Download PDF: Monthly_201907

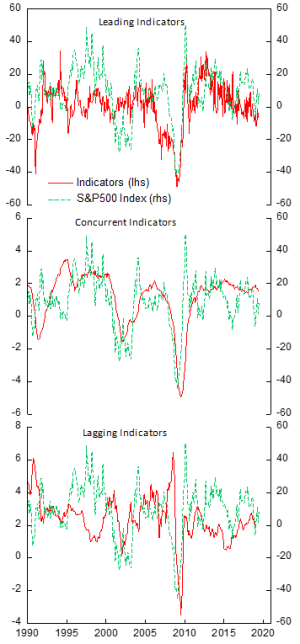

“For months investors have been concerned about potential recession in the U.S., yet the stock market is at all time high. How could we reconcile these developments?”, asked one my friend who is working at an asset management company. The effects from reflationary effort from China has yet to be seen and the U.S. economy is slowing down, a dangerous combination for global equities. The expectation of Fed rate cut, however, has boosted U.S equity to record level as the cost of capital overshadow the decline in corporate earnings growth outlook (toward 0% growth).

In the meantime, global manufacturing PMI has yet to find a bottom and emerging markets’ PMI has been relapsing after a brief period of strength in the first quarter this year. Moreover, the risk of Fed policy mistake should not be understated. Much of these, except the later, has been discounted in the market and that leave the market direction to the battle between earnings outlook and stimulus effort from fiscal and monetary policy.

Currently, I’m seeing a greater downside risk and limited upside in global equity markets, especially in the U.S. as valuation has been significantly higher than European and EM counterparts. From a contrarian point of view, long world equities ex-US and short US stocks.

Rather than concluding myself in either “recession” or “reflation” camp, I would rather point out several factors that will set the direction of global equities and adjust portfolio allocation according to its development.

- Global trade and manufacturing output. De-escalation of trade war rhetoric and South Korean exports figure are important indicators to watch. The later is still very weak in June.

- Monetary policy in U.S, Euro Area and China. Steepening of UST yield curve and accelerating Chinese M1 growth would be an encouraging sign. Both are giving inconclusive signal with a bias toward the upside (steepening and accelerating growth in money supply) as Fed has announced its intention to ease and Chinese government stimulus lagged effect should be felt in the second half of the year.

- Capital spending and government fiscal stimulus. Rise in copper price above 6300 USD/MT and other commodity prices would signal a firm rebound in global demand.

But what is the market saying?

- U.S. economy will stay robust and earnings outlook stays positive while emerging markets outlook is getting better amid reflation effort across EM countries.

- Easing monetary policy will devaluate paper money purchasing power, hence the gold price in fiat money is rising. It also says that global risk has spiked up significantly. It is prudent to hedge part of the portfolio until the global slowdown has bottomed.

- Global demand is still weak amid the slowdown in China reverberating to countries in its supply chain. Stronger easing effort by EM central bank and Chinese fiscal policy will be the impetus for economic recovery.

- Euro economy likely to stay weak relative to U.S. but Canadian and Japanese economy is getting relatively stronger. Again, this proves that the U.S. cycle is behind RoW and it is likely that rest of world equity will outperform U.S.

Portfolio Construction

In constructing our portfolio, we take a more cautious approach, hedging our risky position with a call option on VIX, discussed in the later part of this month piece. Meanwhile, for the equity allocation, we are bottom-fishing countries whose earnings outlook is set to improve and whose valuation is at historically low level. We discuss our equity country allocation separately at the end of the section.

Assuming a US$ 1 million with 95% equity allocation and 5% weight to call option of VIX, we have an overall portfolio that is beta neutral during correction and reduce the drag of hedging if the market rally further. An ATM (X@15) call option on VIX expiring in December 2019 currently trades at $2.95/contract. Assuming 20% equity market correction and VIX spiking to 30, which has been historically the case, the portfolio will be worth:

Equity: 950.000 x (1-20%) = 760.000

VIX: (30-(15+2.95)) x 100 x (50.000/295) = 204.237

Total Portfolio = 964.237 (-3.58%)

While if the market rallies 10% and our 6-months hedge expire worthless, our portfolio would be up 5%. Given the chance to close our hedge early during market correction and use the proceed to buy more equities, we hope to gain from both our hedge and the rebound in equity prices afterward.

