Download PDF: Russia_Country_Research

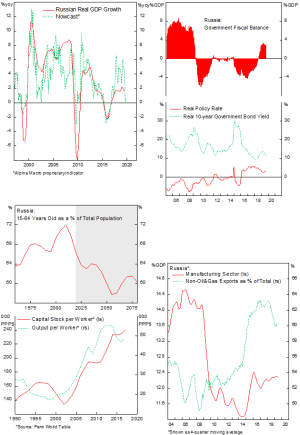

Russia’s growth rate has experienced a dramatic slowdown since the Global Financial Crisis. Domestic imbalances, correction in oil prices and sanctions imposed by the U.S. in 2014 have all contributed to the slack. Since, Russian government has been trying to fix its budget imbalance, reducing reliance on imports and building economic war chest. Yet, its domestic economy is still weak and growth rate has yet reached pre-2014 level.

Going forward, there are several tailwinds that are likely accelerate Russian economic growth in the coming years, which should bode well for Russian assets and the ruble. First, the government is enacting a supply-side reform to boost investment and create employment, focusing on infrastructure, healthcare and education projects. Second, monetary policy is likely to err on the looser side as inflation rate slows further, a marked reversal after years of tight policy aimed at maintaining domestic stability resulting from sanctions and ruble depreciation. Third, the impact of sanctions has largely materialized on the economy and the country is increasingly becoming self-reliant in as a result.

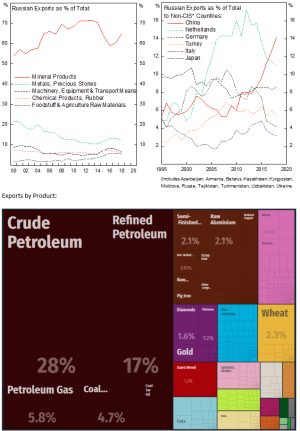

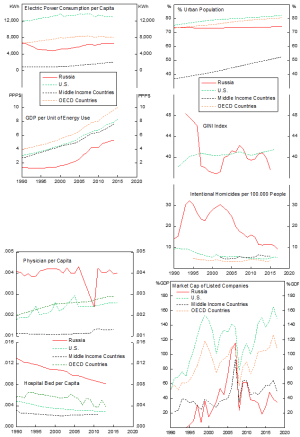

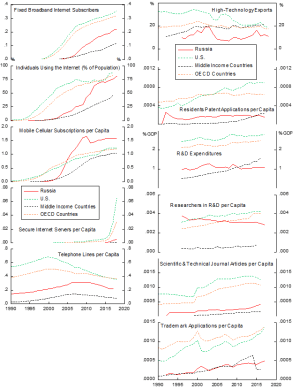

On the structural side, Russia has emerged from one of the riskiest EM countries into one with significant buffer against external risk, after being isolated by sanctions in 2014. Although the demographic factor is not supportive for growth (labor as a share of the population is past its peak), it forces companies to do massive capital investment to boost productivity. The economy is still heavily reliant on oil and gas exports, making it prone to fluctuation in global cycle, and hardly diversifies outside natural resources; manufacturing sector as a share of Russian GDP has stayed flat in the past decades. However, realizing the need to diversify from oil revenue, the government is trying to boost export-oriented manufacturing and agroindustrial sector.

Cyclical Upturn in the Making

Fiscal and monetary policy are both going into easier direction, and there are ample room to stimulate significantly from both sides.

- Russian government has announced $390 billion (25% GDP) infrastructure project for the coming 5 years and President Putin is eager to accelerate its implementation (Box). By the end of 2018, $89 billion has been earmarked in the federal budget until 2021. Currently 13 national projects have been in operation, focusing on infrastructure, health and education sector. President Putin has met few times with Prime Minister Medvedev to follow up on the project and asked him to be personally involved in tracking the progress. However, the implementation of such projects has historically (2007 and 2012) been fraught with failure and confidence in the government execution ability remains low.

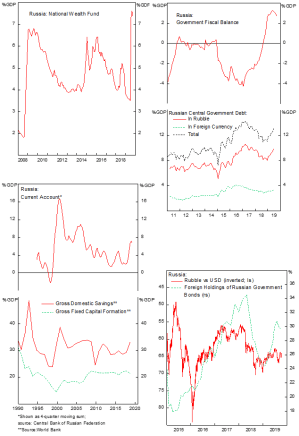

- The liquid assets part of Russian National Welfare Fund (NWF), at 5.7% of GDP, almost reached its 7% of GDP limit, through oil revenue contribution when Urals crude is above $41.6 per barrel. Any amount in excess of the limit could be used by the government to invest in assets with higher return such as government infrastructure projects. It is estimated that with current oil prices, the liquid part of Russian NWF will be above the 7% limit by the end of 2019, leaving $28 billion (1.8% GDP) in 2020 and $65 billion (4.2% GDP) in 2021 to spend on various government initiatives.

