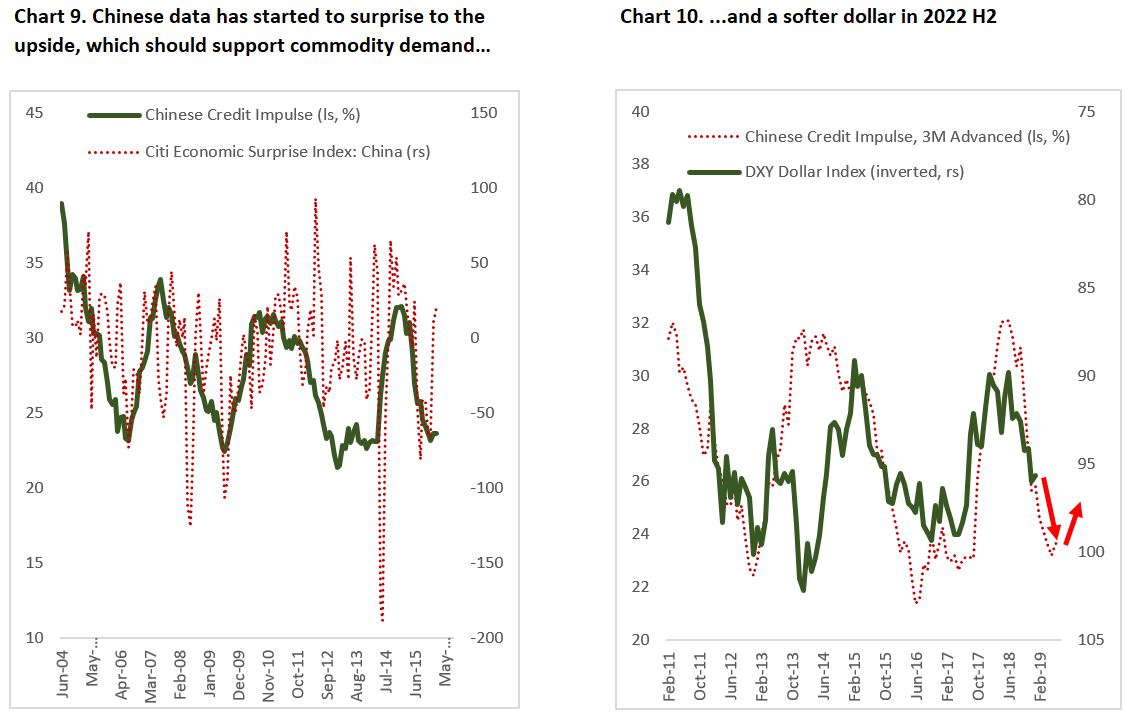

Last week the Chinese central bank finally cut one-year Loan Prime Rate (LPR) by 10bps from 3.8% to 3.7%, and also cut five-year LPR by 5bps to 4.60%, the first cut since April 2020 when global economy was in the midst of pandemic uncertainty. In the past two months we have also seen the credit impulse – which leads the economy and financial market by 6 to 9 months – bottoming. In our past publications we stressed on the urgency for Chinese policymakers to reflate the economy amid rapidly deteriorating growth outlook amid decelerating global growth and its zero-Covid policy that strains domestic demand, and we believe current monetary easing by the PBoC will translate to improving outlook for Chinese economy and stocks in the coming months.

The easing by Chinese policymakers is in stark contrast with the increasingly hawkish monetary guidance from the Federal Reserve and other major central banks around the world. The market is now pricing Fed rate hike of over 4 times this year with the possibility of 50bps hike in March meeting, while the Bank of Canada is set to raise rate as early as this week. This should bode well for the dollar and loonie, especially against EUR and JPY; both the ECB and BOJ is relatively dovish.

