It was four decades ago when Federal Reserve last tighten monetary policy in a comparable speed and size to what we are seeing today. This is not surprising as it was also the last time the U.S. saw headline CPI inflation above 8% (Chart 1). Although the Fed was successful in bringing down inflation and keeping it low in the subsequent decade, this also comes with a great pain for workers. U.S. unemployment rate spiked from 6.3% in the beginning 1980 to 10.8% by the end of 1982 while the U.S. economy went through a severe recession (Chart 2).

The good news is that today Fed credibility is high – following decades of price stability – and long-term inflation expectations remain anchored, which should prevent currently high inflation from turning into a wage-inflation spiral. Although the Fed was late in tightening monetary policy as growth rebounded last year, this year it has been making up lost ground by raising interest rate by over 300-bps in less than eight months. Given that historically it took 6-12 months for the impact of monetary policy to be transmitted to the real economy, the market is right to worry about potential recession next year.

Chairman Powell has repeatedly said that going forward the path of interest rate hike will be taken on a meeting-by-meeting basis and based on the coming economic data, with inflation and employment situation being the key focus. The problem with this approach is that both inflation and employment data are lagging indicators, and should the Fed wait for these data to turn before adjusting its policy, it is likely already a bit late. Whereas we saw the Fed being too complacent in believing inflation to be transitory in 2021, there is the risk that the reverse is true today – with the Fed expected to deliver another 100-bps hike in the next six months even as the economy is expected to slow significantly and several leading indicators for inflation turning south. Some observations related to inflation and employment:

- The surprise in August CPI inflation is driven largely by higher shelter cost and services inflation, both of which are likely near its peak. House prices and housing sector activity lead owners’ equivalent rent by about 18 months and these indicators are pointing to a flattening of shelter cost in the coming months before possibly starting to fall in Q2/23 (Chart 3).

- Ongoing normalization in supply chain and falling commodity prices should continue to become a drag for the headline inflation in the near term. The price component of both manufacturing and non-manufacturing surveys is pointing to a deceleration in CPI inflation ahead (Chart 4). More importantly, the supply/demand balance of workers is improving, with labor force participation rate increasing to 62.4% in August from 62.1% in July (still lower than the 63.4% rate seen before the pandemic) and NFIB surveys showing that companies are planning to ease its hiring plan (Chart 5). Balancing the mismatch between job vacancy and unemployment rate should temper wage demand as labor bargaining power decline.

- Inflation expectations have remained anchored and is trending lower as the Fed tightens monetary policy (Chart 6). The 10-year inflation breakeven rate is currently trading at 2.34%, which is significantly below 2.8% in May but is still above the 2% average seen prior to the pandemic. We think long-term inflation breakeven needs to come down below 2% for the Fed to end the tightening cycle, which would also highlight market’s worry about future growth. At that point in time, risk assets should have fallen significantly, and growth will likely be under 1%.

The bottom line is that there is a significant risk the Fed will make a policy mistake by overtightening financial conditions at a time when the U.S. and global economy is slowing. Although CPI print in the coming months may continue to highlight elevated inflationary pressure, leading indicators are already pointing to lower inflation for various CPI categories. The key for the Fed is to strike a balance between curbing inflation and supporting growth. An overly tight monetary policy risks larger-than-necessary slowdown in the economy and potentially a significant rise in unemployment during the recession.

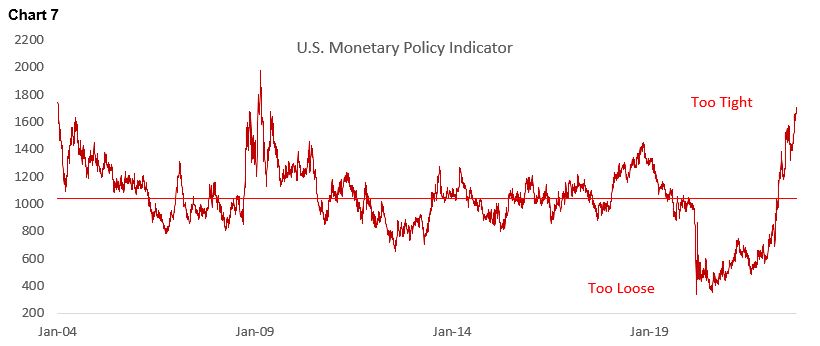

In September’s Summary of Economic Projections (SEP) released by the Fed, 2023 GDP growth is revised down to 1.2% from 1.9% in June, and unemployment rate is revised higher to 4.4% from 3.9%. Meanwhile, the median federal funds rate (FFR) is expected to rise to 4.6% in 2023 from 3.8% previously, and longer-run interest rate projection remains at 2.5%. This highlights the central bank’s expectation for the economy to grow below potential next year and loosening of labor market condition, two factors that should bring inflation closer to its 2% target. At the very end of the Q&A, Chairman Powell said, “we written down what we think is a possible path of FFR, the path that we actually execute will be enough. It will be enough to restore price stability.” This clearly shift the risk from the Fed from doing too few to curb inflation to doing too much and destroy growth (Chart 7).

