Download PDF: Visegrad Country Research

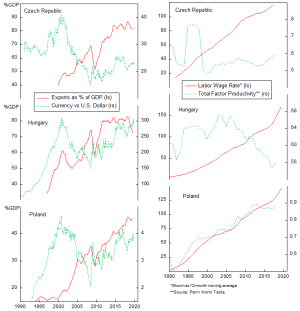

Visegrad countries growth post-Soviet collapse has been impressive, averaging 4% for Poland and 2.5% for Hungary and Czech Republic, compared to 1.5% for Germany. Exports as % of each country GDP has more than doubled in the last two decades (page 13). Faster growth has narrowed the GDP per capita gap significantly (page 4, top left), and further convergence from currently still low level is likely. There are several tailwinds that have accelerated this development and will continue to benefit the growth profile going forward, primarily coming from the countries’ structural condition, fiscal and monetary policies, and allocation from EU funds to less developed region within the area.

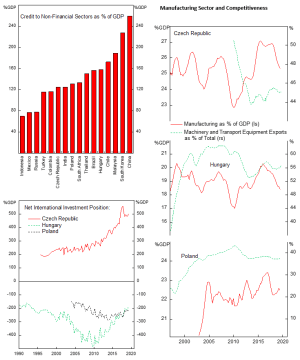

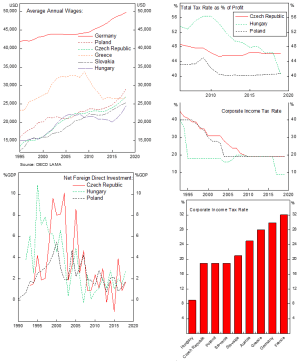

- Cheaper labor cost and lower tax rate than European average bode well for Visegrad countries’ manufacturing sector (page 15).

- Hungary has the cheapest labor cost and lowest tax rate. Hungarian government decision to cut corporate tax rate to 8%, the lowest across European countries, is likely to drive the shift of manufacturing base from countries with higher labor cost and tax rate. However, aging population and impediments on immigration might eventually push wages higher; unemployment rate is currently at two decades low (page 12, bottom left).

- The forint has weakened the most compared to the koruna and zloty, depressing the cost in common currency terms. Hungarian average wages are half of Germany and 20% less in common currency terms than Poland, marking it as a prime destination for European manufacturing base.

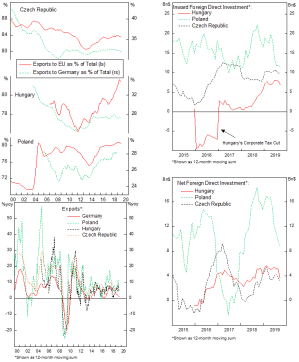

- Significant integration to German and EU manufacturing sector ties Visegrad countries’ growth to the health of the rest of Europe (page 16, bottom left). 80% of Visegrad countries’ export are destined to EU and 30% of it going to Germany. However, despite the weakness of German manufacturing sector, exports growth from Czech, Hungary and Poland are still quite strong.

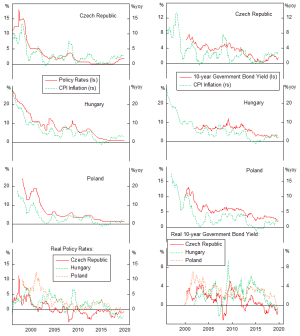

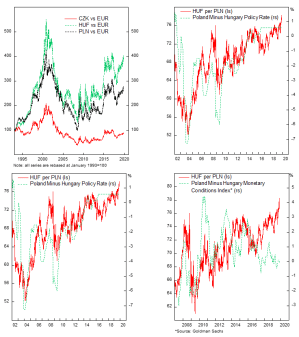

- Monetary policy has been kept on the looser side to avoid strengthening local currency that will erode the export competitiveness relative to other European countries. With negative real policy rates (page 5), floating and cheap currencies, ease of access to credit, investor-friendly policies and government stability, Visegrad countries’ cost of capital is likely lower than other European countries. Meanwhile, the weaknesses in local currencies relative to EUR, combined with high share of exports revenue invoiced in EUR, translates to widening margin.

