Download PDF: EM_VIX_Hedging_strategy

- EM equities’ superior returns relative to its DM counterparts have been associated with higher volatility and left-tail risk. Rule-based portfolio hedging reduces the severity of tail-risk and performance drag while improving EM portfolio’s risk-return profile over the long run.

- Currently EM VIX spread over S&P500 VIX is at an all time low, meaning that insuring EM portfolio is relatively cheaper than it has ever been. The increase in correlation between markets during stress periods also reduces the basis risk of hedging EM portfolio with S&P500 VIX, making it a viable alternative. Despite higher liquidity of S&P500 VIX-based contract, basis risk from a domestic-induced market volatility could not be ruled out.

- EM stocks have historically dropped 20% every two to three years. As EM equities rally further, EM investors should be increasingly wary of higher volatility and risk of major correction.

The traditional method of hedging portfolio’s tail risk, such as buying out-of-money put options, proves to be a complicated and inefficient strategy. Investors not only have to select the right duration and strike price of the put, but the option itself is also overpriced relative to the “fair value” as signified by higher implied volatility relative to realized volatility. Although part of this problem could be alleviated through bull spread strategy (buying OTM put option and selling OTM call option), the difference in volatility term structure and cap on potential gains mean investors are at risk of trailing the benchmark if EM equity rallies abruptly.

In this report we are proposing an alternative of hedging EM portfolio using volatility-based index based on EM equity (VXEEM) and S&P500 (VIX), when volatility is increasing. Due to longer data availability of VIX relative to VXEEM, all the backtesting done in this report is simulated using the index.

The Secret Recipe

Between 2006 to February 2019 the return of holding VIX averaged -46% annually, making a buy-and-hold strategy a sure way to lose money. However, having a small portion of VIX allocation during periods of increasing volatility can reduce the tail risk significantly while reducing the cost of insuring the portfolio.

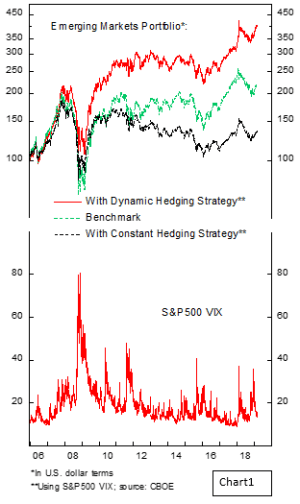

The strategy proposed in chart 2 is a very simple one: allocate 10% of EM portfolio value to long VIX position when it is above 20-day and 200-day moving average, and volatility on VIX is greater than its 10-day moving average. If at closing of the market the conditions above is satisfied, investors should long VIX index the next day. The intuition behind the strategy is that VIX shot up very quickly to an extreme level during period of stresses, which also coincide with an increase in volatility of the VIX itself. Meanwhile, on the mean-reversion process to normal level the decrease in VIX is accompanied by lower volatility of VIX itself. In this light, the model will allocate VIX on the portfolio as soon as volatility is increasing beyond its averages and exit the position when it is still at a high level but trending lower, reducing the cost of insurance significantly.

The backtesting result shown assumes daily rebalancing and zero transaction cost, investors should tailor the rules according to their rebalancing period and mandate. However, the availability of VIX ETF has made the transaction costs negligible and provides investors with the flexibility to choose the term of the VIX; short-term VIX is generally more volatile relative to medium-term VIX. During the 3442 trading days there are 150 transactions of buying and selling the VIX index, an equivalent of 4.4% turnover in the portfolio, which is not an unreasonably high number.

The rule-based strategy outperforms plain-vanilla EM equity by 83% over 12.2 years, or equivalent to an alfa generation of 5.1% annually from market timing. In contrast, having a constant 10% allocation on the EM portfolio results in an underperformance of 38% over the same period. Maximum drawdown during the GFC is also decreased to 51% compared to 64% for the benchmark.

EM VIX and S&P500 VIX

Considering the higher volatility of EM relative to U.S. equities, it is logical that EM VIX index should be higher than the S&P500 counterpart. However, the tight correlation between both markets means investors could hedge an EM portfolio using both instruments and choose the cheaper alternative. When EM VIX spread over S&P500 is low on a historical basis, investors should hedge using EM VIX, and vice versa. The impact is twofold: 1) investors are able to buy cheaper protection and 2) relative gain from the contract purchased as the spread mean-revert to normal level.

Increasing volatility in the U.S. market also often reverberate to EM’s, and the higher volatility of EM equity would translate into higher risk premium required by investors, which result in underperformance of EM stocks during periods of global risk-off. Chart 3 shows that an extremely low spread of EM VIX relative to U.S. counterpart were historically followed by underperformance of EM equity due to the complacency of EM investors, which results in EM VIX-hedging having a better hedge performance.

There are several reasons for basis risk in using S&P500 VIX to hedge EM portfolio. The first one lies in the cause of increasing volatility in both markets. If the correction in EM equity is related to dollar strength, as it did last year, S&P500 VIX may not increase by much when EM equity tumble, reducing the effectiveness of the hedge. On the other hand, hedging using S&P500 VIX when it is already at an elevated level may put investors at a loss if the U.S. market stabilize earlier than EM’s, a condition where the VIX decreases and EM stocks continue plunging, highlighted by increasing EM VIX spread over S&P500 VIX.

Green Light Ahead

We believe that the recovery in EM equities is still at its early phase and the risk/reward ratio is attractive. Last year’s 27% correction has made the overall EM stocks to be very cheap from a valuation perspective, and the troughing of many EM countries in the cycle will result in the outperformance of EM equities relative to U.S.

However, investors should be increasingly wary of the risk of major sell-off as EM stocks move higher and making new highs. Historically EM equity has a major correction every 2-3 years since 1990, stressing the importance of timing the market correctly.

The bottom line is that investors should be thinking of hedging their EM portfolio when it keeps on making new high, not when the market is already beaten out.

Kevin Yulianto, PFM

Copyright

Unless otherwise noted, all materials, including images, illustrations, designs, icons, photographs, video clips and written and other materials are part of this site and are copyrights, trademarks and other intellectual property owned, controlled or licensed by Putamen Capital or its third-party partners. Any use of materials on this site, including reproduction for purposes other than those noted above, modification, distribution or replication, without the prior written permission of Putamen Capital is strictly prohibited.

The information, recommendations, analysis and research materials presented on this site are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.