Download PDF:

There are two main drivers of global deflationary trend in the past 30 years: rising global trade allowed by the shift towards greater openness in China and former Soviet countries and the explosion of productive-age population facilitated by the baby boomer generation (Chart 1).

In 1989, the wage gap between the developed world and China or Central Eastern European countries (Czech Republic, Hungary, and Poland) was tremendous, allowing goods manufacturers to move their production facility offshore and reduce production cost significantly, which has also translated to consumers enjoying lower goods prices. On top of this, the world was also enjoying a boom in productive-age worker that translated to greater global productive capacity. Market reforms in China and CEE countries suddenly adds 1.2 billion workers integrated to the global supply chain, forcing wages in the rich, developed countries like U.S. to compete with overseas labor.

Over the past decade, however, these two forces are starting to reverse.

- First, global trade relative to the economy has stagnated since the 2008 financial crisis, which probably was worsened by the U.S.-China trade war during Trump’s presidency. Resource nationalism means every country is trying to secure key materials to be produced domestically, and the current feud between U.S. and China over the status of Taiwan has only accelerated the rush among governments to foster their own domestic champions in critical sectors, such as semiconductor, software, and cyber security.

- Second, the Covid-19 pandemic has also shown the benefits of having a regional supply chain. It would make more sense if goods production for U.S. consumption to be based in Mexico, for example, rather than in China or India. A regionalization of manufacturing facilities is likely. Taken together, the shift in mindset among executives from “just in time” to “just in case” could translate to greater business resilience at the expense of higher cost.

- Third, falling fertility rate and the aging of baby boomers are projected to cause significant increase in dependency ratio. Rising life expectancy means demand could stay strong while labor supply shrinks, which will inevitably lead to rising inflationary pressure unless labor productivity offset the decline in employment. To be clear, we think that the current spike in inflation will prove to be temporary, but a higher average inflation figure is possible – especially if the two factors above intensify (Chart 2).

Japan = U.S. in 20 Years?

Japan is a perfect example of how a rich, developed country could continue to grow despite its declining productive-age worker. Chart 3, top panel shows that Japanese manufacturing sector has been able to maintain its output despite a third decline in employment since 1990. On average, Japan loses 1% of its labor every year, but this was offset by similar amount of productivity growth. As labor was becoming scarce and costly, corporate Japan invested heavily in productivity-enhancing machinery between 1980 and 2000, which lower its capital efficiency from 15 to 9 times (Chart 3, bottom panel). Both capital and labor efficiency has been stable, at 10 and 6 times, respectively, over the past two decades.

Chart 4 shows the situation for U.S. manufacturing sector. Similar to Japan, U.S. manufacturing employment has also been declining since early 2000s, but unlike Japan, output has continued to rise – reflective of the U.S. higher capital and labor efficiency, at 13 and 7 times, respectively. However, historical trajectory suggests that U.S. input efficiency could converge to those of Japan in the next two decades as the country continue to invest in productivity-enhancing technologies such as robotics equipment, AI, and automation.

For the whole economy, Japanese capital efficiency peaked in early 1960s when its economy was still manufacturing and export heavy (Chart 5). At the time, half of the cars produced domestically was exported and Japanese exports were growing double digit until the 1980s. As the country gets richer, however, the service sector – where productivity is lower and harder to improve – takes a larger share of the economy and drags down capital efficiency of the economy. Interestingly, U.S. capital efficiency today is at a level comparable to the peak in Japan (Chart 6) despite the structural decline in manufacturing sector share of GDP over the past half century (Chart 7).

Capital deepening and reshoring of manufacturing base to the U.S. will no happen in all sectors. It does not make sense for lower value-added goods manufacturing to be brought back to the U.S., but more advanced manufacturing of chips, electronics, airplanes and medical equipment could rejig domestic manufacturing, replacing the loss in domestic manufacturing of autos and consumer goods.

