Download PDF: Monthly_2019_April

The strength of the dollar has dismayed many investors, us included. The weakening growth in the U.S., as measured by final demand component of the GDP, has pointed downward and should lead to a weaker dollar at a time when China is reflating. We still believe that the current improvement in Euro area and Emerging Asia will eventually drive their currency stronger and the dollar weaker. However, sentiment also matters in FX trading: current net speculative position of the dollar is extremely net long and continue to grind higher.

There are only two occasions since the 2000 when the net speculative on the dollar peaked and the DXY rose afterward: 2008 and 2014. Our argument is that in 2008, the financial crisis drove investors into safe-haven currencies, including the dollar. Meanwhile, in 2014 the dollar strengthened due to expectation of rising interest rate for the first time in the U.S. post-GFC. Then, the stronger U.S. growth and tighter monetary policy relative to European countries and Japan have kept the dollar strong until synchronized global growth happened in 2017.

The current dollar bull story is driven by many factors: relative stronger growth between the U.S. and Europe, Quantitative Tightening of the Fed balance sheet, last year’s tight Chinese policy and significantly higher yield of U.S. bonds relative to other DM countries. Except for the last one, we see the trend of these factors are reversing and may weigh the dollar later in the second half of the year. For now, our portfolio is still geared toward higher dollar, but going forward we are looking for an entry point to sell the dollar and load up on CAD and JPY. If our forecast turns out to be true, EM assets and currency will be the biggest winner, although the U.S. stock market may also rally.

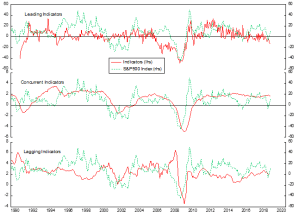

The U.S. economy is showing signs of weaknesses after 10 years of bull market. Our leading indicator, a combination of car sales, housing starts, consumer confidence and PMIs, is showing a downward and contractionary trend. Combined with flattening yield curve and increasing chance of too tight policy mistake by the Fed, we are very nervous about the state of U.S. economy. We think we are in the very end of the cycle and correction is overdue. Implicit behind that view is the bearish bias on the U.S. equity and the world, as declining U.S. market would make it harder for the other markets to rise.

Although it may sound naïve, we think that should the U.S. equity undergo a major correction, other markets would correct by a lesser amount due to an already much cheaper valuation and the lagging cycle in the U.S. compared to China and other DM countries. That is the reason, in this month piece, we have carefully picked our countries selection for our portfolio.

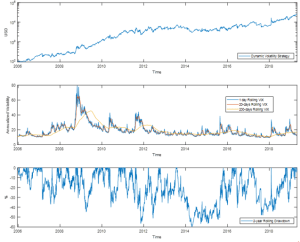

And to hedge our risk, we have been carrying a position in a long-dated VIX call option that we might switch with put option on the SPX in the near term. Thanks to the current low volatility regime (hedge fund bets against VIX is at extremely high level), the cost of hedging is fairly low. Moreover, our Volatility Strategy (VS) would also act as a buffer to our losses in the equity position when major correction happens.

Kevin Yulianto, PFM

Chief Investment Officer

Quick Review on the Quantitative Model Performances

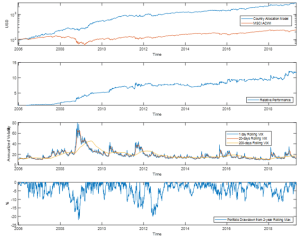

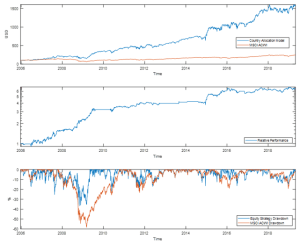

For the month of April 2019, our quantitative models underperform the global benchmark, mainly due to the model country selection. The Global Asset Allocation Strategy (GAAS) model, which reflects the overall quantitative strategy, gained 2.9% while our benchmark (MSCI ACWI) gained 3.4%. Meanwhile, the Global Equity Strategy (GES), which reflects only the country selection, gained 1.8%. The Volatility Strategy (VS) drives most of the upside of the quantitative model performance, gaining 13.4% for the month, as volatility headed lower for most of the trading days.