- Russian government has also completed a reform on pension spending in 2018, which raised the retirement ages gradually to 65 for men and 60 for women by 2028, allowing a more productive spending to in the economy. VAT revenues has also been increased from 18% to 20%, equivalent to 0.5% GDP, to partially offset the increase in government spending.

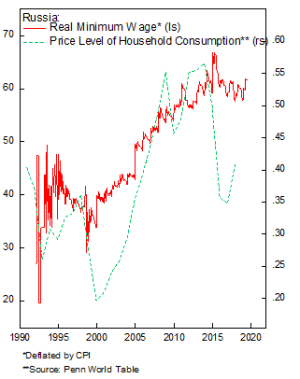

- The ruble has strengthened significantly this year and is among the most favored currencies in the EM space among investors. High equity and bond yields, lower than average external risk and above breakeven oil prices have driven inflow into Russian assets. Meanwhile, inflation rate is now at 4% central bank’s target and is likely to come down further due to the slack in production capacity. All these allow Russian central bank to cut rates by 75 bps this year, a trend we expect to continue.

Balancing the Imbalances

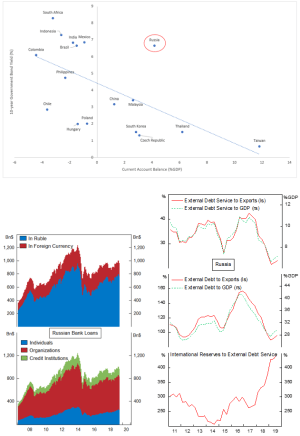

Although the country has not been diversifying from its natural resource dependency, Russia has been transformed from one of the riskiest Emerging Markets countries in late 90’s into one with the most conservative external profile.

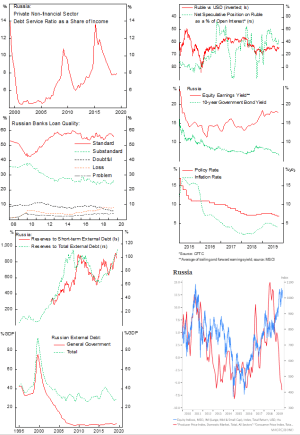

- After 5 years of being in sanction, domestic Russian firms have largely adapted to the sanctions imposed and is now using MIR, its own payment system, to circumvent the restriction from transaction and settlement in U.S. dollar. Russia has been trying to reduce its dependence on Western system and higher amount of new borrowing has been mainly conducted in ruble, reducing the share of foreign currency borrowing in the banking system. This is in contrary of the environment in late 90’s, when marked depreciation of the ruble made it impossible for firms to service their foreign currency borrowings.

- Large international reserves and low foreign-currency denominated debt put Russia among the top of EM countries to weather volatilities and external shocks. By running huge current account surplus, Russia has eliminated the need to short-term financing. In 1998, Russian international reserves were covering only 13% of its total external debt, in contrast with 113% currently.

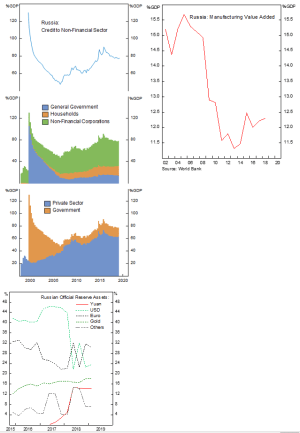

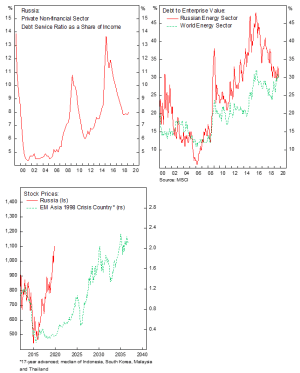

- Government and corporates have been on a deleveraging effort since the sanction, reducing interest burden and giving ample room for earnings to contract before it runs into trouble. In fact, interest burden as a share of corporate income has fallen to 8% from 14% in 2015.

