Read in PDF: Monthly 201908

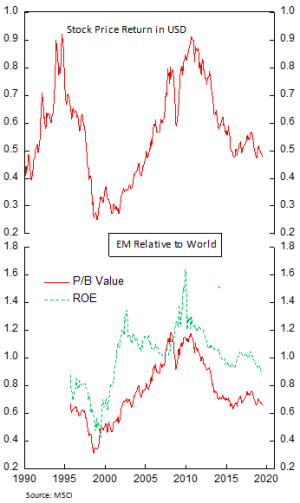

As bond yields continue to stumble globally, we expect that more SWF and pension fund will divert allocation from fixed income to both public and private equity, which would be a boon for the deepening of stock market globally. Holding developed countries’ government bond is a sure way of losing purchasing power, leaving pension fund to search for yields among EM bonds and corporates. It is not unlikely that in the end of the next decade, fixed income would play less than 20% of pension fund assets. Small cap and value stocks, two segments that have underperformed in the last decade, will benefit eventually as the valuation of popular name becomes lofty. European market, benefitting from the trend in consumer staples (Nestle) and healthcare (Novartis, Roche), should also benefit from the rise of middle-income population across the world.

The search for yield will continue and EM will be one among many that will benefit from the cross-border flow. EM equities are currently trading at a discount relative to DM and is grossly underrepresented in the world benchmark. In the next decade, we think the story is about EM countries growth and convergence toward DM standard. Back in the second half of the 90’s EM countries were the source of headache for investors, with sporadic crisis occurring across Latin America, starting with Mexico Tequila crisis, and then Asia in the 1998. In the 2000’s many EM countries start to float their currency, including Argentina, and build their buffer to counter problems in their Balance of Payment, a process that continues in the next decade after the Great Financial Crisis. Inside EM itself, Asian countries with high savings rate have fare much better compared to LatAm countries, whose majority of savings rate are below 18% GDP.

The rise of technology firms after 2010 in the U.S. and the cyclical top of the commodity boom resulted in EM underperforming in the last decade. However, we are seeing a shift in both trends. Increasing scrutiny over data and regulation in the tech sector, both in domestic and cross-border information flow, will put strain on the growth of the giant. The demand for energy and raw materials should also pick up as more people in Latam and Asia join the middle class. Africa, meanwhile, would be in the position most EM countries today were 30 years ago.

Massive Long Position on Turkish Equity

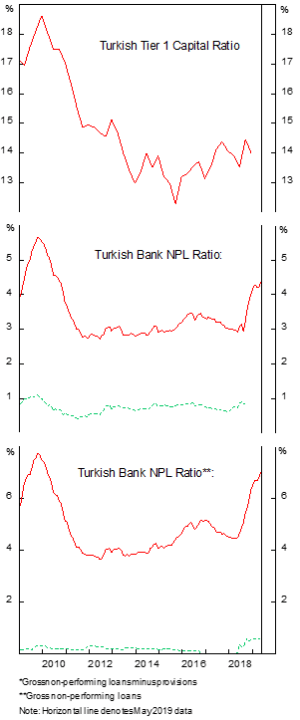

The macro picture in Turkey has improved significantly since late last year. Industrial production stopped contracting and confidence among businesses and consumers have improved. Inflation, probably the most important indicators of the economy, has come down significantly to 15.7% from 25% at the peak last year. However, it does not mean that the country will not suffer from a crisis again in the near term. International reserves have been exceptionally low, covering merely 25% of total external debt and 122% of short-term external debt. Should the world go back into risk aversion mode or Erdogan push for another unfriendly policies, it is likely that lira will depreciate further and trigger another balance of payment crisis among firms with high FX debt, causing the central bank to tighten massively and hurt the economy.

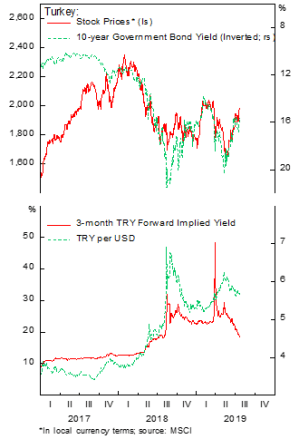

Nevertheless, our base case scenario is for the lira to appreciate to 5.3 TRY/USD level (+7%) over the next year and the equity market to rally on the back of multiple expansion and EPS improvement. Without further sanctions from the U.S. related to the S400 delivery and other external shock, we expect EPS to improve 11% and multiples to expand 24% from current level P/E of 6.9 to 8.6. Taking the lower range of base case estimates, we see unhedged long position in Turkish equity to return 40-45% in the next 12 months. This all despite the equity has rallied 21% from its August 2018 bottom, but still 22% below its recent high. We acknowledged, however, that the risk is also high. A sudden 15% drop in one week cannot be ruled out, as had happened last year.