Just as it takes some time for demand-driven inflationary pressure to accumulate, taming inflation and bringing it back down to 2% target will likely require some patient. The problem today is that the Fed wants to force it down rapidly out of fear (correctly) that inflation expectation will be unmoored if the currently high inflation is tolerated so stay for longer.

This forceful policy tightening, with interest rate hiked by over 300-bps in the past seven months, comes at a time when global growth is already weakening. Chinese economy is growing at an anemic 3% rate this year and will likely stay below 5% in 2023, the slowest it has been since Deng’s liberalization era in the 1990s. Europe is in recession amid the energy crisis and war on its Eastern front, and majority of German mittelstand will be facing going concern issue if energy prices do not fall quickly. Meanwhile, Emerging Market countries are being forced to raise interest rate forcefully to defend its currency from sliding against the dollar that could translate into domestic inflation problem. As growth in U.S. slows for the remainder of the year and in the first half of 2023, American will likely reduce its demand for imported goods – a headwind for export-driven economy such as China, Vietnam, South Korea and Taiwan. Already we are seeing currencies of these countries falling significantly against the dollar.

We think the global cycle is late, and there are reasons to believe on why U.S. growth next year could be even lower than the 1.2% projection made in Fed’s September SEP:

- First, despite consumer demand (70% of GDP) being more resilient than we thought earlier, the direction of goods spending continue to be lower, whereas spending on services remains below pre-pandemic trend. Chart 8 shows that spending on durable goods is now softer than a year ago, with furniture, electronics, and appliances category lower than pre-pandemic level – a sign that consumers have started to cut back on discretionary goods purchases. This is not surprising as household savings rate has fallen to 5%, below the historical average of 7% to 10% and the employment outlook is set to deteriorate (Chart 5). More importantly, consumers will increasingly feel the pinch from loss of purchasing power as real wage growth remains firmly in negative territory. None of these is surprising, as this is exactly what the Fed wants to see to cool demand.

- Second, businesses are cutting back on capex as the outlook for next year growth is highly uncertain. Although business investment accounts for only 20% of GDP, it is highly volatility and is the main driver of economic cycle. Currently, the move in cyclical/defensive stocks is discounting a deep U.S. manufacturing recession (Chart 9), and this will likely coincide with a broader economic recession (Chart 10). Outside the U.S., Europe is already in a de facto recession amid the energy crisis and Chinese growth is anemic, both of which unlikely to drive export demand for U.S. goods.

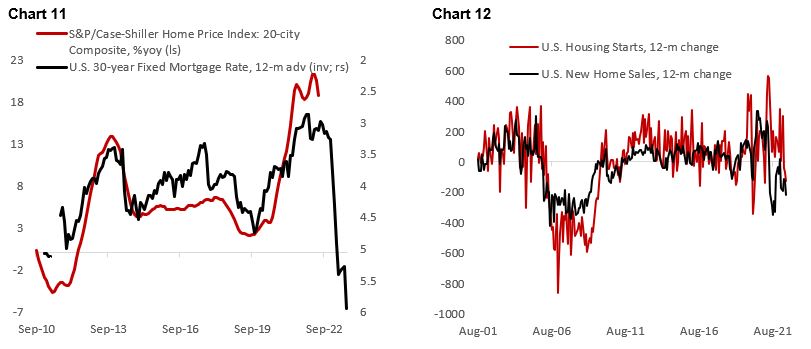

- Lastly, housing and housing-related activities are facing serious headwinds from deteriorating affordability. The Atlanta Fed GDPNow, currently forecasting Q3 GDP growth of 0.3% qoq, indicates a 1% drag on growth solely from residential investments alone. This should continue at least until the first half of 2023 (Chart 11). As property prices continue to correct, homebuilders’ sentiment and housing starts should soften and become a drag on growth (Chart 12). It remains to be seen whether there will be enough political appetite for an adequate fiscal stimulus in the coming downturn, considering that policymakers are fixated on preventing inflation from creeping higher.

In summary, there is a decent probability that monetary tightening will or has gone too far and recession is now inevitable. With 6 to 12 months lag for monetary policy to be transmitted the real economy, the full impact of over 300-bps rate hike YTD and ongoing quantitative tightening will put undue pressure on the economy when it is already in a weak spot, likely by early next year. Investors should brace for impact and maintain a defensive posture in their portfolio. The next section discusses various scenario possible that will align equities and bonds closer to fundamentals.

