Download PDF: Market Timing Strategy of Emerging Markets Portfolio

Despite the recent volatility from the trade war and deterioration in global growth, from a valuation perspective, however, EM stocks remain cheap compared to its historical averages and relative to DM equities. Since around 2012, as the earnings generation capability of EM stocks declined, investors have mostly shunned away from EM equity and drove multiples significantly lower. We argue that the increasingly similar characteristics between EM and DM countries will eventually result in the convergence of their equity multiples. Currently, relative to DM equity, EM stock has a ROE of 0.95x (5% discount) and P/B value of 0.68x (32% discount).

Bottom line is that there is a structural case to be made for long EM equities. Cyclically, the current rally is still at its early phase and has plenty of room to run.

- Buy-and-Hold vs Tactical Strategy in EM Investment

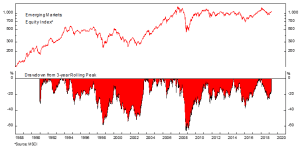

In the last 23 years, buy-and-hold investors have gained dismal return from investing in Emerging Markets equity. EEM ETF, a proxy for actual price return investors received by investing in EM equity, returned only 128.9% (3.67% annualized) since March 1996. Investing in EM stocks also entail a great risk with the market suffering from a major market decline (>20%) every 3 years due to various reasons; Fed tightening, dollar strength and Chinese stop-and-go cycle are common cause.

However, it does not mean that investors should shy away from EM equities altogether. Performance of investing in EM equity could be greatly enhanced by various market timing strategies, in terms of both risk and return. Fundamentally, watching the turn of Chinese business cycle is one important input in getting the timing right. The challenge for investors is to build a reliable signal to know when to get in and out of EM stocks, as the depth of EM correction could be very deep, and the rebound process usually happens sharply. In the following section, we proposed two simple strategy that has worked well in EM equities.

- Two Simple Market Timing Strategy for Investing in EM Stocks

The strategy proposed is based on two facts on the market: 1) declining equity prices and increasing VIX goes together, with the later has a mean-reversion tendency and acts as investors’ sentiment toward the market and 2) EM stock prices move in trend due to herding behavior.

Contrary to decreasing VIX level in an uptrend or flat market, period of downturn is always preceded by a spike in VIX above its moving average. Hence, a market peak will be accompanied by lower VIX than its moving average and a market bottom will be accompanied by a high level of VIX reversing to its mean. Intuitively, this strategy works effectively because a sell signal will always be generated on the day the market has a major correction, limiting investors losses only to the initial dip. Meanwhile, a buy signal will be generated when the market bottoms and about to resume its upward movement, limiting the “missed” opportunity of market rebound. The drawback of the VIX-based strategy occurs during a very long period of low volatility when there would be many false signals due to depressed level of its moving averages.

The second strategy is based on crossover between prices and its moving averages. The strategy works very well in highly volatile markets such as EM equity and less well in relatively calm market. This is because, similar to the VIX-based strategy, the moving average will tend to converge toward the current price level in a long period of calm market, creating many false signals to investors.

The back testing below is based on EEM ETF as the benchmark and assumes 0.3% transaction cost. After a signal is generated at the end of the day, investors are assumed to be able to purchase the security at the closing price.

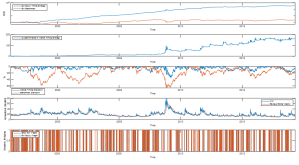

- Aggressive tactical asset allocation (VIX-based strategy)

Buy signal is generated when VIX is below its 59-day moving average and sell signal is generated when VIX is above its 59-day moving average. The determination of number of days for the moving average is explored further in the next section. Maximum drawdown is reduced to 34% compared to 65% for EM benchmark, while return is magnified to 29.34% annually compared to 3.67% for a buy-and-hold strategy. Turnover of the strategy (number of transactions divided by total number of trading days) is at 10.5%.

- Moderate tactical asset allocation (Moving average strategy)

Buy signal is generated when price is above its 102-day moving average and sell signal is generated when price is below its 102-day moving average. The determination of number of days for the moving average is explored further in the next section. Maximum drawdown is reduced to 16.8%, while return is magnified to 12.4% annually compared to 3.67% for a buy-and-hold strategy. Turnover of the strategy (number of transactions divided by total number of trading days) is at 2.2%

Simulation of Parameter

The determination of number of days in the moving average is based on optimization between return, number of transaction and maximum drawdown of the strategy. The chart below shows the result of various moving average strategy; annualized return includes 0.3% fee for every transaction.

- Strategy Performance Across Equity Markets and Trade Implementation

The strategy was tested across 40 country equity indexes in both DM and DM, using 134-day parameter for the VIX-based strategy and 107-day for the moving average strategy. Results are shown in the table below. It shows that the VIX-based strategy works consistently in 27 out of 40 countries (67.5%) while the moving average strategy only works in 15 out of 40 countries (37.5%). The term “works consistently” means that the strategy creates an alpha in majority of the period, with outperformance of the strategy increasing in a stable way. In countries where the strategy does not work consistently, it is not necessarily that the strategy underperforms buy-and-hold strategy, but rather there are brief period of overperformance followed by long period of underperformance. If investors only care about the outperformance of the strategy regardless of the consistency, between 1996 to April 2019, the VIX-based strategy works in 36 markets (90%) and the moving average strategy works in 29 markets (72.5%).

The VIX-based strategy seems to work more universally as higher volatility from the U.S. market often reverberate to all other market as well, hence the usefulness of U.S. market volatility in predicting other DM and EM markets direction. Meanwhile, the moving average strategy does not work well in trendless and choppy markets; take an example of South African equity (in U.S. dollar terms) that trade in a flat range between 2010 and 2015.

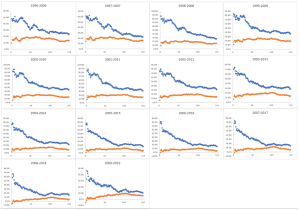

Quants might question the robustness of optimized parameters to forecast out-of-sample data; for example, whether the x-day moving average is an optimal result for different time period. The scatterplot below shows the result of both strategy with a rolling back testing period, where we could see that the strategy produces similar pattern of results in varying time period and the “optimum” number of days for moving average signal tend to be clustered in the same area.

Attached to this file is the result of these two strategies applied in 40 different indexes (Market Timing Strategy)

Kevin Yulianto, CAIA, PFM

Chief Investment Officer

Copyright © 2019, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.