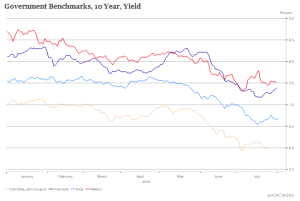

The impact of last year crisis could be visibly seen in the banking sector, which surprisingly has been more resilient compared to previous crisis events. Gross NPL increased to 4.4% in May from 2.9% in August 2018. Most of the default, however, is in those denominated in local currency rather than those in FX. Implied forward yield of Lira has also declined significantly to 18% from its 32% high in August 2018, which is a better proxy rather than the high at end of March that was caused by short selling restriction by the government. Since 2006, inflation in Turkey has averaged 8-10% compared to currently 16%, meaning that local currency Turkish bond is also attractively priced should normalization continues. At the time of this writing, Turkish earnings yield stands at 14.56% while 10-year government bond yield in local currency yields 16.2%. Historically, the two assets have been yielding +/-2% from each other, which support our thesis that earnings multiple will expand to 8.6x trailing P/E (earnings yield of 11.6%).

The ebb and flow of multiple and earnings also tend to go together. Period of declining earnings tend to be accompanied by contracting multiples, vice versa. Hence, in a recovery, investors are likely to benefit from three return source: earnings improvement, multiples expansion and currency appreciation. Earlier last month, we also published a more comprehensive research studying the market response to previous crisis in EM countries, with Turkey being one of them. Conclusion is that inflation serves as a great barometer for the country recovery, with the rebound in equity market going together with lower inflation figure two years after the crisis peaked.

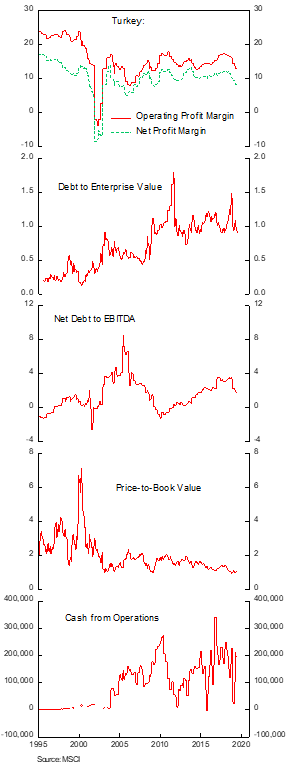

On a more fundamental note, we have seen deterioration in earnings, leverage and valuation late last year that is consistent with previous crisis events, and an improvement in some of these metrics since early this year. Cash flow from operational side has normalized while debt ratios have declined. Currency, after adjusting for inflation, is still trading at an undervalued level, which is an equivalent of easing for the domestic economy.

Bottom line, we like what we are seeing in Turkey domestic economy and favor a long-dated ATM equity call option strategy to access the market, as it limits our downside and serves as a cheap leverage for the fund. On the political front, we are more cautious and will continue monitoring the government policies and intervention in the Central Bank.

Revisiting This Year Thesis

Below is the performance review since the beginning of our monthly post. At the end of the section, we outlined our current most favored market.

December 2018: Overweight Financials and EM

January 2019: Long Turkish, Colombian, Mexican, Japanese equities. Long Mexican, Indian, Indonesian, Colombian government bonds

February 2019: Long Argentine equities

April 2019: Long Brazilian and South African government bonds

May 2019: Long Russian, Japan, South Korea equities

June 2019: Long Spanish, Italy and Canadian equities

Most of our investment thesis holds, but we are trimming those with less conviction to maintain discipline in our portfolio management process and free up capital to be allocated to new, quality ideas.

- Long Argentine Equities, especially the banking sector (BBAR US ADR)

- Long Canadian Equities

- Long Colombian Equities

- Long Italian Equities

- Long Mexican Equities

- Long Spanish Equities

- Long Turkish Equities

- Long U.K. Equities

- Long AUD/USD

- Long VIX as a hedge (details on July publication)