Recession is a Tailwind for Bonds, Equity Will Suffer

Given the high probability of recession that increasingly unlikely to be “quick and shallow”, the outlook for bonds is much more favorable relative to equity. The stock-to-bond ratio is currently 33% above its trend and should come lower as manufacturing PMI falls (Chart 13 and 14). This could be achieved by various combination of a fall in stock prices and bond yields. The most likely scenario, in our view, is an around 15% appreciation in Treasury bonds and further 15-20% decline in S&P 500 to below 3200.

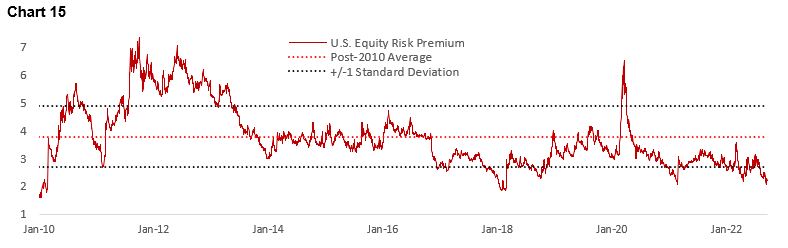

Since early this year we have warned that U.S. equities are overvalued and that slowing growth and tightening monetary policy would bode poorly for both multiple and earnings. Six months forward, the S&P 500 is 20% lower but surprisingly equity risk premium (ERP) has fallen even further to 2.2%, significantly below historical average of 3.8% (Chart 15). This is because 10-year Treasury yield has also risen from 2.3% at the end of March to 3.6% today. Unless yields start to fall, meaning that the Fed soften its stance towards policy tightening, the pain for equities will continue as growth deteriorates into 2023.

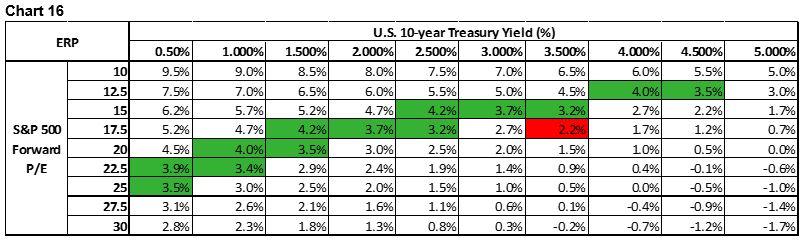

Given that we think equity risk premium has to rise above 4% for risk assets to reach bottom in this cycle, either yields have to fall drastically or multiple has to decline further (Chart 16). In our base case, consistent with our expectation for bonds to rally from current level and equities to correct by double digit, we expect a fall in 10-year Treasury yield to 2.5-3% and S&P 500 forward P/E to 15 times or below. If inflation prove to be sticky even as growth slumps in Q4/22 and Q1/23 and the Fed being forced to hold interest rate above 4.5%, equity multiple will likely fall below 13 times. This is our worst-case scenario. Either way, the outlook for bonds is much more favorable than for equities, at least for the next 3-6 months.

As discussed in the first section of this piece, there are encouraging signs that inflationary pressure going to abate in the coming months as demand cool down and that the labor market will start to loosen, which should drag down service inflation (Chart 3, 4, 5 and 8). As it become obvious that growth will enter recessionary territory next year, monetary policy should stop becoming ever tighter.

Historically, an inverted yield curve marks the top of long-term yields and currently the spread of 10/2-year curve is at -50 bps – the highest is has been since late 1990s. This highlights the risk of Fed’s policy mistake at a time when leading indicators are showing that various components of inflation will fall in the coming quarters, if not months (Chart 17). Today the 2-year yield is significantly above 10-year inflation breakeven rate, and the last time this happened was prior to the 2008 financial crisis when global growth was stronger. Back then, China was growing double digits and majority of Emerging Market countries were enjoying a commodity-driven boom. Today, Europe is in recession, China’s growth is sub-3%, and EM countries are battling with their own domestic issues – including headache from strong dollar and falling commodity prices. All of these factors will eventually blowback to the U.S. economy and translate into deflationary forces (Chart 18).

However, the current macro environment is not yet signaling imminent Fed pivot. Labor market is still relatively tight, and inflation, being the lagging indicator the Fed targets, remains at an uncomfortably high level. Inflation expectation is also still above pre-pandemic averages. However, yields do not have to rise much higher as the lagged impact of prior tightening will hit an already weak growth by the end of this year. Breakeven inflation should continue to trend lower in Q4 and it probably need to go under 2% before the Fed pause its tightening (Chart 6), which could be happening in the fourth quarter.