Our Global Equity Strategy (GES) model still favors Brazilian and Mexican equities for the month of May, while also flirting with the recommendation of long South African equity. Qualitative discussion on these countries is outlined in the next section.

Figure 2.1 Global Asset Allocation Strategy (GAAS) Model Performance

Figure 2.2 Global Equity Strategy (GES) Model Performance

Figure 2.3 Volatility Strategy (VS) Model Performance

Qualitative Screening on Countries Equity Valuation:

Brazil, Canada, Germany, UK, Japan, Korea, Mexico, Russia, Turkey and US

From a cycle point of view, Brazilian equity is in a tough spot. We expect the economy to decelerate in the near-term and uncertainties from the pension reform bill, including spats between Bolsonaro’s family and politicians, are weighing down our assessment on the country. Although our quantitative model is recommending a long position in the equity, we are overruling this decision and stay put right now as we believe there will be a better entry point to buy the market.

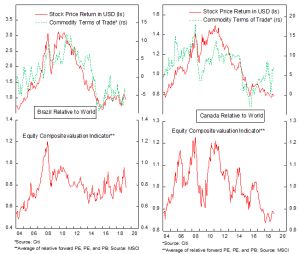

Canadian equities have been lagging its world counterparts even as oil prices rallied. The manufacturing sector is showing a deceleration since the second quarter last year and has not shown an improvement so far. The slowing growth in the U.S. will be a drag on Canada and although we think the currency is cheap, we believe the relative growth profile is still more attractive for the U.S., which should drive the USDCAD pair higher. Moreover, flatter curve, weakening manufacturing activity and the drop in excessive property prices in major cities will be negative for the Canadian banking sector, which accounts for almost 40% of the index.

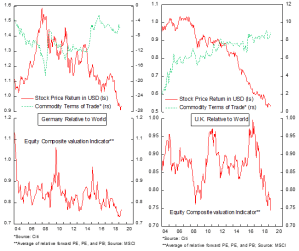

German manufacturing sector PMI has been declining in almost a straight-line manner since January 2018 along with the stock market relative performance to world equity, dragged by the policy tightening in China and weakening growth across the Euro area. However, we think that cycle is making a bottom and equities will further rally going forward. Should the outlook for Chinese reflation continue, as we expect, German bourse might be the greatest beneficiary among developed market countries.

British equity has been massively lagging the world since its peak before the 2008 GFC and the condition is worsened by Brexit just as the outlook started to improve back in 2016. The fear of a hard Brexit and exodus of firms leaving Britain to European countries have driven the multiples into level not seen since the GFC. We are seeing a deep value firms across British equities and believe the economy will continue its expansion after the cyclical bottom in October 2018.

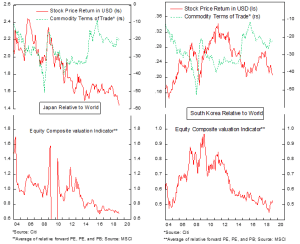

Japan’s manufacturing sector shows an improvement in April as Chinese reflation continues to take effects on neighboring countries in its supply chain (Korea, Taiwan and Japan). The country’s terms of trade are improving, and it looks like Japanese economy is making a cyclical bottom last February. With these cyclical factors in mind and cheap currency, we are trying to be more positive on Japanese equities, despite the prospective increase in VAT rate later this year.

South Korean firms are known for its conglomeration and poor governance, which most investors think justify the low multiples of the equity market. However, we believe the market will be re-rated in the medium term as its earnings improve after the recent huge drop. On the economic side, manufacturing activity bottoms in last February and has been rebounding sharply in the last two months as Chinese import demand has been stronger.