- Banking sector’s health has been improving in the last 5 years as a result of the clean-up on bad banks by the Central Bank of Russian Federation. The number of banks has been greatly reduced from 1058 in 2010 to 484, by consolidating weaker banks or revoking their charter, in order to reduce those with poor governance. As the domestic economy improves and adapt to Western sanctions, non-performing loan has been falling to 8.4% from 17% in 2015 and bad loans have been adequately provisioned.

- The government has been trying to encourage private sector activities, as highlighted by the fall in state employment and consumption since late 90’s, but 2014 sanctions have put pressure on private sector activities and reduce their share in the economy. Moreover, as drafted in the 2024 strategic objectives, the government has been focusing on the development of export-oriented businesses in the manufacturing and agroindustrial sector, which may allow Russia to diversify its exports products.

Takeaways on Russian assets

- Russian equity is massively discounted relative to EM benchmark and trade below its book value. Energy firms, comprising over 60% of the MSCI benchmark, are more profitable than its EM counterparts and trading at a heavily discounted valuation. Moreover, leverage of Russian energy firms has come down significantly since the 2014 oil price correction, which should reduce the risk premium required to hold its stocks. However, the declining PPI inflation is concerning for listed non-oil firms, as margin of manufacturing firms are likely to be squeezed in the near term.

- In real terms, Russian government bonds offer attractive risk-return. The country run twin-surplus and government debt level is low at 12% of GDP, mainly denominated in local currency. The combination of lower inflation and external risk is likely to push down Russian local-currency government bond yields further. (Long Russian government bond?)

- The ruble is expensive, according to our fair value model, and terms of trade has been deteriorating. Recent outperformance of the ruble has been mainly due to the tight monetary policy by the central bank and foreign inflow into Russian government bonds, as the government is running responsible fiscal policy and has a very low debt level. The shift in focus toward driving growth, however, is likely to limit the upside of Ruble from current level.

| National Goals and Strategic Objectives of the Russian Federation through to 2024

In order to achieve breakthroughs in science and technology and socioeconomic development in the Russian Federation, increase the country’s population, improve the living standards and conditions of our citizens, and create an environment and opportunities for all to fulfil their potential, the President has instructed the Government to achieve the following national development goals by 2024: a) ensure sustainable natural population growth; b) increase life expectancy to 78 years (80 years by 2030); c) ensure sustainable growth of real wages, as well as the growth of pensions above inflation level; d) cut poverty in half; e) improve housing conditions for at least 5 million households annually; f) accelerate technological development and increase the number of organisations engaged in technological innovation to 50 percent of the total; g) speed up the introduction of digital technologies in the economy and the social sphere; h) take Russia into the top five largest economies, ensure economic growth rates exceeding international rates, while at the same time maintaining macroeconomic stability, including inflation under 4 percent; i) support high-productivity export-oriented businesses in the basic sectors of the economy, primarily, in manufacturing and the agroindustrial complex, based on modern technology and staffed with highly qualified employees. |

| Russian Manufacturing Industry

Russian manufacturing sector could be classified into the building of machinery and metallurgy products. The former includes aerospace production, weapons and military machinery, electrical engineering, pulp and paper, and automotive for road and agricultural machinery. Metallurgy complex of Russia includes the extraction of metal ores, their enrichment, metal smelting, production of roll stock. This industry includes ferrous and nonferrous metallurgy, with the former comprising 90% of the products.

|

Effects from Russian Sanctions vs Previous EM Crisis

Russia’s Structural Outlook

Before 2014, Russian real policy rates were often zero or negative, incentivizing many firms to do binge borrowing to sometimes finance dubious projects. This loose monetary policy has resulted in the ruble depreciating over time and creates excesses in the banking system, which made the financial system prone to external shocks. The double whammy from 2014 oil price collapse and sanctions, however, serve as a wake up call for both the government and central bank to get its policy in order and to put a more stringent regulation on the banking system.

- Positive policy rate, which has made borrowing more costly for firms, and the crackdown on the banking system since the appointment of conservative central bank governor in 2013, have led to contraction of credit to Russian corporations and halving of the number of banks. And despite the 100-bps cut this year, over the backdrop of falling inflation and weak domestic growth, policy rate is still tilting toward tighter bias, giving room for the central bank to ease further and boost growth in the medium-term.

- On the fiscal front, Russian government has also turned toward a more responsible fiscal management, as highlighted by the more realistic assumption regarding the breakeven oil price needed to balance its fiscal. The government has also shifted its spending from social security towards more productive infrastructure, health care and education spending, in the form of the 25% GDP national projects. Moreover, given the greying population, government’s success in completing the pension reform last year has also put government fiscal sustainability in check, reducing the risk of bloated fiscal deficit during period of low oil prices.

