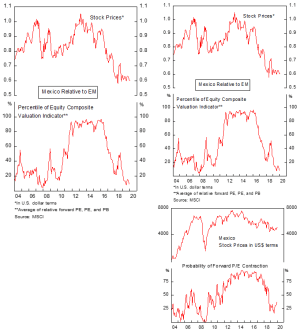

Mexico

Our thesis on Mexican equity has played nicely as the market rallied 20% from its bottom in August 2019. We still see significant upside and would buy on weakness. Our base assumption for this market is 25-35% gain this year, 5-10% from EPS growth and around 20% from valuation multiples increase.

Turkey

The market is on a bring of a breakdown to the upside and we are expecting 45-50% gain from Turkish equity, 22% from earnings growth and 25% from valuation multiples increase. Majority of the macro data has also rebounded strongly in the past year: economic confidence index and retail sales have all show signs of life.

Russia

The energy sector margin has been undergoing a normalization phase last year, causing the massive outperformance of Russian equity above historical correlation with oil prices. We are expecting 30-35% gain from Russian equity this year, even after a strong 2019 rally, driven by 14-18% EPS growth and 10-20% valuation expansion.

Copyright © 2020, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.