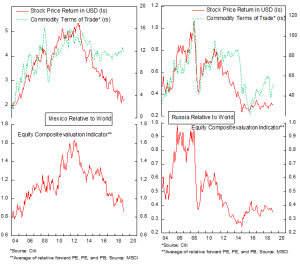

After recording a contraction in Q1, we expect Mexican economy to recover later this year. Several indicators are already showing early signs of improvement: industrial production, manufacturing business confidence and retail trade. Exports and imports, however, are still contracting on a year-on-year basis and domestic demand is still fairly weak. On itself, currently we like Mexican equities but are uncertain whether it will outperform the world equities at this point. For now, we stay put on the quantitative model’s assessment.

Our view for Russia is tied to our view on oil: increase in oil price has historically coincide with the outperformance of Russian energy sector relative to world and U.S. energy sector. Russian equities have always been cheap and round of sanctions on Russia has kept multiples stay low. We are seeing a broader recovery in the economy, especially in the second half of 2018, that will boost Russian equity’s earnings. Meanwhile, inflation is expected to remain anchored at 5% +/-1% and exports start to improve alongside increase in oil price. We believe the market has limited downside from current level and investors should focus on the volatility of Rubble when investing in this market.

Despite still contracting, Turkish economic activity has improved somewhat, as indicated by the manufacturing PMI figure that currently stands at 46.8, 4.1 points better than its through in September last year. Banking sector NPL number is not showing signs of catastrophic stresses either: gross non-performing loans have been declining since March and Capital Adequacy Ratio (CAR) is at a healthy 16.4% in March. Cheaper TRY should give a boost to Turkish manufacturing goods exports and create a feedback loop to a stronger economy. Currently, most of investors’ concern lies in the declining reserves and Erdogan’s action regarding the result of regional election in Istanbul and Ankara, where his party lost. Despite these risks, we believe Turkish equity is a deep value play and will advance in the next 12 months regardless of the political outcome. However, we will continue to monitor the central bank’s reserve data to spot potential crisis brewing in the horizon.

U.S. economy has been stronger than most expect, and April’s manufacturing PMI data is showing an uptick to 52.6 from last month’s 52.4 figure. This may prove to be a short-term cyclical bottom in U.S. economy, like those in the third quarter of 2017. If this is the case, then U.S. equity will rally further as the expansion continues. However, we are uncomfortable with the high multiple U.S. equity is trading at, despite knowing that the FAANG stocks are driving tit upward. For now, we tend to avoid broad allocation to U.S. equity and prefer to go for a bottom-up approach when we saw value in some names.

What About EM Bonds?

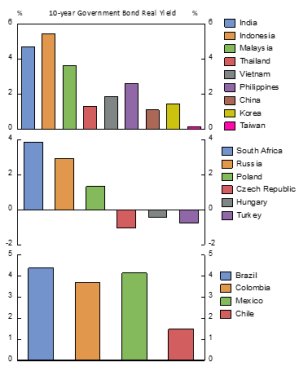

We think carry trade on EM bonds are still attractive as the differential rate is attractive for selected countries and currencies remain cheap. On the short side we pick German bund and on the long side: Indonesia, Brazil and Mexico. The former two countries are in their peak cycle and a slowdown in manufacturing activities may be due, which should bode well for bonds. Since last year, inflation in all these countries have been below 5% mark and is trending structurally lower over time.

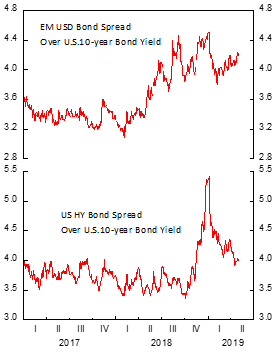

The market is also pricing 20 bps higher risk to EM hard-currency bonds relative to US High-Yield, which we think make little sense. The rebound in Emerging Market economy should decrease the riskiness of sovereign issuers: reserves in most EM countries have been flat or increasing (except in Turkey) and currencies are cheap and hence reduce the probability of currency crisis. Banking crisis likelihood is also much lower relative in the 2000’s, capital adequacy for most EM countries is above 12% to risk-weighted assets and NPL is below 5%. Also, the shift in currency composition of sovereign issuers toward local-currency bond reduces the default probability significantly.

On the risk side, continued dollar strength will deter carry-trade and might eliminate the attractiveness of holding EM currencies relative to the dollar.