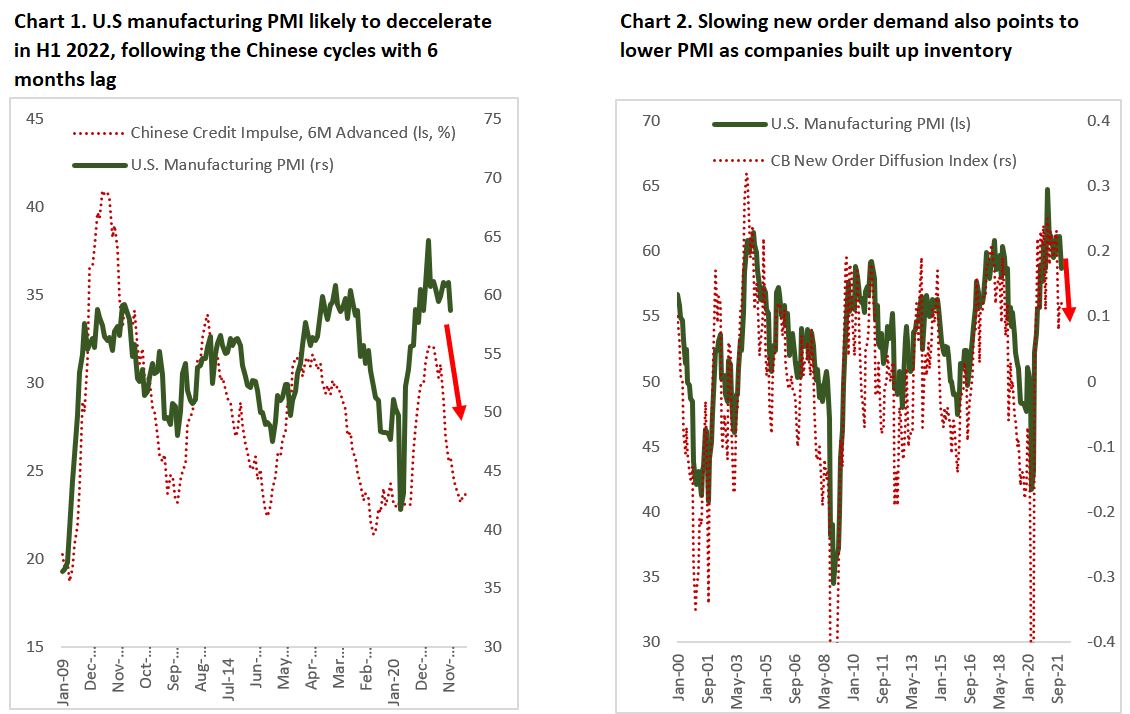

The tightening of monetary policy comes at a time when growth outlook is normalizing in the U.S. and its stock market is at an elevated valuation level. Chart 1 shows that since the Global Financial Crisis (GFC), U.S. manufacturing cycle has followed Chinese credit cycle and is currently rolling over. In addition, Conference Board New Order Diffusion Index also points to lower PMI number down the road. A slowing economy, tighter monetary conditions, and rich valuation all point to the risk of meaningful (10-20%) correction for U.S. equity in the first half this year.

Our view is that volatility should remain high in the first and second quarter of 2022 as the financial market digest weaker-than-consensus earnings and valuation headwind, before the growth outlook brighten again in Q3. S&P 500 should trade range-bound. More importantly, we doubt that the Fed could raise interest rates significantly (>2%) without choking the economy given the steepness of current yield curve (Chart 3). The 10/2 curve have room to flatten further as the Fed initially raise interest rate and 10-year Treasury yield could surprise to the downside amid aggressive tightening pushing down the already slowing growth, geopolitical uncertainty surrounding Russia-Ukraine conflict, and downward surprise in inflation.