Corporate leverage has come down significantly post-2014. The impact of falling oil prices, depreciating rubble and sanctions have put Russian energy firm in a precarious position to find external financing, which lead to a mass deleveraging of corporates’ balance sheet. As a result, debt as a share of enterprise value fell from its peak at 48% toward 30% and is now on an equal footing with the world’s, while corporate interest burden as a share of income halved during the same period. This gives more room for Russian firms to weather the shock from falling revenue related to decline in oil prices.

On the risk side, Russia has barely diversified from its dependency on energy sector. This put Russian growth at the mercy of international oil prices and global cycle, which lead to a high beta market. It is also difficult for productivity of the country to rise, as it requires labor reallocation of labor from low productivity sector into higher one, such as from agriculture to manufacturing. In Russia case, investment and employment have mainly been concentrated in the oil and gas sector due to the higher profitability of the sector, which in turn, further reduces the incentive to invest in human capital and manufacturing sector.

Russian Domestic Resilience

- Rationing and shortages during Soviet Union era leaves Russian household more resilient toward shocks. Employees are more willing to take real wage cut, providing flexibility for businesses to manage its cost during downturns.

- Russia is self-sufficient and a large net exporter of few basic food commodities such as grain and corn, reducing the transmission between weaker ruble and higher food prices. Moreover, household consumption price level also sees a significant drop as Russian adapt and alter their consumptions pattern.

- Lower household debt level compared to other EM countries insulate Russian households from shock in the credit market. Meanwhile, the weaker ruble increases Russian competitiveness in the export market.

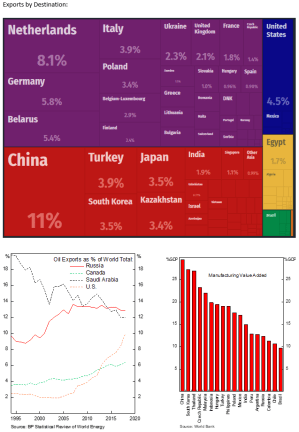

Russian Role in World Energy Sector

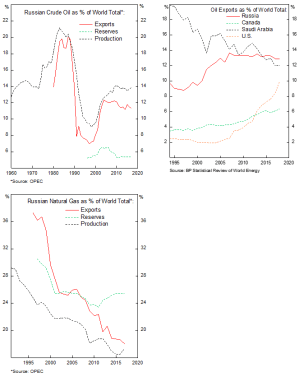

Russia is a major player in world’s energy sector, contributing 13% of world’s oil demand and 18% of its natural gas demand. Russian supply of energy is especially important to European Union countries, who imports 30% and 39% of its total demand of oil and natural gas from Russia. The dependence is even higher for Central European countries, with some countries importing over 75% of its total energy demand from Russia. As a result, EU countries are on a precarious position in choosing between supporting other European countries, such as Ukraine, and securing its energy supply. The going through of NordStream 2 pipeline project, despite heavy criticism from the U.S., highlighted the lack of economically feasible alternatives for European countries in diversifying its supply.

Russia is also expanding its client base toward Asian countries, especially China. The two countries have agreed to establish joint ventures to develop an Arctic natural gas facility and trade of 1.3 trillion m3 gas through the Siberian pipeline (see link below). The closer ties between Russia and China and their close geography mean Russia is likely to supply greater share of Chinese energy demand going forward, benefitting Russian energy firms. The Arctic offshore oil resources are also becoming strategically important for Russia, as melting ice cap allows shipping through the Northern Sea to reach Asian market. However, the progress is hampered by the sanction imposed in 2014, restricting deepwater oil technology, equipment and expertise from the West to develop the Arctic projects.

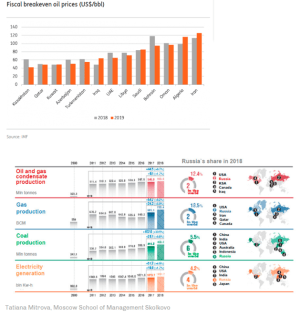

Russia, compared to other oil producing countries, needs a relatively lower oil price to balance its budget. This allows Russia to grab market share when oil price decline, as they could afford lower oil prices and restrain from cutting production for longer period compared to Saudi Arabia that needs $80 per barrel oil to balance its budget. Moreover, the assumption of Russian government breakeven oil price is also getting more conservative. In 2014, Russian government state budget was balanced at oil price of $100, a contrast to current low $40 breakeven price. This put government fiscal profile at a much more (or even too) conservative and sustainable path.

Copyright © 2019, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.