What About Currencies?

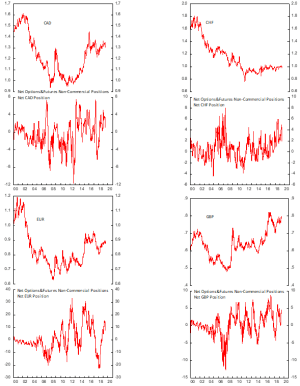

As we are expecting a lower U.S. growth and improving RoW outlook from Chinese and EM reflationary effort, we think U.S. dollar will weaken relative to other G7 and EM currencies, except EUR. Net speculative positioning on CAD and JPY have been turning over and both currencies will likely continue its rally against USD. AUD should also benefit from commodity prices increase and stronger Chinese demand should the reflationary effort works.

We think that the worst is already priced in the currency market and a weaker dollar will reinforce the recovery in global growth. A controlled inflation and weak growth will lead to EM central banks to cut rates, a phase that historically has been positive for EM equities and risk assets in general.

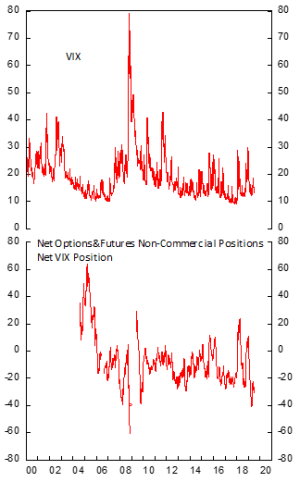

VIX To Go Higher and Is a Better Hedging Tool

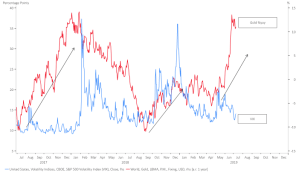

As I`m writing this section, the VIX is trading at 13.1, a relatively low-level this year. As we are generally bearish on the U.S. market, we are we believe holding a small percentage of our portfolio in VIX call option deserves some merit. First, we are trying to immunize our portfolio equity beta to reduce the downside in global equity correction, whatever the cause, for the next 6 months. Second, on its own we believe volatility will march higher, as historically been the case when gold price increase significantly, preceding the jump in volatility (see chart).

At 13, the VIX is not expensive and provides a better hedge than buying S&P500 put option on cost-to-potential-upside ratio. The net speculative position on VIX has been near record negative as well, which is prone to trade unwinding should U.S. corporate earnings undershoot expectation significantly leading to market correction.

Moreover, if our prediction is correct, selling or exercising VIX option during market slump will provide us funds to purchase undervalued equities, acting as a reserve cash position.

Global Equity Views and Country Selection

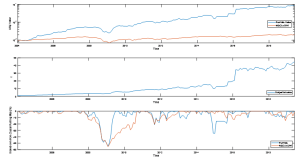

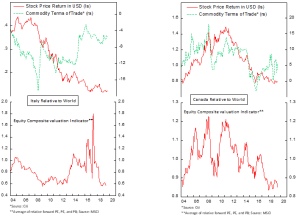

Our country allocation has not differed significantly from last month’s and we are rotating few countries to benefit from an improvement in outlook in Mexico and Italy while dropping Japan from the portfolio. Our quantitative equity allocation model portfolio returned 9.23% in June compared to 6.46% for MSCI ACWI, our benchmark. Meanwhile since its back-testing period starting in January 2004, the model portfolio returned 33.7% annually vs 4.7% for MSCI ACWI.

Our two highest conviction idea since the beginning of the year have panned out very well. Turkish equity has returned 7.7% in the Q2 and our call option position has returned 74%. Meanwhile, our long position on Argentine bank (BBAR) has returned 40.8% due to the improvement of the peso and general macro environment. We continue to advocate long position on these two markets as the risk/reward is still attractive.