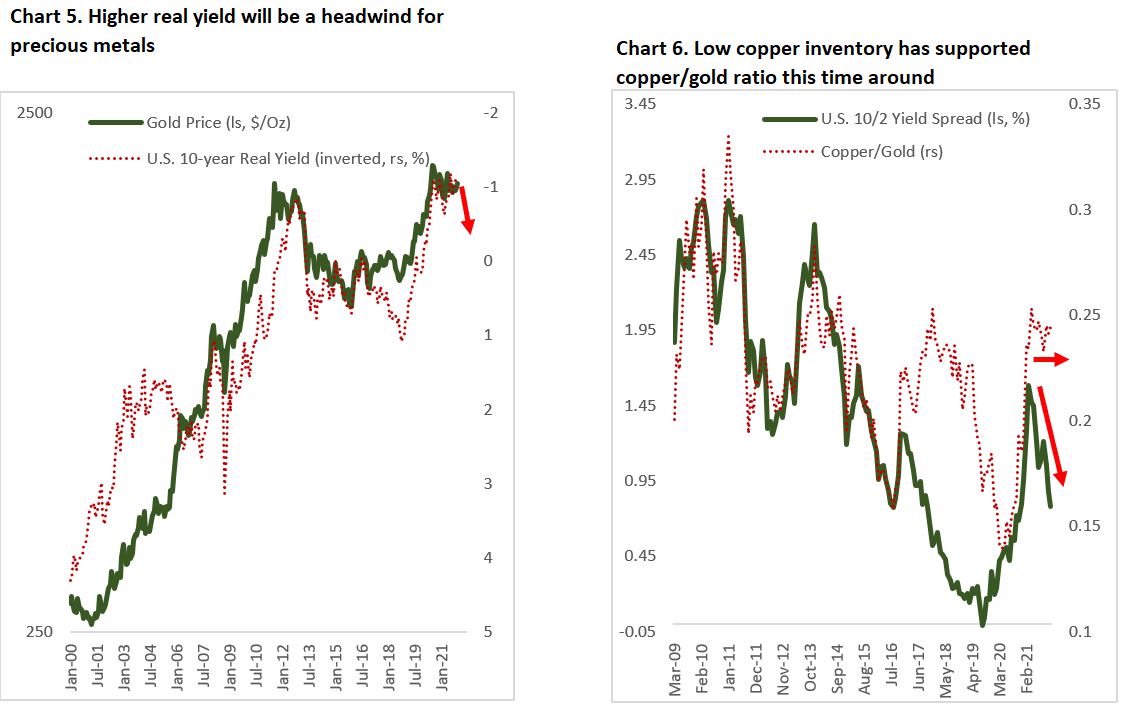

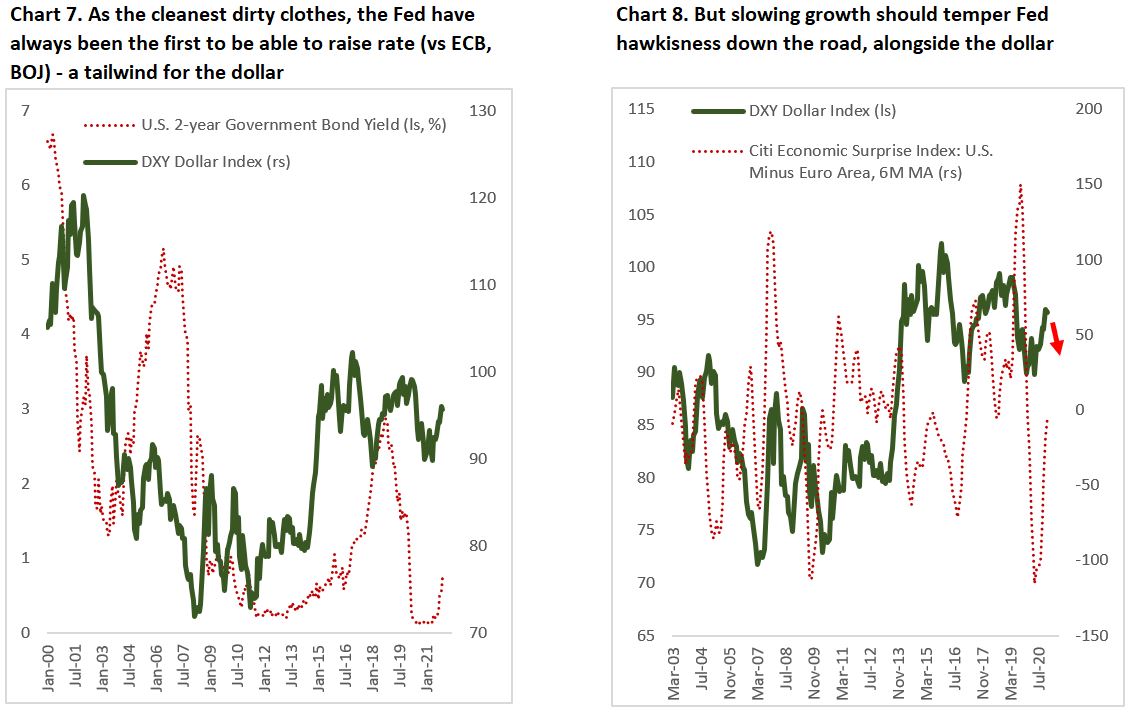

Until there is clear sign that inflation is finally rolling over, the Fed is likely to maintain its hawkish stance, driving real yield and the dollar higher (Chart 4 and Chart 7). This is the reason we are slightly bearish on gold (Chart 5). The outlook for base metals is much better, in our view. A pick-up in Chinese credit cycle historically leads to a new bull cycle for industrial metals and the world is currently facing constraint metals supply due to low investments over the past decade. Copper prices have stayed high despite the bad news surrounding Chinese real estate sector in the past year – which accounts for over 15% of global refined demand – and inventory is at decade-low level. Iron ore price has started to rebound after vicious correction since July 2021, and nickel is at all time high. Our bet is that we are in another commodity super-cycle after decade-long low commodity prices (Chart 6). As the old-adage saying goes, “the cure of low prices is low prices”. This is especially true in the energy sector today, with oil trading at $85/bbl.

Chart 8 shows that as the U.S. domestic growth slows and Chinese reflation is taking place, European economy should outpace U.S. due to its tighter correlation with Chinese growth, a headwind for the dollar in the medium term.

W are reiterating our stronger dollar conviction for the next 3 months, followed by weaker dollar afterwards (Chart 10).

Flattening yield curve and a stronger dollar implies we are entering the late phase of the business cycle, which warrants a more defensive equity positioning as volatility rises (Chart 11). This will prove to be a difficult task for managers as high-multiple growth stocks that was deemed as bulletproof in the past decade is now maturing.

Copyright © 2022, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used in this publication may have been obtained from a variety of sources including Bloomberg, Macrobond, CEIC, Choice, MSCI, BofA Merrill Lynch and JP Morgan. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.