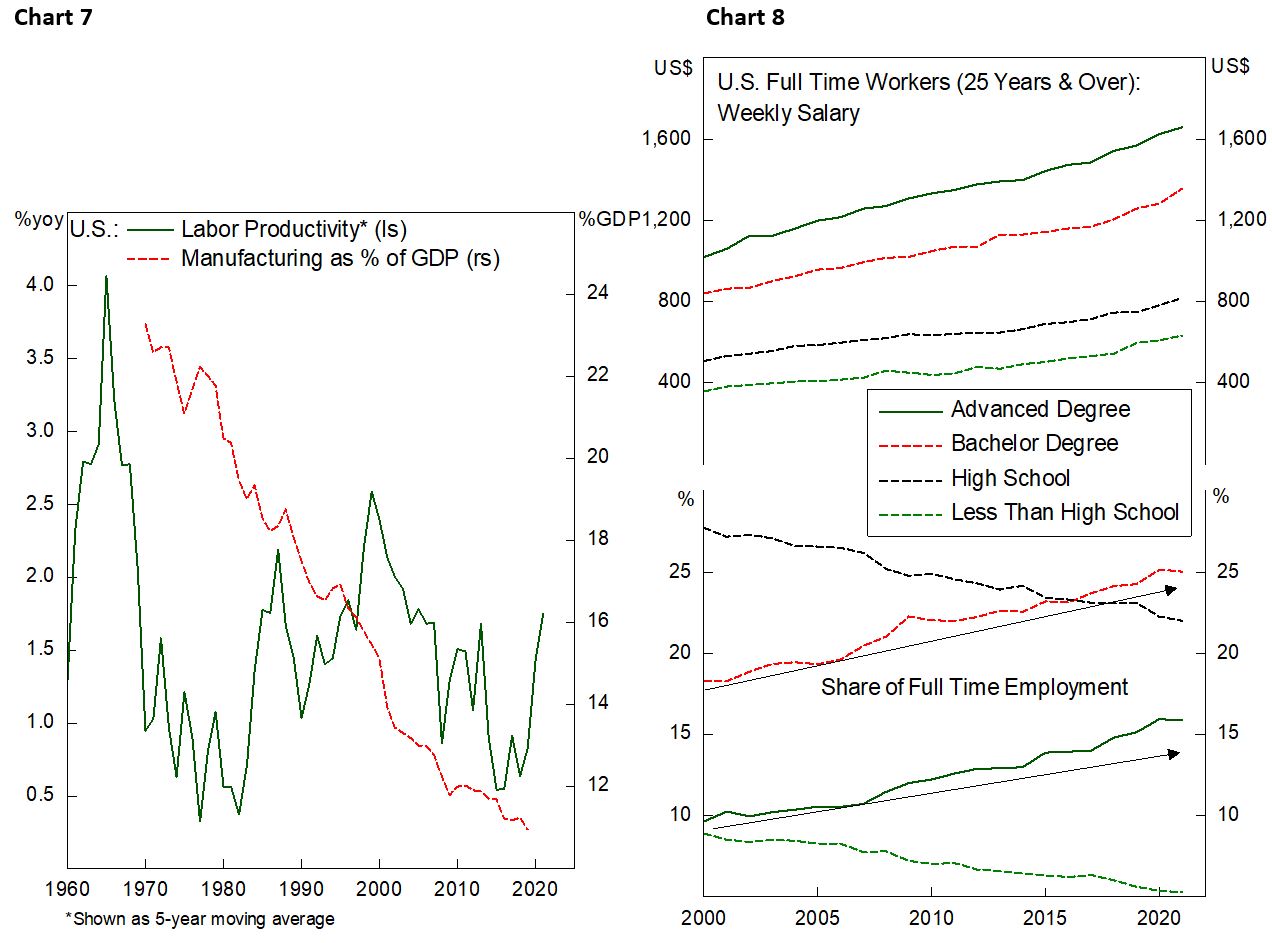

The increase in automation also means that demand for high-skilled labor will rise as jobs with low value added are automated, i.e., warehouse and delivery workers (Chart 8). Demand for worker in the low productivity service sector should remain strong as it requires higher cognitive function and is more difficult to automate, i.e., construction, restaurant, leisure, healthcare.

From investment perspective, investors should look for companies that is riding the wave of automation, either as consumer or producer of these technologies. Top among our list are players in the manufacturing of robotic arms, automated driving technologies, AI-based supply chain diagnostic, and lastly, semiconductor.

Copyright © 2021, Putamen Capital. All rights reserved.

The information, recommendations, analysis and research materials presented in this document are provided for information purposes only and should not be considered or used as an offer or solicitation to sell or buy financial securities or other financial instruments or products, nor to constitute any advice or recommendation with respect to such securities, financial instruments or products. The text, images and other materials contained or displayed on any Putamen Capital products, services, reports, emails or website are proprietary to Putamen Capital and should not be circulated without the expressed authorization of Putamen Capital. Any use of graphs, text or other material from this report by the recipient must acknowledge Putamen Capital as the source and requires advance authorization. Putamen Capital relies on a variety of data providers for economic and financial market information. The data used, or referred to, in this report are judged to be reliable, but Putamen Capital cannot be held responsible for the accuracy of data used herein.