Stay Defensive Within Equity

In the second section above we highlight the fact that equity risk premium (ERP) for U.S. stocks is too low considering the deteriorating macro environment. U.S. equity remains overvalued and given that the Fed is adamant in inflicting some pain to the economy to bring inflation down, valuation multiple should fall to below historical average of around 16 times. So far this year, the correction in equities have been largely driven by multiple compression, while earning estimates have only started to come down and have further to go.

Staying defensive remains the key in allocating capital to equities as long as monetary condition is tightening and growth outlook continues to be revised lower. Defensive stocks have massively outperformed cyclicals this year, and it has not staged any meaningful rebound despite the head fake narrative of Fed pivot in June – unlike the broader U.S. equity benchmark. It is important to note that historically a cyclical bottom in equity coincided with a bottom in cyclical/defensive ratio, making this ratio important to monitor as confirmation of a “true” bottom that has yet to come (Chart 19).

Currently, as in mid-June, S&P 500 trades at 16.5 times forward earnings. Our base-case scenario remains anchored on the potential for forward P/E trending towards 14-16x and 10% EPS contraction, implying a fair value for S&P 500 around 3000 (Chart 20). There will be counter-trend rally in between as positioning reached extremely bearish, but it would be difficult to time. If anything, investors should stay defensive as the macro condition remains negative for risk assets.

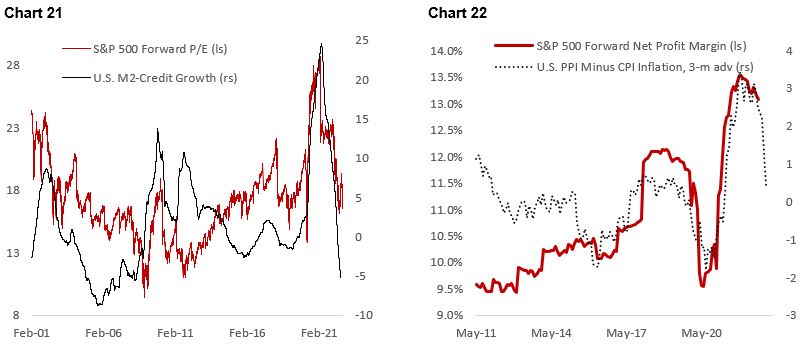

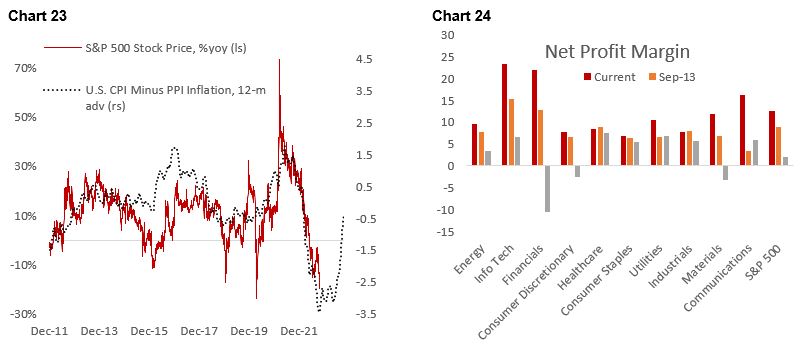

Our target for S&P 500 forward P/E of 14-15 times is based on deteriorating liquidity condition that should prick the bubble in high-multiple stocks with poor cash flow generation ability (Chart 21). Liquidity should continue to worsen in the coming quarters as the lagged impact of previous rate hikes and quantitative tightening takes effect. Meanwhile, leading indicators, such as growth tax, are indicating that earnings will fall by at least 10%. This is consistent with the high likelihood for S&P 500 margin to fall to 11.5% from 13% currently amid input cost pressure (Chart 22).

In terms of margin visibility, we expect companies to be on the defensive and focus on cutting cost until mid-2023, with the potential of positive inflection in stocks around April 2023 (Chart 23). This is the reason investors should underweight cyclical sectors in the coming months, as margins will be cut drastically in recession with growth-sensitive sectors suffering more. Chart 24 shows that margin for consumer staples, healthcare, and utilities have historically did better than other sectors during growth downturn, which drove their outperformance relative to the benchmark.

IT also has the potential to get bid at the first sign of Fed pivot, although the sector is trading rich (Chart 25). There will come a time to add industrials and financials stocks that currently trade at an attractive valuation once growth outlook improves. Energy and material stocks likely trade weaker in the short-term as recession unfolds, and investors should use this opportunity to add to their portfolio amid very constructive outlook in the coming decade. Remains underweight consumer discretionary as we expect consumer will continue to cut discretionary spending in the coming quarters.

Copyright © 2022, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.