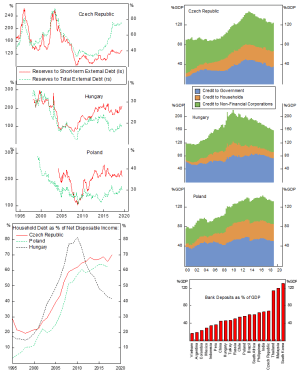

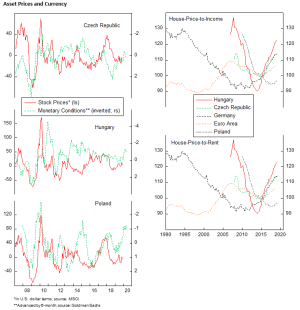

- Interest burden for corporations in Visegrad countries, below 8% of income, is low (page 10). The contagion from low interest rates policy in Europe increase the feasibility of project and encourage investments in the region. The easy access to credit, however, may risk asset prices bubble. Price-to-income and price-to-rent of housing in Czech Republic, Hungary and Poland have been climbing significantly after bottoming in 2015.

- Despite loose monetary policy, there are few signs of excesses in household and corporate leverage. Household debt as % of disposable income ratio has been relatively flat (page 9 and 18), and even declining in Hungary despite the steep increase in house price, highlighting the relatively healthier household leverage condition and lower risk of consumer debt bubble. Meanwhile, bank’s non-performing loans is below 4% and capital has been markedly above those recommended by Basel III.

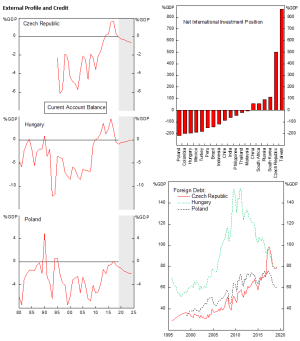

- In October 2019, European Court of Justice ruled that mortgages denominated in CHF could be converted into Polish zloty, at the expense of lender. Since the accession to EU in 2004, around 700.000 households in Poland, one out of five mortgagers, have been taking out mortgages denominated in foreign currency due to its lower rates. However, the weaknesses of local currency relative to Swiss franc and the decision by SNB to remove the currency cap have more than doubled the mortgage value for household. All this bode negatively on Polish banking sector.

- Hungary experienced similar clean up earlier in 2011, which sent banks’ NPL to 16%. However, this cleanup allows the rapid house price recovery in the last decade, compared to sluggish recovery in Poland. Hungary’s share of foreign debt denominated in foreign currency has declined from 85% at the peak to currently 70% (page 19).

- Government fiscal policy could be loosened if growth deteriorates significantly. Czech, Hungary and Poland have a sound fiscal policy (page 6). Czech Republic and Poland have a relatively low public debt (page 7), which allow the government to boost fiscal spending when necessary without breaching the medium-term budgetary objective (MTO) rules set by EU, financed by cheap issuance of bonds.

- EU member state are obliged to MTO of not exceeding a structural deficit of 1% of GDP for countries with debt-to-GDP ratio below 60% and 0.5% of GDP for countries with debt-to-GDP above 60%. Bottom line is that Hungary and Poland have low room for fiscal manoeuvre due to its relatively high debt-to-GDP ratio and/or current fiscal condition compared to Czech Republic (page 7, bottom left).

- All three countries have and are likely to continue to benefit from EU development fund in the coming years. There are six funds with the focus to boost the development of “less developed” region within the EU. The three main large funds, namely European Regional Development Fund (ERDF), European Social Fund (ESF), and Cohesion Fund (CF) cover over 80% of the total disbursement. ERDF focuses on research and innovation, enhancing SME competitiveness, infrastructure building and technology. ESF focuses on employment, education, training and social inclusion. Meanwhile, CF focuses on building network infrastructures in transport and energy and environmental protection. (https://cohesiondata.ec.europa.eu/overview)

- Poland has been the greatest recipient of the funds, totaling € 86 billion or 18% of GDP for the period 2014-2020 as most of its region is still classified as “less developed” (page 4). All these have helped Visegrad countries to build their capital stocks and enhance productivity of its labor (page 12).

- Although the budgeted amount in the 2021-2027 budget is slightly lower than 2014-2020 budget, the figure is still highly significant at 14.3%, 14.1% and 9.2% of GDP for Hungary, Poland and Czech Republic, respectively over eight years period (page 4, bottom left).

Investment Recommendation:

- Long HUF, short CZK (page 19-21)

- Hungary low tax rate and cheaper labor cost will continue to attract strong FDI flow relative to Poland

- Recent CZK strength relative to HUF will benefit the competitiveness of Hungarian export. Czech Republic is also a more open economy, signified by the relatively higher exports as % of GDP, than Hungary, and the slump in German manufacturing sector is likely to have more negative impact toward the country.

- Fiscal impulse is weakening in Czech Republic, whereas Hungary is flat. Also, EU funds allocated to Hungary is more than 50% higher than to Czech Republic in terms of GDP

Growth

Monetary Policy

Fiscal Policy and Public Debt

Copyright © 2019, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.